Last week: long due Tech stocks correction; UK base rate unchanged; Oil down; BTC dropped; Gold ended unchanged

WEEKLY TRENDS

WEEKLY TRENDS

- A long due and sound correction hit stocks and cryptos last week, corporate spreads are consequently higher

- The US government shutdown is still on and worrying investors as no statistics are available to gauge the US economy pulse since the Summer

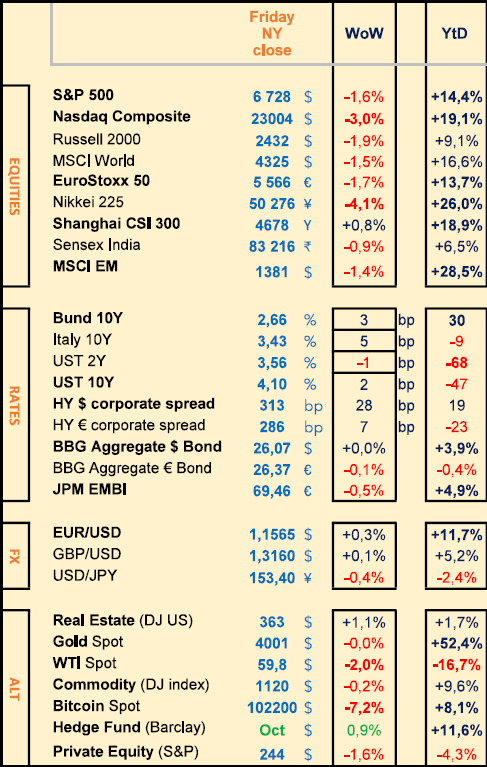

- End of year adjustments have well and truly started. US tech, the most performing stocks so far this year, have been hit the hardest (Palantir -13%, AMD -10%, Nvidia -10%) while some Q3 earnings releases have let EU stocks in positive territory for the week (Rheinmetall +2%, AstraZeneca +2%, Engie +4%, BP +2%). CEOs of GS and MS have both warned last week of a 10 to 20% stock market drawdown (then at a HK financial leaders’ investment summit)

- The UK BOE/MPC kept its base rate unchanged at 4%, a high probability remains for a -25bps Dec cut though. Last OPEC+ meeting decided to increase production starting Dec 1st but to keep its production stable in Q1

- Bitcoin dropped by -7% while ETH fell by -17% and SOL by -20% (approximately $400bn crypto market value lost last week)

- Next week corporate earnings releases include Siemens, Richemont, Alibaba, Tencent and US CoreWeave.

MARKETS

Equities

Weekly performances after earnings releases:

BP (+2%), AstraZeneca (+2%), Rheinmetall (+2%), Engie (+4%)

AMD (-10%), Palantir (-13%), NovoNordisk (-8%), Edenred (-16%)

M&A: Pfizer to buy Metsera for $10bn

Analysts: Edenered (BNPP ‘o/w’ target €39), Essilor (MS ‘o/w’ target €365), Geberit (Barclays ‘o/w’ target ₣560, JPM target ₣600)

Rates

US curve (2-10 years) steepening slightly higher at 54bps (+5bps)

HY corp. spreads higher (+30bps for US at 315bps, +5bps for EU at 285)

Commodities

Oil price lower (-2%) after new OPEC’s production rise decision (+137k barrels per day, starting Dec 1st) S. Arabia sells its oil cheaper to Asia

Gold price stable (ending the week, just above the $4000 mark)

US

Oct ISM Manufacturing index fell to 48.7 (8th straight month of contraction) orders backlog have been contracting for 3 years

Crypto

BTC lower (-7%), Stablecoins hit $311bn in circulation, processing more payments than Visa this year (expected to be $2000bn by 2028)

Under the watch

AI data centres off-balance sheet debts (Meta has $30bn AI related debt in off balance sheet SPV with Blue Owl Capital) UBS estimates AI debt grow by $100bn per quarter, MS projects it to be $800bn by 2028

UK economy expected to grow by +1.5% in 2025 (EY item club thinktank), base rate expected at 3.5% in 2026

Nota Bene

S&P 500 earnings are up +14% (highest growth rate since Q4 2021 and 7 out of 11 sectors present margin expansion)

Current US shutdown is the longest in history (40 days vs 35 in 2019)

CALENDAR

Q3 earnings releases:

