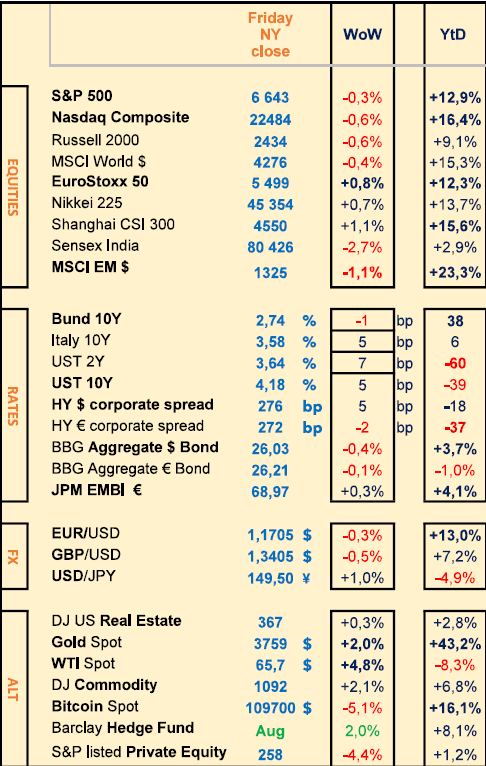

Last week: Hawkish FED comments, strong US consumer spending; SNB rate unchanged at 0%; Oil & Gold price higher

WEEKLY TRENDS

WEEKLY TRENDS

- US August PCE inflation data came out as expected but 3rd estimate of Q2 GDP rose to +3.8% io 3.3% due to robust consumer spending, confirmed in August (+0.6%) NB, US consumer sentiment is weakening (Sep Michigan survey at 55.1 vs 58.2 prior and 70.1 a year ago)

- USD stronger across the board on higher Bond yields

- Potential Russian drones into NATO space, together with lower US oil inventories and OPEC+ production increase seen difficult to achieve by some members, caused a higher Oil price last week. Gold and Silver higher despite stronger USD and higher US yields

- Cryptos had a tough week, weakened across the board including $2.75bn BTC long liquidation (despite Ripple declaring the launch of a EUR linked Stablecoin available on its EUR ledger, and the SEC validating Grayscale’s launch of the first multi-token ETF)

- Coming next week, US Sep NFP job report to be released on Friday and EU Aug CPI/PPI inflation data on Wednesday/Friday. Possible US government shutdown on Oct 1st (last one was 7 years ago)

- NB, GS rose its SP500 target to 6800 for year-end io 6600 prior (1year prediction is at 7200)

MARKETS

Equities

Specific stock weekly performances:

Petershill (+32% on its exit from LSE), OHB (+30% German gov. to spend €35bn), Kingfisher (+20% strong outlook), Renk (+16%), H&M (+13%), Intel (+20% on Apple and TSMC equity capital interests)

Gerresheimer (-22% on BaFin enquiry)

M&A:

Metsera (+56% on Pfizer interest, $7bn)

Analysts: Tate & Lyle (MS ‘u/w’ target £5), Solvay (MS ‘u/w’ target €25), Essilor (GS ‘buy’ target €305), ASML (MS ‘o/w’ target €950)

Rates

US curve (2-10 years) steepening unchanged at 55bps

HY corporate spreads higher +5bps (US at 275bps) ; EU at 270bps

Commodities

Oil price higher (+5%) on lower US inventories, possible Russian drones into NATO space, difficulty to raise production for some OPEC members

Gold price higher (+2%) despite stronger USD and higher US bond yields; Silver rose above $46 an ounce (just below its 2011 high)

US

Aug PCE inflation at +2.7% (Core at 2.9%) vs FED’s target at 2%

Crypto

BTC lower (-5%) on net ETF outflows; ETH (-11%), SOL (-4%), XRP, (-3%) Tether is looking to raise $20bn to reach a $500bn total value

Under the watch

France debt rating reviews (Moody’s 24 Oct; S&P 28 Nov)

US budget and fiscal situation (Oct 14 US court decision over tariffs)

Nota Bene

Magnificent 7 now represent a 35% weight of the SP500

US Treasury Secretary Bessent to provide a $20bn swap line to Argentina

CALENDAR

Earnings releases:

US Nike(30 Sep), EU Tesco (2 Oct)

Macro releases :

US Sep NFP job report (3 Oct), EU Aug CPI (1 Oct), Aug PPI (3 Oct)

WHAT ANALYSTS SAY

Vontobel, 24 September 2025

Author: Cécile Sati, EM Portfolio Manager

Global macroeconomic uncertainty continues to grow, marked by US trade policies and relatively tight credit spreads in both developed and emerging markets. In this unpredictable environment, emerging market investment grade (EM IG) bonds, an often overlooked asset class, deserve special attention.

