Last week: High intraday volatility for Bond yields, Gold, BTC and Oil, while US equities trend lower (5th consecutive week)

WEEKLY TRENDS

WEEKLY TRENDS

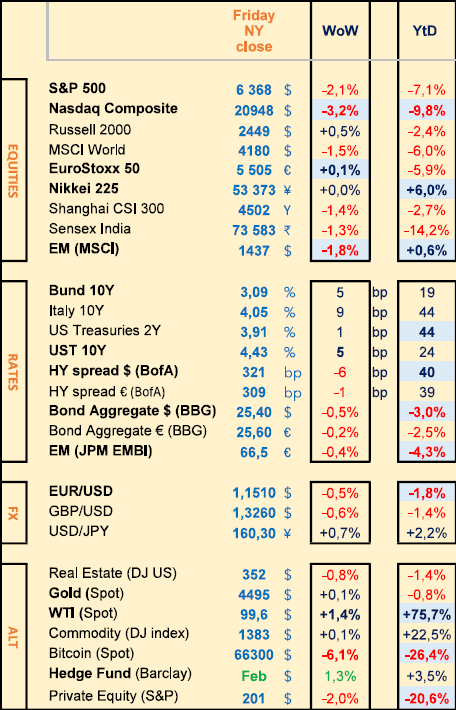

- 5 days ahead of the first Q1 earnings release (US banks) intraday volatility is at its maximum for Gold, Bond Yields (especially the longer end), Oil of course always subject to Trump’s reactions and almost daily decisions, as for the US equities, despite a small recovering for the midcaps (Russell 2000) the Nasdaq and the S&P indices kept trending lower for the 5th consecutive week, remaining way below their 200 day moving averages

- The Energy sector along with Materials outperformed naturally the Tech and Financials last week

- Trump has now set the 6th of April as a date for Iran to reopen the Hormuz strait, while US banks will start releasing their Q1 earnings on the 13th

- Meanwhile next week we shall have on Friday the publication of the US job report for March, but all eyes will remain on Iran’s response to Trump’s ultimatum

- For a month now, Oil and Gas have dramatically been higher (+55% and +85% European gas, +25% US gas that will fuel inflation) global stocks are down 8%, global bonds down 3%, Gold -17%, bearing in mind PE is down 20% and investors fear for Private credit too (including GS’ ex-CEO Blankfein 2 days ago)

MARKETS

Equities

Q4 earnings weekly performances:

Hapag-Lloyd (-22%)

NB weekly: Galderma (+5%) on FDA approval; Valneva (-40%) on inconclusive trial; Boliden (-13%), Edenred (-12%), Avis (+50%), Micron (-15%)

Bank analysts: BP (MS ‘o/w’ target £620), Novartis (MS ‘o/w’ target ₣135), Repsol (MS ‘o/w’ target €28), Total (MS ‘o/w’ target €880), BE Semi (MS ‘o/w’ target €200), ST Micro (MS ‘o/w’ target €36)

M&A: Brown-Forman (+20%) on merger talks with Pernod-Ricard (+8%), Puig (+13%) on merger talks with Estée Lauder (-21%)

Rates

US curve steepening (2-10 years) higher at +52bps (+4bps)

HY corp. spreads lower: US at +320bps (-5); EU at +310bps (flat)

Commodities

Oil price WTI (+1.5%) Trump’s 10 day ultimatum to Iran (6th April)

Gold price stable (despite intraweek volatility), TTF Gas (-12%)

Crypto

BTC (-6%), ETH (-3%), SOL (-3.5%), XRP (-3.5%), US Clarity Act proposal has been amended, showing no more remuneration on Stablecoins a/cs

Under the watch

Cross Currency Basis Swap - showing an increase of USD shortage

Nasdaq and S&P - are way below their 200 day Moving Averages

S&P Tech sector - now trading below last year’s tariff sell-off lows, trading at a 21% discount to its 5 year average P/E ratio or 10% below its 10 year