US CoreWeave (10 Nov), Cisco (12), Applied Materials (13) EU Siemens (13 Nov), Richemont (14)

Tencent, Alibaba (13)

US macro releases:

Sep - Oct CPI /PPI/NFP (pending US government shutdown)

WHAT ANALYSTS SAY

Lombard Odier, 5 November 2025

Author: Michael Strobaek, CIO, Head of investment solutions

· Markets tend to rise over the long term, corrections are less frequent than generally thought, waiting to invest can therefore be costly

· Buying opportunities are psychologically difficult to seize, while markets usually price in known risks efficiently, leaving little room for individual investors to take advantage

· Attempts to avoid a market correction can therefore prove more costly in terms of performance than the correction itself

· We emphasise discipline, diversification, setting of long-term objectives as the most reliable tools for weathering the inevitable market turbulence

The logic behind anticipating a potential correction often has more to do with psychology than actual data. Markets tend to quickly factor in recognised risks. When a risk – such as a potential recession or an expected rise in interest rates – is widely discussed, it is almost certainly already reflected in prices.

An individual investor is unlikely to be ahead of the market.Therefore, if the impact does occur, it is likely to be less severe than expected.

The real danger therefore lies not in the risk itself, but in the gap between perceived risk and actual risk. In this context, market shocks generally take two forms:

· Exogenous shocks – wars, pandemics or other unpredictable disruptions – which are impossible to anticipate with any degree of accuracy. These represent the ‘unknown unknowns’, or highly unpredictable factors.

· Endogenous shocks, or financial market shocks, are linked to excessive valuations and structural imbalances: in other words, bubbles. These risks are easier to observe, but remain difficult to anticipate. The ‘Nifty Fifty’ speculative bubble of the 1960s and 1970s and the Internet bubble that burst in 2000 both lasted longer than sceptics predicted, and attempts to avoid them often came at the expense of compound gains.

That is why perfect timing seems to us to be nothing more than a comforting illusion. The idea of anticipating the exact low point or avoiding every correction is appealing, but generally unrealistic. History shows that weathering volatility is much more profitable than trying to circumvent it.

What builds wealth over the long term is not the accuracy of timing, but participation in the market.

Past experience suggests that the real advantage lies in staying invested, with an appropriate risk profile and asset allocation, while letting the quiet power of compounding do most of the work.

In the short term, markets will almost always appear overbought, and geopolitical events will almost certainly encourage investors to wait. However, trying to avoid a correction can be more costly in terms of performance than weathering the correction.

That is why we continue to emphasise discipline, diversification and setting long-term goals as the most reliable tools for navigating the inevitable market turbulence. In short, get started or you will miss the boat.

Aberdeen Investments, 7 November 2025

Author: Karsten-Dirk Steffens, Country Head Switzerland

Between 2003 and 2024, dividends paid in emerging countries grew by an average of 11.8% per year, significantly outpacing developed economies. With their robust cash flows and increasingly shareholder-friendly governance, these regions are becoming a sustainable alternative for long-term investors.

The Middle East: a driver of diversification

Ten years ago, Saudi Arabia and the United Arab Emirates had little weight in emerging market indices. Today, they occupy a place comparable to that of Latin America. Saudi Arabia is investing heavily in tourism, culture and technology in order to reduce its dependence on oil.

The Emirates, for its part, is positioning itself as a regional hub for innovation open to international capital. New companies are emerging in the infrastructure, logistics and clean energy sectors. The boom in IPOs and technologies such as energy-efficient urban cooling demonstrates the region's long-term growth potential.

Southeast Asia combines digitalisation and dividends

In Southeast Asia, the rise of a dynamic middle class is transforming local economies. In Indonesia, banks and telecom operators are increasing their profitability through digitalisation, while maintaining a generous dividend policy. In Vietnam, economic reforms and market liberalisation are attracting foreign investors. Companies with stable governance are consolidating regular distribution models there. In the Philippines, infrastructure and logistics players are taking advantage of a young population and booming trade to generate solid revenue streams.

Central Asia: a new Eurasian growth arc

Central Asia is entering a strategic phase of development. Kazakhstan, one of the world's largest uranium producers, is benefiting from the return to favour of nuclear power as a sustainable energy source. Its low production costs and integrated logistics chains make it a reliable player for investors seeking stable energy returns. In Georgia, technologically advanced banks with rigorous risk management are establishing themselves as new regional players. The region thus offers unique opportunities for diversification, relatively independent of Western economic cycles.