These bonds could be an attractive alternative for investors seeking long-term income and greater portfolio resilience. As a subset of emerging market hard currency debt, EM IG bonds share similar characteristics with developed market investment grade (DM IG) bonds and offer additional benefits such as greater diversification and less exposure to US macroeconomic risks.

Over the past decade, the emerging market debt universe has expanded significantly, from around $1 trillion to over $3 trillion, with emerging market companies among the fastest-growing asset classes globally. In the major EM sovereign indices, the share of investment grade bonds has risen from less than 10% in the mid-1990s to around 60% today. This change reflects the adoption of more prudent macroeconomic policies in many emerging markets, enabling them to better absorb external shocks and improve overall credit quality. The weighting of the AA/A+ segment has also increased, supported by significant issuance volumes from highly rated Gulf countries such as Saudi Arabia. In EM corporate indices, investment grade issuers now account for around two-thirds of market capitalisation.

Over 10 years, EM IG corporate bonds generated an annualised return of around 3.3%, slightly above the 3.1% offered by US IG bonds. More importantly, this return was achieved with significantly lower volatility (4.1% versus 6.7%). By comparison, EM IG sovereign bonds yielded 2.7%, penalised by their longer duration, which weighed on them during the sharp rise in global interest rates in 2022. However, EM sovereign bonds generally offer better liquidity, with larger issue sizes than EM corporates. Interestingly, the relatively lower trading activity in EM IG corporates can play a defensive role in periods of high volatility. From a risk-adjusted perspective, EM IG corporates posted a higher Sharpe ratio (0.21) than US IG over the period. A 50% EM IG sovereign/50% EM IG corporate mixed allocation produces a Sharpe ratio of 0.13, comparable to that of US IG (0.14), thus offering diversification without sacrificing return.

The solid risk-adjusted returns of EM IG bonds appear to stem from a diversified composition by region and issuer, robust fundamentals and favourable technical factors. While the United States accounts for 73% of the US IG index, the EM IG universe covers 35 countries. On the issuer side, quasi-sovereigns and state-owned enterprises often operate in strategic sectors and benefit from explicit or implicit support. EM corporates are spread across various sectors such as utilities, infrastructure and banking. These are generally large, systemically important companies at the regional level, often operating in regulated markets, which provides additional stability. For their part, supranational issuers, such as development banks, have strong credit ratings thanks to strong shareholder support, preferred creditor status and prudent financial policies.

Credit quality remains robust. On the sovereign side, many EM countries have solid external buffers, including large foreign exchange reserves and current account surpluses. On the corporate side, credit metrics are generally healthier than those of their DM peers, with net leverage ratios trending lower.

Finally, in regions such as Asia and the Middle East, local institutions frequently purchase USD-denominated debt issued by their own governments or national champions, creating a stable domestic demand base that can help limit spread volatility, even when international investors become more risk-averse.

Despite an attractive risk-return profile, EM IG remains significantly underrepresented in actively managed dedicated strategies. EM corporate bonds are held by a wide variety of investors, including local institutions, crossover investors and diversified EM strategies.

Crossover investors, such as US IG managers, generally maintain only limited exposure to EM IG, as it accounts for only around 9% of global IG indices (BofA Merrill Lynch Global Corporate Index). Their positions are often concentrated in large, liquid issuers linked to the United States, which are more familiar to non-specialist investors.

Conversely, global EM strategies such as the EMBI (Emerging Markets Bond Index) and CEMBI (Corporate Emerging Markets Bond Index) invest across the entire credit spectrum, including high yield (HY). For investors with strictly investment grade mandates or tight risk budgets, these strategies are less suitable.