UBS gated its $500m RE fund for up to 3 years

Nota Bene

Stock markets moves since 27 Feb (War with Iran): Tel Aviv +5%, S&P -7%, Dax -11%, FTSE -9%, Nikkei -12%, Kospi -13%, UAE -15%

Key markets moves since 27 Feb: Brent +55%, Europ. gas +85%, US gas +25%, global stocks -8%, USD index +2%, UST10yr -3%, Copper -9%, Gold -17%, Coffee +6%, Platinum -14%, Palladium -23%, Cocoa +6%

CALENDAR

Earnings releases:

US Nike (31 March), *GS (13 April), JPM, Wells Fargo, Citi (14), BofA, MS (15)

EU *Shell (8 April)

Macro releases:

US March NFP job report (3rd April)

WHAT ANALYSTS SAY

Aberdeen Investments, 27 March 2026

Author: Paola Bissoli, Director

The classic question regarding raw materials is: are there enough of them? Today, a more pertinent question arises: who can process them? Those who understand this identify not only the drivers of current inflation, but also the sources of future returns. Even if oil production is sufficient, the system remains vulnerable – not only in terms of transport, but above all in terms of processing. Refineries, cracking units, LNG terminals: these facilities are highly specialised, geographically concentrated and difficult to replace in the short term. The same applies to metals. Rare earths exist all over the world, but their processing is concentrated in a few countries. Lithium is abundant, but battery-grade lithium requires highly specialised refining capabilities. What matters is not so much the resource itself as control of the value chain. True scarcity therefore lies not in the ground, but in the ability to make resources usable quickly and reliably.

Several long-term forces are converging: the energy transition, artificial intelligence and geopolitical tensions. Demand, driven by both economic imperatives and political decisions, is expected to remain robust for decades to come. Yet new capacity is failing to keep pace, and where it does exist, production volumes and quality are declining. Central banks cannot solve this problem. Monetary policy can curb inflation, but at the expense of growth, as it does not create resources.

One of the most underestimated drivers comes from the digital world. Artificial intelligence may seem intangible, but it is extremely resource-intensive: data centres consume enormous amounts of electricity, cooling and metals. Copper, uranium and rare earths are thus becoming the major, yet often overlooked, beneficiaries of digitalisation.

This demand is not cyclical, but structural – and it comes on top of that driven by the energy transition.

Greenland illustrates this paradox: vast resources but limited economic significance. Why? Because resources alone do not constitute supply. Only infrastructure, processing capacity and political acceptance enable them to be converted into usable inputs.

Scarcity is therefore not only material, but also temporal. A new mine often takes more than ten years to come on stream; refineries are costly and politically sensitive. Meanwhile, demand is accelerating.

If the real bottleneck lies not in the ground but in the capacity to utilise it, then the logic of investment changes fundamentally. What matters is not the resource itself, but the ability to extract it and transform it into productive systems. Value is created where infrastructure, processing capacity and barriers to entry are high. In this environment, traditional diversification becomes less effective. Inflation becomes less cyclical and more structural. Real assets gain in importance – particularly where physical scarcity meets structural market power.

Understanding where critical capacities are emerging and how supply chains are evolving means no longer simply investing in commodities, but in the system that underpins them.

Nordea AM, 26 March 2026

Author: Hilde Jenssen, Head of fundamental equities

Energy resilience is a central pillar of the strategic transformation currently underway in Europe. It requires significant investment in electrification and electricity infrastructure. However, the war in Iran is causing turbulence on global energy markets. In 2022, the Russia-Ukraine crisis triggered an acute supply crisis centred on Europe – particularly regarding gas – leading to emergency policy responses, high price volatility and short-term investment opportunities linked to scarcity and substitution effects. The current disruption, linked to the Middle East, differs in nature: it concerns less immediate physical shortages than a persistent geopolitical risk premium, with markets focusing more on oil, shipping routes and regional instability. Consequently, policy responses are less reactive and more strategic, reinforcing multi-year capital expenditure (capex) commitments in areas such as networks, LNG, storage, energy efficiency and domestic energy systems. This is shifting investment opportunities away from tactical and volatile strategies towards companies offering long-term growth visibility, regulated or contracted cash flows, and structural alignment with energy security and decarbonisation objectives, suggesting more lasting effects on capital allocation than the 2022 shock.

