Trump/FED honeymoon for US stocks (energy, financials, tech) - Euro zone lags behind (on US tariffs and German politics)

WEEKLY TRENDS

WEEKLY TRENDS

- After Trump’s victory and the 25bp FED rate cut, US stock markets had two reasons to celebrate last week, the SP500 even broke the 6000 mark briefly on Friday. Trump’s MAGA (Make America Great Again) should lead to lower companies’ taxation, boost energy production, have deregulations including in cryptos and hike tariffs, leading to more inflation

- Short dated US Bond yields are up while long dated are down (given the budget deficit Trump’s politics would create in the longer run)

- China announced a $1.4trn debt swap last week, BOE, FED and Riksbank cut their rates

- October US ISM figures were above consensus for Services, Oil price went back up due to OPEC+ decision to postpone its production hike until the end of December

- Note: Palantir, Tesla, Coinbase stocks

MARKETS

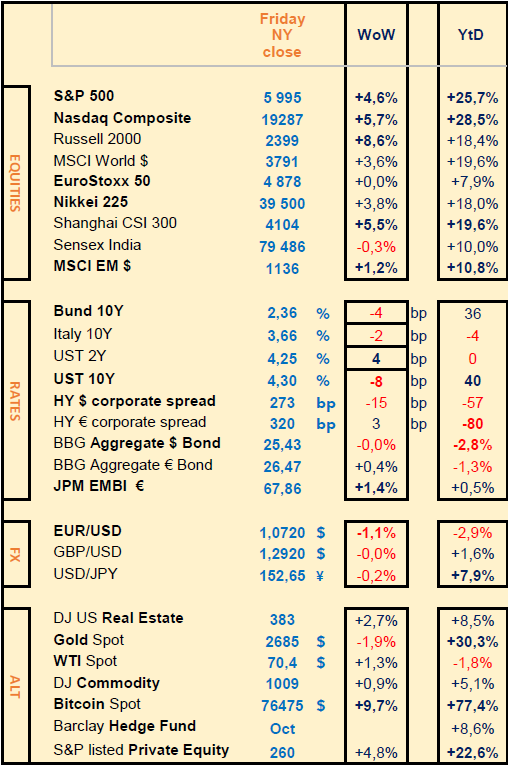

Equities

Q3 earnings releases last week (stock WoW performance):

+++ Palantir (+42%), Berkshire Hathaway (+3%), Qualcomm (+3%), ARM Holdings (+5%), Swiss Re (+6%)

- - - Novo Nordisk (-3%), Richemont (-6%), BMW (-7%), Enel (-5%), Bayer (-4%), Unicredit (-6%), Air France KLM (-12%), Credit Agricole (-7%)

NB: Tesla (+31%) Elon Musk hugely benefitted from Trump’s victory; so did Coinbase (+48%)

Rates

US curve (2-10 years) steepening, lowered to a mere 5bps. US 10yr yield ended the week down at 4.30%, while the 2 yr ended up at 4.25% (inflationary Trump’s economic expansion with an increased budget deficit)

Commodities

Oil price is up after OPEC+ decided to postpone its production hike until the end of December, Rafael hurricane distorts the Gulf of Mexico’s production, amid Trump’s desire to raise US oil production

Gold price corrected after 41 new record highs in 2024, impacted by higher 2yr US yield

US

ISM Services in Oct (56 vs 53.8 expected and 54.9 prior) best reading since Aug 2022; Services PMI in Oct (55 vs 55.3 expected and 54 prior)

EU

Political uncertainty in Germany with Chancellor Scholz (SPD) firing his Finance Minister (FDP) and calling for a confidence vote on Jan 15 (anticipated elections could be then held in March)

Crypto

BTC is up 10% (topped for the first time $77 000 briefly last week) due to Trump’s victory, being favourable to further deregulation of cryptos, even contemplating some cryptos in the US reserves

Nota Bene

SP500 stocks concentration, the top 10 companies in the index account for 37% of the index (10% more than in 2000): Microsoft, Apple, Nvidia, Alphabet, Amazon, Meta, Berkshire Hathaway, Eli Lilly, JPM, Broadcom

CALENDAR

WHAT ANALYSTS SAY

Goldman Sachs, 8 Nov 2024 - Briefings

The impact of Trump's election on US equities

The S&P 500 rose to a record this week after Donald Trump won the US presidential election. Equity market volatility plunged as the election outcome became known faster than traders had expected, says Brian Garrett, head of Equity Execution on the Cross Asset Sales desk in Global Banking & Markets at Goldman Sachs. US stocks surged in part because many clients had reduced the amount of risk in their portfolio amid uncertainty about the results of the election, Garrett says. Investors have since re-engaged some of the trades that were successful after the 2016 presidential race, such as buying financials, small caps, technology, and energy stocks, he says.

