Last week: US July inflation and Nvidia Q2 results as expected; French PM’s confidence’s vote on 8 Sep hit EuroStoxx 50

WEEKLY TRENDS

WEEKLY TRENDS

- Summer ended on a weaker note last Friday (take profits after ATH for BTC and US stocks). In India and in France, stocks were impacted as US tariffs kicked in for India at 50% and France’s PM’s confidence will be put at high risk on Sep the 8th with a no confidence vote that looks almost certain now. China stock index was the big winner last week and in August too (Hedge Funds are taking large positions there)

- Nvidia’s long awaited Q2 earnings showed slightly better than forecast revenues and outlook

- Trump’s new gamble on the FED (firing governor Lisa Cook) agitated the markets and questioned the FED’s independence

- Investors will focus on the US August Job report release on Friday, after the recent revision debacle we had (Trump firing BLS’s head)

- Note that a local US appeal court decided that Trump’s new tariffs were illegal but its ruling may possibly be implemented on October 14 only.

MARKETS

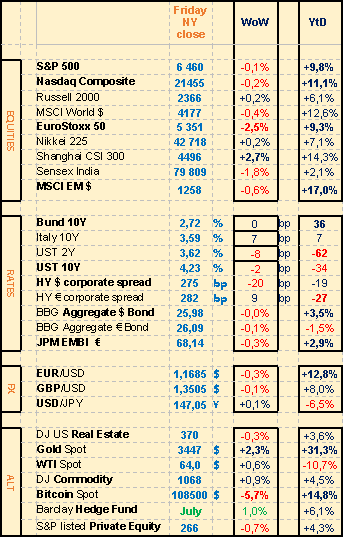

Equities

Earnings released stock weekly performances:

Nvidia (-2%), MongoDB (+44%), Vinci (-9%), Pernod Ricard (-4%)

Pure Storage (+33%), Snowflake (+21%), BioArctic (+25%)

Valneva (-24%) US FDA suspended its licence (Chikungunya vaccine)

M&A:

Puma (+14%) Pinault due to sell its 29% share; Nikon (+15%) interest from Essilor Luxottica

Analysts: Rolls Royce Hold (MS ‘o/w’ target £12.75), Renault (Citi ‘buy’ target €42), Schneider Elec (JPM ‘neutral’ target €220)

Rates

US curve (2-10 years) steepening slightly up at 60bps (+5). US Bond yields slightly lower.

HY corporate spreads lower for US at 275bps (-20) higher for EU at 285bps (+10)

Commodities

Oil price stable (+0.5%) 50% tariffs on India, lower US inventories

Gold price higher (+2.5%) on lower US yields and FED governance issue

NB: Robusta is at a 3 months high, Arabica much higher too

US

July PCE inflation as expected at 2.6% YoY (Core at 2.9% vs 2.8% prior)

Q2 GPD growth revised at +3.3%

Crypto

BTC second week lower at –5.5% (after ATH at $124500 on 14 Aug)

Under the watch

France-Italy Bond yields convergence (10 year yield difference remains below 10bps)

Nota Bene

US equity mutual funds cash at record low (1.4%) not much dry powder

CALENDAR

Earnings releases:

US Salesforce, HP (3 Sep), Broadcom (4)

EU bioMérieux (4 Sep)

Macro releases:

US August NFP job report (5 Sep)

China Aug PMI (31 Aug), Caixin PMI (3 Sep)

Upcoming central bank meetings:

ECB (11 Sep), FED/FOMC (17 Sep), BOE/MPC (18 Sep)

WHAT ANALYSTS SAY

CME Group, 26 August 2025

The Equity/Oil relationship has undergone fundamental changes

Statistical evidence shows that oil demand is highly correlated with the performance of the global economy. In the past, the price of a barrel of oil also closely tracked changes in consumption. To a certain extent, OPEC once acted as both judge and jury of the oil balance, reducing output in times of weak demand and increasing it when demand rose – a delicate balancing act that ensured the market was never oversupplied for a prolonged period.