That is why we believe that EM IG deserves to be recognised as an asset class in its own right – capable of offering attractive returns and diversification without the typically high risks associated with HY.

Allianz Global Investors, 25 September 2025

Author : Giulia Pellegrini, EM Portfolio Manager

Emerging market debt is a broad and diverse asset class that has delivered strong performance thanks to major advances in economic policy and governance. In our view, negative perceptions of this asset class – namely that it is ‘too risky’ – are outdated. We believe emerging market debt should be a strategic allocation in portfolios, given its potential to offer diversified alpha and attractive risk-adjusted returns.

Emerging market debt has undergone a remarkable transformation over the past 30 years. Today, hard currency debt issuers span more than 70 countries, with a wide range of geographical locations and credit profiles. The share of local currency issues has also increased significantly, reflecting the growing depth of domestic markets. This development underscores the maturity and relevance of the asset class as an essential component of the global bond universe.

Over the past 30 years, emerging market debt has outperformed both US high-yield bonds and US Treasury bills. Many emerging market countries have strengthened their institutions, adopted more prudent fiscal policies and built up significant foreign exchange reserves, making them more resilient to shocks. The increased diversification of the asset class helps reduce the risk of contagion. With active management and thorough analysis, emerging market debt can offer attractive risk-adjusted returns and diversification benefits.

Many emerging markets now have stronger fiscal positions than developed markets. During the Covid-19 crisis, several emerging market central banks acted quickly to combat inflation, enabling them to support growth while preserving financial stability. Emerging market fiscal deficits and debt-to-GDP ratios are often more favourable than those of developed markets.

In addition, economic growth is faster in emerging markets, and the gap has widened in recent years.

It is therefore time to reassess emerging market debt. It has undergone a profound transformation over the past 30 years, but the perception of some investors has not yet changed. The crises and defaults of the early 1990s left a lasting mark, but many emerging economies have made great strides in strengthening their policy frameworks and institutional resilience. They have developed more diversified economies, deepened their local debt markets and improved communication and relations with international investors. These advances were particularly evident during the Covid-19 crisis, when several emerging markets responded with agility and efficiency.

In our view, both our macroeconomic analysis and the ratings agencies' assessments confirm an improvement in the economic fundamentals of emerging markets.

Since 2023, emerging markets have been more likely to see their credit ratings upgraded than downgraded. The asset class – as represented by the JP Morgan EMBIGD index – is now, on average, rated investment grade, which provides additional support.

We believe that more and more investors will turn to this asset class, which we believe should be a strategic component of any asset allocation due to its potential to offer diversified alpha and attractive risk-adjusted returns.

VanEck, 24 September 2025

Author: Alessandro Valentino, Head of Product

The space sector is establishing itself as a major driver of innovation and security. Its potential for transformation is considerable, from global connectivity to defence and Earth observation. However, this momentum remains hampered by high costs, heavy dependence on funding and geopolitical tensions, all of which are risks that must be managed in order to support sustainable expansion. Once reserved for scientific exploration, the space economy has become a strategic and technological driver. In 2024, its value was estimated at approximately $596 bn, following sustained growth in satellite services, Earth observation and related commercial applications. More than half of this market came from Positioning, Navigation and Timing (PNT) applications. These include services based on satellite signals, such as vehicle navigation, mapping, fleet tracking, air and maritime routing, and the synchronisation of financial transactions, telecommunications and electrical networks, with an estimated value of $150 bn. They also include sales of equipment and devices such as GPS receivers, smartphones, on-board navigation systems and connected objects, representing approximately $75 bn.

However, this momentum could be slowed by monetary tightening, higher launch insurance costs or geopolitical tensions limiting international cooperation. But the prospects remain considerable. According to McKinsey, the space economy could triple in size by 2035 to reach $1.8 trn, growing twice as fast as the global economy. Far from being the stuff of science fiction, space technologies such as satellite communications, defence technologies, Earth observation and in-orbit manufacturing are set to be key drivers of economic and societal progress over the next decade.

The satellite sector accounts for the largest share of the space economy and meets rapidly expanding needs, from videoconferencing to online gaming. Low-orbit constellations are multiplying. Their number has risen from 3,300 in 2020 to more than 11,500 by the end of 2024 and could approach 27,000 by 2030. Their proximity to Earth reduces latency, increases transfer speeds and extends coverage areas, making them an ideal solution for high-speed internet and connectivity in remote areas. These systems also help to bridge the digital divide, particularly in Africa, South Asia and Latin America.