While US stocks rallied, European equities declined the day after the US election, as clients began to focus on the potential ramifications of US tariffs on economic growth, says Christian Mueller-Glissmann, head of asset allocation in Goldman Sachs Research.

Even though some potential Trump administration policies, such as tariffs, are seen as inflationary, commodities such as oil and copper declined. That's likely in part because many commodities are priced in US dollars, and they tend to decline when the US currency gains, Mueller-Glissmann notes. Tariffs may also be a headwind for economic growth in China, one of the world's biggest consumers of commodities.

How US tariffs could filter through global stock markets

The prospect for trade tariffs is one of the main policy implications that investors are focused on following the election of Donald Trump as US president. His policy proposals include across-the-board tariffs on imports. European indices, along with China and other emerging markets, tend to be highly sensitive to trade restrictions, according to Goldman Sachs Research. Our economists have also downgraded their forecasts for European GDP growth, reflecting the increase in trade uncertainty and the prospect for increased tariffs. By contrast, US stocks are typically less volatile relative to the broader stock market to changes in world trade.

In Europe, equity markets in Nordic countries and Germany tend to be the most vulnerable to tariffs. UK equities have defensive characteristics and the country's economy is services oriented, making it somewhat less sensitive to changes in trade. Goldman Sachs Research finds that Swiss stocks tend to be insulated to global trade because their products are technologically advanced and difficult to replace.

Machinery and equipment, pharmaceuticals, and chemicals are the Europe products with the largest shares of exports to the US, according to Goldman Sachs Research. Stock market sectors like healthcare, which are considered defensive and have high margins, tend to be less prone to swings from trade uncertainty.

The future of AI may hinge on geopolitics

The US and China are the two leaders in artificial intelligence, but the industry is global, and so is the infrastructure that makes AI possible. Building the global data centers, energy grids, and networks to sustain AI is a geopolitical test that companies and countries alike will need to pass, Jared Cohen, co-head of the Goldman Sachs Global Institute, writes in the magazine Foreign Policy.

Competition over AI has so far been dominated by debates about leading-edge semiconductors. But the next phase is also about geography and power. Where can the data centers that power AI workloads be built? And who has the capital, energy, and infrastructure needed? “The countries that work with companies to host data centers running AI workloads can gain economic, political, and technological advantages and leverage,” Cohen writes. “But data centers also present national security sensitivities, given that they often house high-end, export-controlled semiconductors and governments, businesses, and everyday users send some of their most sensitive information through them.”

The US leads the world in data centers. But while reforms and innovation can improve the domestic outlook, the energy demands of data centers may accelerate far more quickly than the capacities of America's power grid. “America cannot achieve AI autarky, especially when it comes to data centers,” Cohen writes, adding that the US will need close partners for a secure global data center buildout. Data center diplomacy will require detailed risk assessment over issues like export controls, data security and privacy, and geopolitical alignments.

Cohen identifies Canada and the Nordic countries as key data center hubs, and Japan and South Korea as important technology partners. Energy-rich countries in the Middle East like Saudi Arabia, the United Arab Emirates, and Qatar, with significant digital connectivity and the kind of flexible, longterm capital required for data center investments, are also key players. For these countries and others, Cohen writes, “the data center buildout provides an opportunity to lead in aspects of what could power the next global industrial revolution.”

UBS, 7 November 2024 - Shifting back from politics to economics

Authors: Constantin Bolz, CFA, Strategist ; Dominic Schnider, CFA, Strategist

The week ahead

Fresh from the US election and FOMC decision, where both the US dollar and US yields found support from Trump’s victory, markets will take cues from economic data releases next week, with the focus on CPI (Wednesday) and retail sales (Friday). Like with the recent US nonfarm payroll report (which showed an ongoing slowdown in hiring, albeit amid weather-related distortions), we would expect the prints to show further evidence of slowing growth.

In this context, we believe the latest US dollar rally has limits, even if the triggers for a USD reversal are not yet imminent. As we await confirmation of a “Red Sweep” to determine the impact on US fiscal dynamics and bond yields, we put our short-term FX forecasts under review. That said, the medium- to longer-term trend of fading USD strength won’t be easily derailed, not least due to the lose-lose nature of trade tariffs, which would ultimately hurt US growth and reinforce the Federal Reserve’s easing cycle. At its first meeting after the US election, the Federal Reserve made clear that monetary policy remains in restrictive territory and that they are continuing to move rates lower toward the neutral rate.