Europe remains structurally vulnerable to gas flows from the Middle East, and the current conflict illustrates how geopolitical tensions continue to influence price formation and long-term security of supply. However, this vulnerability is precisely what is driving a strengthening, rather than a slowdown, in investment in domestic energy security in Europe and allied markets. The €300bn REPowerEU programme forms the cornerstone of a multi-year response aimed at reducing dependence on imports, through the modernisation of networks, the accelerated deployment of renewable energy, the development of storage, the improvement of energy efficiency in buildings, and better access to critical raw materials. Similar trends are at work in the United Kingdom and certain regions of Asia, whilst the United States is capitalising on its dual role as a supplier of industrial equipment and an energy exporter.

The most compelling opportunities lie in electricity grid and transmission infrastructure, rather than in upstream exploration or short-cycle fossil fuel investments. This includes the modernisation of ageing networks, the development of interconnections, and the deployment of advanced cables, transformers and digital control systems needed to meet rising electricity demand driven by renewables, industry, data centres and transport.

Furthermore, downstream electrification themes, such as energy efficiency in buildings, heat pumps, storage and energy management technologies, are also promising. These developments help reduce dependence on gas and strengthen the system’s resilience. Renewables and clean energy generation remain essential, but without grid capacity and flexibility, their growth is limited; consequently, capital flows are increasingly directed towards regulated networks, equipment suppliers and industrial supply chains that support electrification.

Supported by REPowerEU and national programmes, this long-term investment opportunity is based on predictable cash flows, high barriers to entry and a structural overhaul of the European energy system, rather than cyclical exposure to commodity prices.

Robeco, 25 March 2026

Authors: Jindapa Wanner-Thavornsuk, Portfolio Manager

The rise of AI and digitalisation is driving demand for chips and water. To guard against potential shortages, chip manufacturers and local authorities are investing in large-scale water recycling solutions, creating a wave of growth for businesses across the entire water value chain.

Semiconductor manufacturing is both energy-intensive and extremely water-intensive. Chip factories (‘fabs’), which lie at the heart of AI, data centres and modern electronics, rely on ultrapure water (UPW) for rinsing and cleaning during the etching of wafers. High-performance chips used for AI, data centres and smartphones require even more water, increasing the sector’s needs as it grows.

According to the industry, a single fab consumes between 20 and 38m litres of water per day, equivalent to a small town. Large sites comprising several fabs can exceed these volumes, particularly in hot regions subject to water stress. TSMC thus consumed 101bn litres of water in 2023, a figure set to rise with next-generation technologies.

Chip manufacturing requires different levels of water quality depending on the process. To reduce water withdrawals from public utilities and catchment areas, factories must reuse water within secure systems. Thus, UPW is recycled after use for less demanding processes, such as cooling towers or wet etching. Fabs also ensure that discharged water meets the EPA’s strict standards, which have been reinforced by recent regulations on PFAS and other toxic substances. Such a level of recycling requires a wide range of technologies: advanced treatment systems to remove particles and metals, real-time monitoring tools to control purity, as well as specialised piping networks that limit corrosion and contamination.

To complicate matters, semiconductor factories are increasingly being built in regions already experiencing water stress. In the US, existing and planned fabs are located in areas of moderate to high water stress. Globally, Taiwan, South Korea, Singapore and northern China face similar constraints. A recent analysis indicates that around 40% of existing factories – and over 40% of new ones announced since 2021 – are located in regions expected to experience high or even extremely high water stress by 2030. This represents a major operational risk for one of the most strategic supply chains.