As a result, during both economic booms (such as China’s emergence on the global stage between 2003 and 2008) and downturns (such as the 2007 – 2008 recession), the relationship between stock indices and oil, remained relatively stable. Between 2005 and 2013, for example, one unit of the Nasdaq Index was worth between 30 and 40 barrels of WTI, while for the global equity index, this quotient fluctuated between 3 and 6.

Then came the U.S. shale revolution around 2014 – 2015. OPEC lost much of its pricing power, and the supply-demand balance became increasingly determined by market forces rather than coordinated output policies. In times of oversupply, such as during the Russian-Saudi price war in early 2020, the ratio spiked as oil prices collapsed while the broader economy continued its recovery from the health crisis. The Russian-Ukrainian war triggered a short-lived fear of recession and supply disruption, during which equities temporarily became cheaper relative to oil.

Nonetheless, the underlying trend is clear : Rising supply from outside the producer alliance prevents the oil balance from tightening meaningfully, regardless of economic conditions or oil demand. As a result, the equity-oil ratio has climbed relentlessly. This effect has been particularly pronounced in the Nasdaq Index, amplified by the spectacular rise of AI-driven technology stocks. Whereas 15 – 20 years ago the ratio stood at 30 – 40, it is now well above 300.

Is this the new status quo, or could reverting to the earlier mean occur over a prolonged period? The change observed over the past decade appears to represent a structural shift in equities, driven by the dominance of technology and largely disconnected from commodity cycles.

On the supply side, robust U.S. shale production, rising non-OPEC output, and renewed investment in exploration and production – spurred by the slower-than-expected transition from fossil fuels to renewables – suggest that the divergence between equities and oil, notwithstanding occasional brief corrections, such as the one experienced in tech stocks at the time of writing around August 20, will continue unabated.

Wisdom Tree, 28 August 2025

Author: Mobeen Tahir, Associate Director, Research

Large technology companies are facing a challenge, how to sustainably power data centres, the backbone of modern energy-intensive technologies, including artificial intelligence (AI) and digital assets. The tech giants behind the growth of these data centres now see nuclear energy as a sustainable solution.

Microsoft

Microsoft signed an agreement with Constellation Energy to restart the Three Mile Island nuclear power plant. Unit 1, which ceased operations in 2019, could restart as early as 2027. This agreement will provide nuclear power to Microsoft's data centres for two decades. When the agreement was announced, Constellation's CEO said: ‘This decision is the most powerful symbol of the renaissance of nuclear energy as a clean and reliable energy resource.’

Alphabet (Google)

Alphabet is partnering with Kairos Power to implement small modular reactors (SMRs). The agreement provides for the development and deployment of up to 500 megawatts (MW) of SMR capacity by the early 2030s. Google's plan to deploy 6 to 7 SMRs significantly boosts the credibility of this technology. The company aims to reduce the cost of nuclear power and ensure reliable, carbon-free energy for its AI and cloud operations.

Amazon

Amazon has signed several agreements to secure its nuclear energy supply. Amazon is partnering with Energy Northwest to build two SMR facilities in Washington State that are expected to produce 320 MW of clean energy (with an option to expand to 960 MW in the future). The company is also collaborating with X-energy to commercialise the Xe-100 technology, a small, high-temperature, gas-cooled modular reactor that guarantees reliable, carbon-free electricity. In addition, it has entered into a long-term partnership with Dominion Energy to power its Amazon Web Services data centres in Virginia with carbon-free electricity from existing nuclear power plants. Finally, Amazon has partnered with Talen Energy to build a data centre adjacent to Talen's Susquehanna nuclear plant in Pennsylvania, taking advantage of existing zero-carbon energy.

Meta

Meta has signed a contract with Constellation Energy for the Clinton Clean Energy Centre. Starting in 2027, this agreement will provide carbon-free electricity for 20 years. It will increase the capacity of the Clinton plant by approximately 30 MW and meet Meta's long-term energy needs for its AI-related activities.