It’s early hours after the US election, and while we know that Donald Trump has won a second term as US president, the extent to which he will turn campaign rhetoric into policy is still not clear.

Obstacles to trade and higher US yields could pose significant challenges to emerging market currencies. From that perspective, the reaction so far in emerging market currencies has been rather muted, in our view. The Mexican peso, catching most of the initial pressure and at times falling more than 3% against the US dollar, ended the day after the election even slightly stronger. Dislocations currently are too small to make going outright long higher-risk emerging market currencies look attractive to us, bearing in mind the news flow we anticipate on tariffs in the coming months. We still await news from China regarding further stimulus plans, which can add an important dynamic to the emerging market outlook, as well as higher frequency economic data releases next week. The Mexican central bank will also decide on its policy rate in the coming week.

Today’s US debt-to-GDP level is twice as high as eight years ago, which limits his fiscal leeway. Furthermore, the USD is quite overvalued and the Federal Reserve has started a monetary easing cycle. During his first term, the USD was more or less fairly valued and the Fed was in tightening mode. Like the old saying “political markets have short legs,” we believe markets will soon focus on US economic data instead, primarily labor and inflation prints and their impact on Fed decisions.

In recent weeks, EURUSD pulled back as the odds of a Trump victory rose. With Trump’s re-election this week, the pair took another hit on the day, before recovering slowly. Trump’s first few speeches will certainly be market-moving, but we expect macro data to come back into focus soon, while politics fade more into the background.

We also don’t expect the breakup of the German coalition to affect the euro. The European data calendar next week is remarkably empty, with the US inflation print the most likely to move markets. However, as evidenced by the slightly better German GDP number last week, the bar is very low for European data to surprise positively. Markets have priced more than one rate cut at every European Central Bank (ECB) meeting until mid-2025. We believe that markets got a bit ahead of themselves and don't see scope for a quicker pace of easing than 25 bps at each meeting. Overall, we continue to expect a gradual recovery of the euro against the USD, while we see the remarkable stability in EURCHF around 0.94 and EURGBP around 0.83 persisting.

BlackRock, 6 November 2024 - Trump election win signals big US policy shift

Authors: Catherine Kress, Head of geopolitical research and strategy, BlackRock Investment Institute

Key views:

A Trump win opens the door for tax cuts, deregulation and tougher trade policy. House control is key. Elevated budget deficits are one factor we see pushing up inflation and long-term Treasury yields over time. We stay risk-on in U.S. equities, supported by solid growth and earnings. Yet sticky inflation and higher-for-longer interest rates could eventually challenge risk sentiment.

Former President Donald Trump has won the U.S. presidency, with Republicans retaking control of the Senate. Control of the House of Representatives – where Republicans currently hold a narrow majority – is yet undecided. Control of the House would give a second Trump administration broader powers to enact its tax, energy, trade and regulatory agenda. S&P 500 futures jumped over 2% to a record high, while the U.S. dollar rallied and U.S. bond yields jumped. We stay overweight U.S. stocks and keep our preference for the U.S. over Europe.

We focus on coming changes in fiscal policy, trade, immigration, energy, regulation – and expect a very different approach to foreign policy. Republican control of Congress is key for Trump to extend expiring Tax Cuts and Jobs Act provisions. He is likely to propose new cuts, potentially including corporate taxes. Congressional budget procedures allow deficit increases over the next decade, likely meaning persistent budget deficits – one factor we think will push up long-term Treasury yields.

On trade, Trump has proposed a wide range of tariffs, including 60% on China and 10-20% universal tariffs. He will likely make this an early priority, yet implementation is uncertain. This protectionist stance could reinforce geopolitical and economic fragmentation, a structural factor we see keeping inflation higher in the medium term. A reduction in legal immigration could impact the labor market.

Trump’s win likely means some deregulation, including rolling back banking regulations, though big tech may remain a bipartisan antitrust focus. Under Trump, we see Republicans aiming to boost energy production – though U.S. oil and gas output has already hit all-time highs, and ramping up production takes time. Scaling back parts of the Inflation Reduction Act, like electric vehicle credits, is on the agenda, but full repeal seems unlikely, in our view. We expect Trump will pursue permitting reform to expand energy infrastructure.