To tackle growing water-related challenges, leading chip manufacturers are investing heavily in on-site treatment, recycling and closed-loop systems. In late 2025, TSMC began construction of an industrial water recovery plant in Arizona, designed to recycle up to 90% of the wastewater from its facilities. Intel is also investing several hundred million dollars in water infrastructure at its Arizona site and, together with the city of Chandler, is developing an off-site facility to increase treatment capacity. Samsung, for its part, is partnering with Gyeonggi Province in South Korea to reuse municipal wastewater in its factories by 2029.

In fabs, additional processes produce ultrapure water for cleaning wafers, whilst separate systems manage the cooling water. Continuous monitoring devices check water quality, and specialised pumps, valves and piping ensure it is transported safely. With the global boom in AI chips and data infrastructure, demand for water-related solutions is expected to grow at every stage of the value chain.

Equities

Q4 earnings weekly performances:

Hapag-Lloyd (-22%)

NB weekly: Galderma (+5%) on FDA approval; Valneva (-40%) on inconclusive trial; Boliden (-13%), Edenred (-12%), Avis (+50%), Micron (-15%)

Bank analysts: BP (MS ‘o/w’ target £620), Novartis (MS ‘o/w’ target ₣135), Repsol (MS ‘o/w’ target €28), Total (MS ‘o/w’ target €880), BE Semi (MS ‘o/w’ target €200), ST Micro (MS ‘o/w’ target €36)

M&A: Brown-Forman (+20%) on merger talks with Pernod-Ricard (+8%), Puig (+13%) on merger talks with Estée Lauder (-21%)

Rates

US curve steepening (2-10 years) higher at +52bps (+4bps)

HY corp. spreads lower: US at +320bps (-5); EU at +310bps (flat)

Commodities

Oil price WTI (+1.5%) Trump’s 10 day ultimatum to Iran (6th April)

Gold price stable (despite intraweek volatility), TTF Gas (-12%)

Crypto

BTC (-6%), ETH (-3%), SOL (-3.5%), XRP (-3.5%), US Clarity Act proposal has been amended, showing no more remuneration on Stablecoins a/cs

Under the watch

Cross Currency Basis Swap - showing an increase of USD shortage

Nasdaq and S&P - are way below their 200 day Moving Averages

S&P Tech sector - now trading below last year’s tariff sell-off lows, trading at a 21% discount to its 5 year average P/E ratio or 10% below its 10 year

UBS gated its $500m RE fund for up to 3 years

Nota Bene

Stock markets moves since 27 Feb (War with Iran): Tel Aviv +5%, S&P -7%, Dax -11%, FTSE -9%, Nikkei -12%, Kospi -13%, UAE -15%

Key markets moves since 27 Feb: Brent +55%, Europ. gas +85%, US gas +25%, global stocks -8%, USD index +2%, UST10yr -3%, Copper -9%, Gold -17%, Coffee +6%, Platinum -14%, Palladium -23%, Cocoa +6%

CALENDAR

Earnings releases:

US Nike (31 March), *GS (13 April), JPM, Wells Fargo, Citi (14), BofA, MS (15)

EU *Shell (8 April)

Macro releases:

US March NFP job report (3rd April)

WHAT ANALYSTS SAY

- Aberdeen: The World is concerned with the Hormuz Strait closure but the real bottleneck lies elsewhere

- Nordea: Opportunities are emerging in electricity transmission and distribution infrastructure

- Robeco: Why the future of microchips depends on water

Aberdeen Investments, 27 March 2026

Author: Paola Bissoli, Director

The classic question regarding raw materials is: are there enough of them? Today, a more pertinent question arises: who can process them? Those who understand this identify not only the drivers of current inflation, but also the sources of future returns. Even if oil production is sufficient, the system remains vulnerable – not only in terms of transport, but above all in terms of processing. Refineries, cracking units, LNG terminals: these facilities are highly specialised, geographically concentrated and difficult to replace in the short term. The same applies to metals. Rare earths exist all over the world, but their processing is concentrated in a few countries. Lithium is abundant, but battery-grade lithium requires highly specialised refining capabilities. What matters is not so much the resource itself as control of the value chain. True scarcity therefore lies not in the ground, but in the ability to make resources usable quickly and reliably.