Latin America: the rebirth of forgotten markets

Beyond Brazil, Latin America is experiencing a new dynamic. Peru is benefiting from the copper boom, strengthening public finances and attracting investment, particularly in the financial and technology sectors. Mexico, with its solid economy and stable balance sheets, is seeing the emergence of sustainable models, particularly in airport management. Strong pricing power and growth in air traffic are supporting recurring revenues.

From Eurasia to Latin America, new regions are emerging as reliable sources of dividends, attracting investors seeking stability and diversification.

Natixis Investment Managers, 6 November 2025

Author: Garrett Melson, Portfolio Manager

After a year marked by reversals and successive market narratives, the US economy finds itself, on the whole, in the same position as it was a year ago. Growth, after rebounding from the slowdown caused by economic policy at the beginning of the year, remains resilient but seems to have converged towards its long-term trend. Inflation remains above the Fed's target while continuing on its disinflationary path. Unemployment continues to fall slowly, a sign of a labour market stuck in a dynamic of low hiring and low turnover, prompting the Federal Reserve to shift its priorities towards employment. The property market, which is also stagnant, continues to suffer from low affordability and persistently high mortgage rates, which are dampening demand, while rising inventories of completed properties are weighing on prices and construction. At the same time, the wave of investment in artificial intelligence continues to fuel a bull market dominated by technology, while the strength of the dollar serves as a reminder that American exceptionalism is not yet a thing of the past.

While the precise content of the political agenda remains unclear, the uncertainty that shook the world at the beginning of the year was mainly due to ideological motivations and convictions that are still poorly understood. An acronym now sums up the spirit of 2025: TACO – ‘Trump Always Chickens Out’. This is not meant as a criticism of the president, but rather as an observation that the markets can rely on the already proven scenario of his first term. Trump's programme may be broader and more ambitious, but it now appears to be primarily transactional.

Markets are concerned with profits, not politics, and US companies are still demonstrating their ability to adapt, regardless of who occupies the White House. Give them rules of the game, even if they are changing, and they will find ways to adapt and grow their margins. The safeguards around political decisions are still in place, and that is enough to give companies and investors the visibility they need to move forward. This does not mean, however, that the risks have disappeared. Despite recent volatility and recurring concerns about the concentration of stock market performance, investors seem to have adopted a reflation scenario: stabilisation of the labour market, strengthening growth, slightly expansionary fiscal policy and an accommodative Fed. This environment is strangely reminiscent of last year, when the consensus seemed overly optimistic about growth potential. The apparent stability of the labour market masks a build-up of imbalances: unemployment is rising, job creation is slowing and wage growth is losing momentum, weighing on incomes and consumption – despite the wealth effects supporting affluent households. Fiscal adjustments will provide some support through increased tax refunds, but this will represent little more than 1% of annual household spending, while tariffs will absorb part of it. In addition, the persistent weakness of the real estate sector could ultimately affect employment, with developers reducing their workforce in response to rising unsold inventories.

However, this does not spell recession. Growth is simply expected to be slightly below trend, without plunging into a downward spiral.

Moderate expansion, supported by the Fed and the continued rise of AI, could still provide fertile ground for risky assets and reinforce the dominant position of the United States, regardless of the political climate in Washington.

Equities

Weekly performances after earnings releases:

BP (+2%), AstraZeneca (+2%), Rheinmetall (+2%), Engie (+4%)

AMD (-10%), Palantir (-13%), NovoNordisk (-8%), Edenred (-16%)

M&A: Pfizer to buy Metsera for $10bn

Analysts: Edenered (BNPP ‘o/w’ target €39), Essilor (MS ‘o/w’ target €365), Geberit (Barclays ‘o/w’ target ₣560, JPM target ₣600)

Rates

US curve (2-10 years) steepening slightly higher at 54bps (+5bps)

HY corp. spreads higher (+30bps for US at 315bps, +5bps for EU at 285)

Commodities

Oil price lower (-2%) after new OPEC’s production rise decision (+137k barrels per day, starting Dec 1st) S. Arabia sells its oil cheaper to Asia

Gold price stable (ending the week, just above the $4000 mark)

US

Oct ISM Manufacturing index fell to 48.7 (8th straight month of contraction) orders backlog have been contracting for 3 years