In the near term, we see U.S. equities supported by solid economic and corporate earnings growth, political clarity and Federal Reserve rate cuts. Longer term, much depends on how much of Trump’s agenda is enacted. We think energy, financial and tech sectors can benefit, partly from deregulation. We see multiple factors, including supply constraints like an aging workforce, keeping inflation above pre-pandemic levels. Higher-for-longer inflation and policy rates could eventually challenge risk sentiment. We are neutral long-term U.S. Treasuries and prefer medium-term maturities and some quality credit for income – but expect yields to rise over time as investors seek more compensation for the risk of holding bonds.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+37410 59-55-56

Broker

+374 43 00-43-82

broker@unibankinvest.am

research@unibankinvest.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by OJSC Unibank (registered trademark – Unibank INVEST, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.

Equities

Q3 earnings releases last week (stock WoW performance):

+++ Palantir (+42%), Berkshire Hathaway (+3%), Qualcomm (+3%), ARM Holdings (+5%), Swiss Re (+6%)

- - - Novo Nordisk (-3%), Richemont (-6%), BMW (-7%), Enel (-5%), Bayer (-4%), Unicredit (-6%), Air France KLM (-12%), Credit Agricole (-7%)

NB: Tesla (+31%) Elon Musk hugely benefitted from Trump’s victory; so did Coinbase (+48%)

Rates

US curve (2-10 years) steepening, lowered to a mere 5bps. US 10yr yield ended the week down at 4.30%, while the 2 yr ended up at 4.25% (inflationary Trump’s economic expansion with an increased budget deficit)

Commodities

Oil price is up after OPEC+ decided to postpone its production hike until the end of December, Rafael hurricane distorts the Gulf of Mexico’s production, amid Trump’s desire to raise US oil production

Gold price corrected after 41 new record highs in 2024, impacted by higher 2yr US yield

US

ISM Services in Oct (56 vs 53.8 expected and 54.9 prior) best reading since Aug 2022; Services PMI in Oct (55 vs 55.3 expected and 54 prior)

EU

Political uncertainty in Germany with Chancellor Scholz (SPD) firing his Finance Minister (FDP) and calling for a confidence vote on Jan 15 (anticipated elections could be then held in March)

Crypto

BTC is up 10% (topped for the first time $77 000 briefly last week) due to Trump’s victory, being favourable to further deregulation of cryptos, even contemplating some cryptos in the US reserves

Nota Bene

SP500 stocks concentration, the top 10 companies in the index account for 37% of the index (10% more than in 2000): Microsoft, Apple, Nvidia, Alphabet, Amazon, Meta, Berkshire Hathaway, Eli Lilly, JPM, Broadcom

CALENDAR

- Corporate earnings: US Home Depot (12 Nov), Cisco (13); Europe Astra Zeneca (12), Allianz (13), Siemens (14); China Tencent (13), Alibaba (15)

- Macro: US CPI for Oct (13 Nov); PPI Oct (14); Retail sales, Industrial production Oct (15)

- Others: US federal holiday (11 Nov) stock market open, bond market closed; Jerome Powell before the House Committee (14 Nov)

WHAT ANALYSTS SAY

- Goldman Sachs - Briefings (impact Trump’s election ; US tariffs ; the future of AI)

- UBS - Shifting back from politics to economics

- BlackRock - Trump election win signals big US policy shift

Goldman Sachs, 8 Nov 2024 - Briefings

The impact of Trump's election on US equities

The S&P 500 rose to a record this week after Donald Trump won the US presidential election. Equity market volatility plunged as the election outcome became known faster than traders had expected, says Brian Garrett, head of Equity Execution on the Cross Asset Sales desk in Global Banking & Markets at Goldman Sachs. US stocks surged in part because many clients had reduced the amount of risk in their portfolio amid uncertainty about the results of the election, Garrett says. Investors have since re-engaged some of the trades that were successful after the 2016 presidential race, such as buying financials, small caps, technology, and energy stocks, he says.

While US stocks rallied, European equities declined the day after the US election, as clients began to focus on the potential ramifications of US tariffs on economic growth, says Christian Mueller-Glissmann, head of asset allocation in Goldman Sachs Research.

Even though some potential Trump administration policies, such as tariffs, are seen as inflationary, commodities such as oil and copper declined. That's likely in part because many commodities are priced in US dollars, and they tend to decline when the US currency gains, Mueller-Glissmann notes. Tariffs may also be a headwind for economic growth in China, one of the world's biggest consumers of commodities.