Several long-term forces are converging: the energy transition, artificial intelligence and geopolitical tensions. Demand, driven by both economic imperatives and political decisions, is expected to remain robust for decades to come. Yet new capacity is failing to keep pace, and where it does exist, production volumes and quality are declining. Central banks cannot solve this problem. Monetary policy can curb inflation, but at the expense of growth, as it does not create resources.

One of the most underestimated drivers comes from the digital world. Artificial intelligence may seem intangible, but it is extremely resource-intensive: data centres consume enormous amounts of electricity, cooling and metals. Copper, uranium and rare earths are thus becoming the major, yet often overlooked, beneficiaries of digitalisation.

This demand is not cyclical, but structural – and it comes on top of that driven by the energy transition.

Greenland illustrates this paradox: vast resources but limited economic significance. Why? Because resources alone do not constitute supply. Only infrastructure, processing capacity and political acceptance enable them to be converted into usable inputs.

Scarcity is therefore not only material, but also temporal. A new mine often takes more than ten years to come on stream; refineries are costly and politically sensitive. Meanwhile, demand is accelerating.

If the real bottleneck lies not in the ground but in the capacity to utilise it, then the logic of investment changes fundamentally. What matters is not the resource itself, but the ability to extract it and transform it into productive systems. Value is created where infrastructure, processing capacity and barriers to entry are high. In this environment, traditional diversification becomes less effective. Inflation becomes less cyclical and more structural. Real assets gain in importance – particularly where physical scarcity meets structural market power.

Understanding where critical capacities are emerging and how supply chains are evolving means no longer simply investing in commodities, but in the system that underpins them.

Nordea AM, 26 March 2026

Author: Hilde Jenssen, Head of fundamental equities

Energy resilience is a central pillar of the strategic transformation currently underway in Europe. It requires significant investment in electrification and electricity infrastructure. However, the war in Iran is causing turbulence on global energy markets. In 2022, the Russia-Ukraine crisis triggered an acute supply crisis centred on Europe – particularly regarding gas – leading to emergency policy responses, high price volatility and short-term investment opportunities linked to scarcity and substitution effects. The current disruption, linked to the Middle East, differs in nature: it concerns less immediate physical shortages than a persistent geopolitical risk premium, with markets focusing more on oil, shipping routes and regional instability. Consequently, policy responses are less reactive and more strategic, reinforcing multi-year capital expenditure (capex) commitments in areas such as networks, LNG, storage, energy efficiency and domestic energy systems. This is shifting investment opportunities away from tactical and volatile strategies towards companies offering long-term growth visibility, regulated or contracted cash flows, and structural alignment with energy security and decarbonisation objectives, suggesting more lasting effects on capital allocation than the 2022 shock.

Europe remains structurally vulnerable to gas flows from the Middle East, and the current conflict illustrates how geopolitical tensions continue to influence price formation and long-term security of supply. However, this vulnerability is precisely what is driving a strengthening, rather than a slowdown, in investment in domestic energy security in Europe and allied markets. The €300bn REPowerEU programme forms the cornerstone of a multi-year response aimed at reducing dependence on imports, through the modernisation of networks, the accelerated deployment of renewable energy, the development of storage, the improvement of energy efficiency in buildings, and better access to critical raw materials. Similar trends are at work in the United Kingdom and certain regions of Asia, whilst the United States is capitalising on its dual role as a supplier of industrial equipment and an energy exporter.