Palantir

Palantir has announced a £100m agreement with Nuclear Company to develop a Nuclear Operating System (NOS) that manages reactor construction through its Foundry platform. The system supports supply chain, permitting, safety and progress control, aims to reduce delays and costs while increasing reliability.

Equinix

This month, Equinix announced the conclusion of several advanced nuclear agreements. Equinix is a global company specialising in data centres and digital infrastructure, supporting customers in the cloud, networking and enterprise worlds. It will collaborate with Oklo on a 500 MW agreement for innovative nuclear reactors for its data centres. It has also pre-ordered 20 Radiant micro reactors to provide clean, flexible, on-site energy. In addition, the company has entered into agreements with ULC-Energy and Stellaria, two next-generation nuclear energy developers, to purchase electricity on the European market.

Raiffeisen, 28 August 2025

Author: Geoffroy Brochard, Investment Advisor

When defence creates value

In turbulent times, the strongest companies are not necessarily the ones that make the most noise. Some, more discreet, draw their strength from what analysts call ‘moats’: those sustainable competitive advantages that make their model difficult to replicate. Whether in the form of patents, technological expertise, network effects, closed ecosystems or powerful brands, these are all barriers to entry that enable these companies to maintain their position, generally over the long term. These protections do not guarantee rapid growth, but they do ensure stable profitability, visibility on cash flows and greater resilience to macroeconomic uncertainties. In a world of uncertainty, the ability to preserve what has been built becomes a rare and valuable quality.

Defensive strategies that pay off

Depending on the sector, moats take very different forms. In the pharmaceutical industry, patents protect molecules for more than ten years, giving companies valuable time to make their research profitable. In manufacturing, ASML dominates the production of lithography machines thanks to its unrivalled technological expertise. In Switzerland, VAT Group has established itself in the vacuum valve market with a lead that is difficult to catch up with. In the consumer and luxury goods sector, brands such as Nestlé, LVMH and Hermès rely on their reputation, controlled distribution and well-crafted storytelling. This results in a loyal customer base, the ability to set prices, solid margins and a certain financial stability that transcends economic cycles.

An advantage that takes work

No moat is permanent. Innovation, regulation, changing habits or technology can all disrupt a model. A patent may expire, a brand may go out of fashion, or an emerging player may change the rules of the game. Even network effects can be reversed: a loss of user confidence can quickly overturn a previously dominant model. This is why a competitive advantage must be maintained, adapted and sometimes even redefined. It is not its size that matters, but rather its relevance over time. Successful companies are not just those that have a bulwark: they are those that ensure that it remains useful, solid and difficult to breach.

Between perceived quality and market reality

Even the best companies can disappoint if they are bought at too high a price. The performance of an investment depends as much on the strength of the model as on the valuation at the time of entry. The market may overestimate an advantage, with the price already factoring in years of future success. Conversely, some robust models may be temporarily undervalued due to scepticism or excessive caution. For long-term investors, opportunity arises from this imbalance. The best prospects are found in the combination of an established moat and reasonable valuation. These companies weather cycles with rare consistency while providing portfolios with a form of resilience that, over time, often translates into performance.

Equities

Earnings released stock weekly performances:

Nvidia (-2%), MongoDB (+44%), Vinci (-9%), Pernod Ricard (-4%)

Pure Storage (+33%), Snowflake (+21%), BioArctic (+25%)

Valneva (-24%) US FDA suspended its licence (Chikungunya vaccine)

M&A:

Puma (+14%) Pinault due to sell its 29% share; Nikon (+15%) interest from Essilor Luxottica

Analysts: Rolls Royce Hold (MS ‘o/w’ target £12.75), Renault (Citi ‘buy’ target €42), Schneider Elec (JPM ‘neutral’ target €220)

Rates

US curve (2-10 years) steepening slightly up at 60bps (+5). US Bond yields slightly lower.