The boom in public investment highlights the geopolitical dimension of space. In 2024, government spending reached a record $135 bn, with an increasing share devoted to defence. Secure communications, GPS systems, advanced surveillance and missile defence are now key priorities. Several countries, including China, Russia, the United States and Europe, have established specific military commands. In 2025, the European Union introduced the EU Space Act to strengthen the cybersecurity of space infrastructure, establish operational standards and improve resilience to interference and crises.

Private companies are now key players. They are developing disruptive technologies such as satellite constellations, synthetic aperture radars and modular systems enabling continuous surveillance. These innovations are opening up new possibilities in a variety of fields, from precision farming to logistics, finance, energy management and environmental monitoring.

Beyond these uncertainties, the space economy is emerging as a key driver of the next industrial and technological revolution. The innovative companies that comprise it are already transforming the nature of the economy and are expected to grow much faster than other sectors. Their potential is immense, but it calls for a thoughtful and diversified approach.

Equities

Specific stock weekly performances:

Petershill (+32% on its exit from LSE), OHB (+30% German gov. to spend €35bn), Kingfisher (+20% strong outlook), Renk (+16%), H&M (+13%), Intel (+20% on Apple and TSMC equity capital interests)

Gerresheimer (-22% on BaFin enquiry)

M&A:

Metsera (+56% on Pfizer interest, $7bn)

Analysts: Tate & Lyle (MS ‘u/w’ target £5), Solvay (MS ‘u/w’ target €25), Essilor (GS ‘buy’ target €305), ASML (MS ‘o/w’ target €950)

Rates

US curve (2-10 years) steepening unchanged at 55bps

HY corporate spreads higher +5bps (US at 275bps) ; EU at 270bps

Commodities

Oil price higher (+5%) on lower US inventories, possible Russian drones into NATO space, difficulty to raise production for some OPEC members

Gold price higher (+2%) despite stronger USD and higher US bond yields; Silver rose above $46 an ounce (just below its 2011 high)

US

Aug PCE inflation at +2.7% (Core at 2.9%) vs FED’s target at 2%

Crypto

BTC lower (-5%) on net ETF outflows; ETH (-11%), SOL (-4%), XRP, (-3%) Tether is looking to raise $20bn to reach a $500bn total value

Under the watch

France debt rating reviews (Moody’s 24 Oct; S&P 28 Nov)

US budget and fiscal situation (Oct 14 US court decision over tariffs)

Nota Bene

Magnificent 7 now represent a 35% weight of the SP500

US Treasury Secretary Bessent to provide a $20bn swap line to Argentina

CALENDAR

Earnings releases:

US Nike(30 Sep), EU Tesco (2 Oct)

Macro releases :

US Sep NFP job report (3 Oct), EU Aug CPI (1 Oct), Aug PPI (3 Oct)

WHAT ANALYSTS SAY

- Vontobel: Emerging Market IG bonds as a strategic anchor

- Allianz Global Investors: Dispelling misconceptions about Emerging Market debt

- VanEck: Despite risks, the space industry is establishing itself as a pillar of the next industrial and technological revolution

Vontobel, 24 September 2025

Author: Cécile Sati, EM Portfolio Manager

Global macroeconomic uncertainty continues to grow, marked by US trade policies and relatively tight credit spreads in both developed and emerging markets. In this unpredictable environment, emerging market investment grade (EM IG) bonds, an often overlooked asset class, deserve special attention.

These bonds could be an attractive alternative for investors seeking long-term income and greater portfolio resilience. As a subset of emerging market hard currency debt, EM IG bonds share similar characteristics with developed market investment grade (DM IG) bonds and offer additional benefits such as greater diversification and less exposure to US macroeconomic risks.

Over the past decade, the emerging market debt universe has expanded significantly, from around $1 trillion to over $3 trillion, with emerging market companies among the fastest-growing asset classes globally. In the major EM sovereign indices, the share of investment grade bonds has risen from less than 10% in the mid-1990s to around 60% today. This change reflects the adoption of more prudent macroeconomic policies in many emerging markets, enabling them to better absorb external shocks and improve overall credit quality. The weighting of the AA/A+ segment has also increased, supported by significant issuance volumes from highly rated Gulf countries such as Saudi Arabia. In EM corporate indices, investment grade issuers now account for around two-thirds of market capitalisation.