How US tariffs could filter through global stock markets

The prospect for trade tariffs is one of the main policy implications that investors are focused on following the election of Donald Trump as US president. His policy proposals include across-the-board tariffs on imports. European indices, along with China and other emerging markets, tend to be highly sensitive to trade restrictions, according to Goldman Sachs Research. Our economists have also downgraded their forecasts for European GDP growth, reflecting the increase in trade uncertainty and the prospect for increased tariffs. By contrast, US stocks are typically less volatile relative to the broader stock market to changes in world trade.

In Europe, equity markets in Nordic countries and Germany tend to be the most vulnerable to tariffs. UK equities have defensive characteristics and the country's economy is services oriented, making it somewhat less sensitive to changes in trade. Goldman Sachs Research finds that Swiss stocks tend to be insulated to global trade because their products are technologically advanced and difficult to replace.

Machinery and equipment, pharmaceuticals, and chemicals are the Europe products with the largest shares of exports to the US, according to Goldman Sachs Research. Stock market sectors like healthcare, which are considered defensive and have high margins, tend to be less prone to swings from trade uncertainty.

The future of AI may hinge on geopolitics

The US and China are the two leaders in artificial intelligence, but the industry is global, and so is the infrastructure that makes AI possible. Building the global data centers, energy grids, and networks to sustain AI is a geopolitical test that companies and countries alike will need to pass, Jared Cohen, co-head of the Goldman Sachs Global Institute, writes in the magazine Foreign Policy.

Competition over AI has so far been dominated by debates about leading-edge semiconductors. But the next phase is also about geography and power. Where can the data centers that power AI workloads be built? And who has the capital, energy, and infrastructure needed? “The countries that work with companies to host data centers running AI workloads can gain economic, political, and technological advantages and leverage,” Cohen writes. “But data centers also present national security sensitivities, given that they often house high-end, export-controlled semiconductors and governments, businesses, and everyday users send some of their most sensitive information through them.”

The US leads the world in data centers. But while reforms and innovation can improve the domestic outlook, the energy demands of data centers may accelerate far more quickly than the capacities of America's power grid. “America cannot achieve AI autarky, especially when it comes to data centers,” Cohen writes, adding that the US will need close partners for a secure global data center buildout. Data center diplomacy will require detailed risk assessment over issues like export controls, data security and privacy, and geopolitical alignments.

Cohen identifies Canada and the Nordic countries as key data center hubs, and Japan and South Korea as important technology partners. Energy-rich countries in the Middle East like Saudi Arabia, the United Arab Emirates, and Qatar, with significant digital connectivity and the kind of flexible, longterm capital required for data center investments, are also key players. For these countries and others, Cohen writes, “the data center buildout provides an opportunity to lead in aspects of what could power the next global industrial revolution.”

UBS, 7 November 2024 - Shifting back from politics to economics

Authors: Constantin Bolz, CFA, Strategist ; Dominic Schnider, CFA, Strategist

The week ahead

Fresh from the US election and FOMC decision, where both the US dollar and US yields found support from Trump’s victory, markets will take cues from economic data releases next week, with the focus on CPI (Wednesday) and retail sales (Friday). Like with the recent US nonfarm payroll report (which showed an ongoing slowdown in hiring, albeit amid weather-related distortions), we would expect the prints to show further evidence of slowing growth.

In this context, we believe the latest US dollar rally has limits, even if the triggers for a USD reversal are not yet imminent. As we await confirmation of a “Red Sweep” to determine the impact on US fiscal dynamics and bond yields, we put our short-term FX forecasts under review. That said, the medium- to longer-term trend of fading USD strength won’t be easily derailed, not least due to the lose-lose nature of trade tariffs, which would ultimately hurt US growth and reinforce the Federal Reserve’s easing cycle. At its first meeting after the US election, the Federal Reserve made clear that monetary policy remains in restrictive territory and that they are continuing to move rates lower toward the neutral rate.

It’s early hours after the US election, and while we know that Donald Trump has won a second term as US president, the extent to which he will turn campaign rhetoric into policy is still not clear.

Obstacles to trade and higher US yields could pose significant challenges to emerging market currencies. From that perspective, the reaction so far in emerging market currencies has been rather muted, in our view. The Mexican peso, catching most of the initial pressure and at times falling more than 3% against the US dollar, ended the day after the election even slightly stronger. Dislocations currently are too small to make going outright long higher-risk emerging market currencies look attractive to us, bearing in mind the news flow we anticipate on tariffs in the coming months. We still await news from China regarding further stimulus plans, which can add an important dynamic to the emerging market outlook, as well as higher frequency economic data releases next week. The Mexican central bank will also decide on its policy rate in the coming week.