Crypto

BTC lower (-7%), Stablecoins hit $311bn in circulation, processing more payments than Visa this year (expected to be $2000bn by 2028)

Under the watch

AI data centres off-balance sheet debts (Meta has $30bn AI related debt in off balance sheet SPV with Blue Owl Capital) UBS estimates AI debt grow by $100bn per quarter, MS projects it to be $800bn by 2028

UK economy expected to grow by +1.5% in 2025 (EY item club thinktank), base rate expected at 3.5% in 2026

Nota Bene

S&P 500 earnings are up +14% (highest growth rate since Q4 2021 and 7 out of 11 sectors present margin expansion)

Current US shutdown is the longest in history (40 days vs 35 in 2019)

CALENDAR

Q3 earnings releases:

US CoreWeave (10 Nov), Cisco (12), Applied Materials (13) EU Siemens (13 Nov), Richemont (14)

Tencent, Alibaba (13)

US macro releases:

Sep - Oct CPI /PPI/NFP (pending US government shutdown)

WHAT ANALYSTS SAY

- Lombard Odier: Attempts to avoid a market correction can prove more costly in terms of performance than the correction itself

- Aberdeen Investments: Sources of dividends beyond the BRICS

- Natixis Investment Managers: The US economy remains strong despite uncertainties

Lombard Odier, 5 November 2025

Author: Michael Strobaek, CIO, Head of investment solutions

· Markets tend to rise over the long term, corrections are less frequent than generally thought, waiting to invest can therefore be costly

· Buying opportunities are psychologically difficult to seize, while markets usually price in known risks efficiently, leaving little room for individual investors to take advantage

· Attempts to avoid a market correction can therefore prove more costly in terms of performance than the correction itself

· We emphasise discipline, diversification, setting of long-term objectives as the most reliable tools for weathering the inevitable market turbulence

The logic behind anticipating a potential correction often has more to do with psychology than actual data. Markets tend to quickly factor in recognised risks. When a risk – such as a potential recession or an expected rise in interest rates – is widely discussed, it is almost certainly already reflected in prices.

An individual investor is unlikely to be ahead of the market.Therefore, if the impact does occur, it is likely to be less severe than expected.

The real danger therefore lies not in the risk itself, but in the gap between perceived risk and actual risk. In this context, market shocks generally take two forms:

· Exogenous shocks – wars, pandemics or other unpredictable disruptions – which are impossible to anticipate with any degree of accuracy. These represent the ‘unknown unknowns’, or highly unpredictable factors.

· Endogenous shocks, or financial market shocks, are linked to excessive valuations and structural imbalances: in other words, bubbles. These risks are easier to observe, but remain difficult to anticipate. The ‘Nifty Fifty’ speculative bubble of the 1960s and 1970s and the Internet bubble that burst in 2000 both lasted longer than sceptics predicted, and attempts to avoid them often came at the expense of compound gains.

That is why perfect timing seems to us to be nothing more than a comforting illusion. The idea of anticipating the exact low point or avoiding every correction is appealing, but generally unrealistic. History shows that weathering volatility is much more profitable than trying to circumvent it.

What builds wealth over the long term is not the accuracy of timing, but participation in the market.

Past experience suggests that the real advantage lies in staying invested, with an appropriate risk profile and asset allocation, while letting the quiet power of compounding do most of the work.

In the short term, markets will almost always appear overbought, and geopolitical events will almost certainly encourage investors to wait. However, trying to avoid a correction can be more costly in terms of performance than weathering the correction.

That is why we continue to emphasise discipline, diversification and setting long-term goals as the most reliable tools for navigating the inevitable market turbulence. In short, get started or you will miss the boat.

Aberdeen Investments, 7 November 2025

Author: Karsten-Dirk Steffens, Country Head Switzerland

Between 2003 and 2024, dividends paid in emerging countries grew by an average of 11.8% per year, significantly outpacing developed economies. With their robust cash flows and increasingly shareholder-friendly governance, these regions are becoming a sustainable alternative for long-term investors.

The Middle East: a driver of diversification

Ten years ago, Saudi Arabia and the United Arab Emirates had little weight in emerging market indices. Today, they occupy a place comparable to that of Latin America. Saudi Arabia is investing heavily in tourism, culture and technology in order to reduce its dependence on oil.