Over 10 years, EM IG corporate bonds generated an annualised return of around 3.3%, slightly above the 3.1% offered by US IG bonds. More importantly, this return was achieved with significantly lower volatility (4.1% versus 6.7%). By comparison, EM IG sovereign bonds yielded 2.7%, penalised by their longer duration, which weighed on them during the sharp rise in global interest rates in 2022. However, EM sovereign bonds generally offer better liquidity, with larger issue sizes than EM corporates. Interestingly, the relatively lower trading activity in EM IG corporates can play a defensive role in periods of high volatility. From a risk-adjusted perspective, EM IG corporates posted a higher Sharpe ratio (0.21) than US IG over the period. A 50% EM IG sovereign/50% EM IG corporate mixed allocation produces a Sharpe ratio of 0.13, comparable to that of US IG (0.14), thus offering diversification without sacrificing return.

The solid risk-adjusted returns of EM IG bonds appear to stem from a diversified composition by region and issuer, robust fundamentals and favourable technical factors. While the United States accounts for 73% of the US IG index, the EM IG universe covers 35 countries. On the issuer side, quasi-sovereigns and state-owned enterprises often operate in strategic sectors and benefit from explicit or implicit support. EM corporates are spread across various sectors such as utilities, infrastructure and banking. These are generally large, systemically important companies at the regional level, often operating in regulated markets, which provides additional stability. For their part, supranational issuers, such as development banks, have strong credit ratings thanks to strong shareholder support, preferred creditor status and prudent financial policies.

Credit quality remains robust. On the sovereign side, many EM countries have solid external buffers, including large foreign exchange reserves and current account surpluses. On the corporate side, credit metrics are generally healthier than those of their DM peers, with net leverage ratios trending lower.

Finally, in regions such as Asia and the Middle East, local institutions frequently purchase USD-denominated debt issued by their own governments or national champions, creating a stable domestic demand base that can help limit spread volatility, even when international investors become more risk-averse.

Despite an attractive risk-return profile, EM IG remains significantly underrepresented in actively managed dedicated strategies. EM corporate bonds are held by a wide variety of investors, including local institutions, crossover investors and diversified EM strategies.

Crossover investors, such as US IG managers, generally maintain only limited exposure to EM IG, as it accounts for only around 9% of global IG indices (BofA Merrill Lynch Global Corporate Index). Their positions are often concentrated in large, liquid issuers linked to the United States, which are more familiar to non-specialist investors.

Conversely, global EM strategies such as the EMBI (Emerging Markets Bond Index) and CEMBI (Corporate Emerging Markets Bond Index) invest across the entire credit spectrum, including high yield (HY). For investors with strictly investment grade mandates or tight risk budgets, these strategies are less suitable.

That is why we believe that EM IG deserves to be recognised as an asset class in its own right – capable of offering attractive returns and diversification without the typically high risks associated with HY.

Allianz Global Investors, 25 September 2025

Author : Giulia Pellegrini, EM Portfolio Manager

Emerging market debt is a broad and diverse asset class that has delivered strong performance thanks to major advances in economic policy and governance. In our view, negative perceptions of this asset class – namely that it is ‘too risky’ – are outdated. We believe emerging market debt should be a strategic allocation in portfolios, given its potential to offer diversified alpha and attractive risk-adjusted returns.

Emerging market debt has undergone a remarkable transformation over the past 30 years. Today, hard currency debt issuers span more than 70 countries, with a wide range of geographical locations and credit profiles. The share of local currency issues has also increased significantly, reflecting the growing depth of domestic markets. This development underscores the maturity and relevance of the asset class as an essential component of the global bond universe.

Over the past 30 years, emerging market debt has outperformed both US high-yield bonds and US Treasury bills. Many emerging market countries have strengthened their institutions, adopted more prudent fiscal policies and built up significant foreign exchange reserves, making them more resilient to shocks. The increased diversification of the asset class helps reduce the risk of contagion. With active management and thorough analysis, emerging market debt can offer attractive risk-adjusted returns and diversification benefits.