Today’s US debt-to-GDP level is twice as high as eight years ago, which limits his fiscal leeway. Furthermore, the USD is quite overvalued and the Federal Reserve has started a monetary easing cycle. During his first term, the USD was more or less fairly valued and the Fed was in tightening mode. Like the old saying “political markets have short legs,” we believe markets will soon focus on US economic data instead, primarily labor and inflation prints and their impact on Fed decisions.

In recent weeks, EURUSD pulled back as the odds of a Trump victory rose. With Trump’s re-election this week, the pair took another hit on the day, before recovering slowly. Trump’s first few speeches will certainly be market-moving, but we expect macro data to come back into focus soon, while politics fade more into the background.

We also don’t expect the breakup of the German coalition to affect the euro. The European data calendar next week is remarkably empty, with the US inflation print the most likely to move markets. However, as evidenced by the slightly better German GDP number last week, the bar is very low for European data to surprise positively. Markets have priced more than one rate cut at every European Central Bank (ECB) meeting until mid-2025. We believe that markets got a bit ahead of themselves and don't see scope for a quicker pace of easing than 25 bps at each meeting. Overall, we continue to expect a gradual recovery of the euro against the USD, while we see the remarkable stability in EURCHF around 0.94 and EURGBP around 0.83 persisting.

BlackRock, 6 November 2024 - Trump election win signals big US policy shift

Authors: Catherine Kress, Head of geopolitical research and strategy, BlackRock Investment Institute

Key views:

A Trump win opens the door for tax cuts, deregulation and tougher trade policy. House control is key. Elevated budget deficits are one factor we see pushing up inflation and long-term Treasury yields over time. We stay risk-on in U.S. equities, supported by solid growth and earnings. Yet sticky inflation and higher-for-longer interest rates could eventually challenge risk sentiment.

Former President Donald Trump has won the U.S. presidency, with Republicans retaking control of the Senate. Control of the House of Representatives – where Republicans currently hold a narrow majority – is yet undecided. Control of the House would give a second Trump administration broader powers to enact its tax, energy, trade and regulatory agenda. S&P 500 futures jumped over 2% to a record high, while the U.S. dollar rallied and U.S. bond yields jumped. We stay overweight U.S. stocks and keep our preference for the U.S. over Europe.

We focus on coming changes in fiscal policy, trade, immigration, energy, regulation – and expect a very different approach to foreign policy. Republican control of Congress is key for Trump to extend expiring Tax Cuts and Jobs Act provisions. He is likely to propose new cuts, potentially including corporate taxes. Congressional budget procedures allow deficit increases over the next decade, likely meaning persistent budget deficits – one factor we think will push up long-term Treasury yields.

On trade, Trump has proposed a wide range of tariffs, including 60% on China and 10-20% universal tariffs. He will likely make this an early priority, yet implementation is uncertain. This protectionist stance could reinforce geopolitical and economic fragmentation, a structural factor we see keeping inflation higher in the medium term. A reduction in legal immigration could impact the labor market.

Trump’s win likely means some deregulation, including rolling back banking regulations, though big tech may remain a bipartisan antitrust focus. Under Trump, we see Republicans aiming to boost energy production – though U.S. oil and gas output has already hit all-time highs, and ramping up production takes time. Scaling back parts of the Inflation Reduction Act, like electric vehicle credits, is on the agenda, but full repeal seems unlikely, in our view. We expect Trump will pursue permitting reform to expand energy infrastructure.

In the near term, we see U.S. equities supported by solid economic and corporate earnings growth, political clarity and Federal Reserve rate cuts. Longer term, much depends on how much of Trump’s agenda is enacted. We think energy, financial and tech sectors can benefit, partly from deregulation. We see multiple factors, including supply constraints like an aging workforce, keeping inflation above pre-pandemic levels. Higher-for-longer inflation and policy rates could eventually challenge risk sentiment. We are neutral long-term U.S. Treasuries and prefer medium-term maturities and some quality credit for income – but expect yields to rise over time as investors seek more compensation for the risk of holding bonds.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+37410 59-55-56

Broker

+374 43 00-43-82

broker@unibankinvest.am

research@unibankinvest.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by OJSC Unibank (registered trademark – Unibank INVEST, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.