The Emirates, for its part, is positioning itself as a regional hub for innovation open to international capital. New companies are emerging in the infrastructure, logistics and clean energy sectors. The boom in IPOs and technologies such as energy-efficient urban cooling demonstrates the region's long-term growth potential.

Southeast Asia combines digitalisation and dividends

In Southeast Asia, the rise of a dynamic middle class is transforming local economies. In Indonesia, banks and telecom operators are increasing their profitability through digitalisation, while maintaining a generous dividend policy. In Vietnam, economic reforms and market liberalisation are attracting foreign investors. Companies with stable governance are consolidating regular distribution models there. In the Philippines, infrastructure and logistics players are taking advantage of a young population and booming trade to generate solid revenue streams.

Central Asia: a new Eurasian growth arc

Central Asia is entering a strategic phase of development. Kazakhstan, one of the world's largest uranium producers, is benefiting from the return to favour of nuclear power as a sustainable energy source. Its low production costs and integrated logistics chains make it a reliable player for investors seeking stable energy returns. In Georgia, technologically advanced banks with rigorous risk management are establishing themselves as new regional players. The region thus offers unique opportunities for diversification, relatively independent of Western economic cycles.

Latin America: the rebirth of forgotten markets

Beyond Brazil, Latin America is experiencing a new dynamic. Peru is benefiting from the copper boom, strengthening public finances and attracting investment, particularly in the financial and technology sectors. Mexico, with its solid economy and stable balance sheets, is seeing the emergence of sustainable models, particularly in airport management. Strong pricing power and growth in air traffic are supporting recurring revenues.

From Eurasia to Latin America, new regions are emerging as reliable sources of dividends, attracting investors seeking stability and diversification.

Natixis Investment Managers, 6 November 2025

Author: Garrett Melson, Portfolio Manager

After a year marked by reversals and successive market narratives, the US economy finds itself, on the whole, in the same position as it was a year ago. Growth, after rebounding from the slowdown caused by economic policy at the beginning of the year, remains resilient but seems to have converged towards its long-term trend. Inflation remains above the Fed's target while continuing on its disinflationary path. Unemployment continues to fall slowly, a sign of a labour market stuck in a dynamic of low hiring and low turnover, prompting the Federal Reserve to shift its priorities towards employment. The property market, which is also stagnant, continues to suffer from low affordability and persistently high mortgage rates, which are dampening demand, while rising inventories of completed properties are weighing on prices and construction. At the same time, the wave of investment in artificial intelligence continues to fuel a bull market dominated by technology, while the strength of the dollar serves as a reminder that American exceptionalism is not yet a thing of the past.

While the precise content of the political agenda remains unclear, the uncertainty that shook the world at the beginning of the year was mainly due to ideological motivations and convictions that are still poorly understood. An acronym now sums up the spirit of 2025: TACO – ‘Trump Always Chickens Out’. This is not meant as a criticism of the president, but rather as an observation that the markets can rely on the already proven scenario of his first term. Trump's programme may be broader and more ambitious, but it now appears to be primarily transactional.

Markets are concerned with profits, not politics, and US companies are still demonstrating their ability to adapt, regardless of who occupies the White House. Give them rules of the game, even if they are changing, and they will find ways to adapt and grow their margins. The safeguards around political decisions are still in place, and that is enough to give companies and investors the visibility they need to move forward. This does not mean, however, that the risks have disappeared. Despite recent volatility and recurring concerns about the concentration of stock market performance, investors seem to have adopted a reflation scenario: stabilisation of the labour market, strengthening growth, slightly expansionary fiscal policy and an accommodative Fed. This environment is strangely reminiscent of last year, when the consensus seemed overly optimistic about growth potential. The apparent stability of the labour market masks a build-up of imbalances: unemployment is rising, job creation is slowing and wage growth is losing momentum, weighing on incomes and consumption – despite the wealth effects supporting affluent households. Fiscal adjustments will provide some support through increased tax refunds, but this will represent little more than 1% of annual household spending, while tariffs will absorb part of it. In addition, the persistent weakness of the real estate sector could ultimately affect employment, with developers reducing their workforce in response to rising unsold inventories.

However, this does not spell recession. Growth is simply expected to be slightly below trend, without plunging into a downward spiral.

Moderate expansion, supported by the Fed and the continued rise of AI, could still provide fertile ground for risky assets and reinforce the dominant position of the United States, regardless of the political climate in Washington.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+374 43 00-43-82

Broker

broker@unibankinvest.am

research@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.