Many emerging markets now have stronger fiscal positions than developed markets. During the Covid-19 crisis, several emerging market central banks acted quickly to combat inflation, enabling them to support growth while preserving financial stability. Emerging market fiscal deficits and debt-to-GDP ratios are often more favourable than those of developed markets.

In addition, economic growth is faster in emerging markets, and the gap has widened in recent years.

It is therefore time to reassess emerging market debt. It has undergone a profound transformation over the past 30 years, but the perception of some investors has not yet changed. The crises and defaults of the early 1990s left a lasting mark, but many emerging economies have made great strides in strengthening their policy frameworks and institutional resilience. They have developed more diversified economies, deepened their local debt markets and improved communication and relations with international investors. These advances were particularly evident during the Covid-19 crisis, when several emerging markets responded with agility and efficiency.

In our view, both our macroeconomic analysis and the ratings agencies' assessments confirm an improvement in the economic fundamentals of emerging markets.

Since 2023, emerging markets have been more likely to see their credit ratings upgraded than downgraded. The asset class – as represented by the JP Morgan EMBIGD index – is now, on average, rated investment grade, which provides additional support.

We believe that more and more investors will turn to this asset class, which we believe should be a strategic component of any asset allocation due to its potential to offer diversified alpha and attractive risk-adjusted returns.

VanEck, 24 September 2025

Author: Alessandro Valentino, Head of Product

The space sector is establishing itself as a major driver of innovation and security. Its potential for transformation is considerable, from global connectivity to defence and Earth observation. However, this momentum remains hampered by high costs, heavy dependence on funding and geopolitical tensions, all of which are risks that must be managed in order to support sustainable expansion. Once reserved for scientific exploration, the space economy has become a strategic and technological driver. In 2024, its value was estimated at approximately $596 bn, following sustained growth in satellite services, Earth observation and related commercial applications. More than half of this market came from Positioning, Navigation and Timing (PNT) applications. These include services based on satellite signals, such as vehicle navigation, mapping, fleet tracking, air and maritime routing, and the synchronisation of financial transactions, telecommunications and electrical networks, with an estimated value of $150 bn. They also include sales of equipment and devices such as GPS receivers, smartphones, on-board navigation systems and connected objects, representing approximately $75 bn.

However, this momentum could be slowed by monetary tightening, higher launch insurance costs or geopolitical tensions limiting international cooperation. But the prospects remain considerable. According to McKinsey, the space economy could triple in size by 2035 to reach $1.8 trn, growing twice as fast as the global economy. Far from being the stuff of science fiction, space technologies such as satellite communications, defence technologies, Earth observation and in-orbit manufacturing are set to be key drivers of economic and societal progress over the next decade.

The satellite sector accounts for the largest share of the space economy and meets rapidly expanding needs, from videoconferencing to online gaming. Low-orbit constellations are multiplying. Their number has risen from 3,300 in 2020 to more than 11,500 by the end of 2024 and could approach 27,000 by 2030. Their proximity to Earth reduces latency, increases transfer speeds and extends coverage areas, making them an ideal solution for high-speed internet and connectivity in remote areas. These systems also help to bridge the digital divide, particularly in Africa, South Asia and Latin America.

The boom in public investment highlights the geopolitical dimension of space. In 2024, government spending reached a record $135 bn, with an increasing share devoted to defence. Secure communications, GPS systems, advanced surveillance and missile defence are now key priorities. Several countries, including China, Russia, the United States and Europe, have established specific military commands. In 2025, the European Union introduced the EU Space Act to strengthen the cybersecurity of space infrastructure, establish operational standards and improve resilience to interference and crises.

Private companies are now key players. They are developing disruptive technologies such as satellite constellations, synthetic aperture radars and modular systems enabling continuous surveillance. These innovations are opening up new possibilities in a variety of fields, from precision farming to logistics, finance, energy management and environmental monitoring.

Beyond these uncertainties, the space economy is emerging as a key driver of the next industrial and technological revolution. The innovative companies that comprise it are already transforming the nature of the economy and are expected to grow much faster than other sectors. Their potential is immense, but it calls for a thoughtful and diversified approach.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+374 43 00-43-82

Broker

broker@unibankinvest.am

research@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.