The most compelling opportunities lie in electricity grid and transmission infrastructure, rather than in upstream exploration or short-cycle fossil fuel investments. This includes the modernisation of ageing networks, the development of interconnections, and the deployment of advanced cables, transformers and digital control systems needed to meet rising electricity demand driven by renewables, industry, data centres and transport.

Furthermore, downstream electrification themes, such as energy efficiency in buildings, heat pumps, storage and energy management technologies, are also promising. These developments help reduce dependence on gas and strengthen the system’s resilience. Renewables and clean energy generation remain essential, but without grid capacity and flexibility, their growth is limited; consequently, capital flows are increasingly directed towards regulated networks, equipment suppliers and industrial supply chains that support electrification.

Supported by REPowerEU and national programmes, this long-term investment opportunity is based on predictable cash flows, high barriers to entry and a structural overhaul of the European energy system, rather than cyclical exposure to commodity prices.

Robeco, 25 March 2026

Authors: Jindapa Wanner-Thavornsuk, Portfolio Manager

The rise of AI and digitalisation is driving demand for chips and water. To guard against potential shortages, chip manufacturers and local authorities are investing in large-scale water recycling solutions, creating a wave of growth for businesses across the entire water value chain.

Semiconductor manufacturing is both energy-intensive and extremely water-intensive. Chip factories (‘fabs’), which lie at the heart of AI, data centres and modern electronics, rely on ultrapure water (UPW) for rinsing and cleaning during the etching of wafers. High-performance chips used for AI, data centres and smartphones require even more water, increasing the sector’s needs as it grows.

According to the industry, a single fab consumes between 20 and 38m litres of water per day, equivalent to a small town. Large sites comprising several fabs can exceed these volumes, particularly in hot regions subject to water stress. TSMC thus consumed 101bn litres of water in 2023, a figure set to rise with next-generation technologies.

Chip manufacturing requires different levels of water quality depending on the process. To reduce water withdrawals from public utilities and catchment areas, factories must reuse water within secure systems. Thus, UPW is recycled after use for less demanding processes, such as cooling towers or wet etching. Fabs also ensure that discharged water meets the EPA’s strict standards, which have been reinforced by recent regulations on PFAS and other toxic substances. Such a level of recycling requires a wide range of technologies: advanced treatment systems to remove particles and metals, real-time monitoring tools to control purity, as well as specialised piping networks that limit corrosion and contamination.

To complicate matters, semiconductor factories are increasingly being built in regions already experiencing water stress. In the US, existing and planned fabs are located in areas of moderate to high water stress. Globally, Taiwan, South Korea, Singapore and northern China face similar constraints. A recent analysis indicates that around 40% of existing factories – and over 40% of new ones announced since 2021 – are located in regions expected to experience high or even extremely high water stress by 2030. This represents a major operational risk for one of the most strategic supply chains.

To tackle growing water-related challenges, leading chip manufacturers are investing heavily in on-site treatment, recycling and closed-loop systems. In late 2025, TSMC began construction of an industrial water recovery plant in Arizona, designed to recycle up to 90% of the wastewater from its facilities. Intel is also investing several hundred million dollars in water infrastructure at its Arizona site and, together with the city of Chandler, is developing an off-site facility to increase treatment capacity. Samsung, for its part, is partnering with Gyeonggi Province in South Korea to reuse municipal wastewater in its factories by 2029.

In fabs, additional processes produce ultrapure water for cleaning wafers, whilst separate systems manage the cooling water. Continuous monitoring devices check water quality, and specialised pumps, valves and piping ensure it is transported safely. With the global boom in AI chips and data infrastructure, demand for water-related solutions is expected to grow at every stage of the value chain.

Contacts

8 Kievyan Street, Yerevan, Armenia

+374 10 712 259

+374 43 004 182

unibankinvest@unibank.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.