HY corporate spreads lower for US at 275bps (-20) higher for EU at 285bps (+10)

Commodities

Oil price stable (+0.5%) 50% tariffs on India, lower US inventories

Gold price higher (+2.5%) on lower US yields and FED governance issue

NB: Robusta is at a 3 months high, Arabica much higher too

US

July PCE inflation as expected at 2.6% YoY (Core at 2.9% vs 2.8% prior)

Q2 GPD growth revised at +3.3%

Crypto

BTC second week lower at –5.5% (after ATH at $124500 on 14 Aug)

Under the watch

France-Italy Bond yields convergence (10 year yield difference remains below 10bps)

Nota Bene

US equity mutual funds cash at record low (1.4%) not much dry powder

CALENDAR

Earnings releases:

US Salesforce, HP (3 Sep), Broadcom (4)

EU bioMérieux (4 Sep)

Macro releases:

US August NFP job report (5 Sep)

China Aug PMI (31 Aug), Caixin PMI (3 Sep)

Upcoming central bank meetings:

ECB (11 Sep), FED/FOMC (17 Sep), BOE/MPC (18 Sep)

WHAT ANALYSTS SAY

- CME Group

- Wisdom Tree

- Raiffeisen

CME Group, 26 August 2025

The Equity/Oil relationship has undergone fundamental changes

Statistical evidence shows that oil demand is highly correlated with the performance of the global economy. In the past, the price of a barrel of oil also closely tracked changes in consumption. To a certain extent, OPEC once acted as both judge and jury of the oil balance, reducing output in times of weak demand and increasing it when demand rose – a delicate balancing act that ensured the market was never oversupplied for a prolonged period.

As a result, during both economic booms (such as China’s emergence on the global stage between 2003 and 2008) and downturns (such as the 2007 – 2008 recession), the relationship between stock indices and oil, remained relatively stable. Between 2005 and 2013, for example, one unit of the Nasdaq Index was worth between 30 and 40 barrels of WTI, while for the global equity index, this quotient fluctuated between 3 and 6.

Then came the U.S. shale revolution around 2014 – 2015. OPEC lost much of its pricing power, and the supply-demand balance became increasingly determined by market forces rather than coordinated output policies. In times of oversupply, such as during the Russian-Saudi price war in early 2020, the ratio spiked as oil prices collapsed while the broader economy continued its recovery from the health crisis. The Russian-Ukrainian war triggered a short-lived fear of recession and supply disruption, during which equities temporarily became cheaper relative to oil.

Nonetheless, the underlying trend is clear : Rising supply from outside the producer alliance prevents the oil balance from tightening meaningfully, regardless of economic conditions or oil demand. As a result, the equity-oil ratio has climbed relentlessly. This effect has been particularly pronounced in the Nasdaq Index, amplified by the spectacular rise of AI-driven technology stocks. Whereas 15 – 20 years ago the ratio stood at 30 – 40, it is now well above 300.

Is this the new status quo, or could reverting to the earlier mean occur over a prolonged period? The change observed over the past decade appears to represent a structural shift in equities, driven by the dominance of technology and largely disconnected from commodity cycles.

On the supply side, robust U.S. shale production, rising non-OPEC output, and renewed investment in exploration and production – spurred by the slower-than-expected transition from fossil fuels to renewables – suggest that the divergence between equities and oil, notwithstanding occasional brief corrections, such as the one experienced in tech stocks at the time of writing around August 20, will continue unabated.

Wisdom Tree, 28 August 2025

Author: Mobeen Tahir, Associate Director, Research

Large technology companies are facing a challenge, how to sustainably power data centres, the backbone of modern energy-intensive technologies, including artificial intelligence (AI) and digital assets. The tech giants behind the growth of these data centres now see nuclear energy as a sustainable solution.

Microsoft

Microsoft signed an agreement with Constellation Energy to restart the Three Mile Island nuclear power plant. Unit 1, which ceased operations in 2019, could restart as early as 2027. This agreement will provide nuclear power to Microsoft's data centres for two decades. When the agreement was announced, Constellation's CEO said: ‘This decision is the most powerful symbol of the renaissance of nuclear energy as a clean and reliable energy resource.’

Alphabet (Google)

Alphabet is partnering with Kairos Power to implement small modular reactors (SMRs). The agreement provides for the development and deployment of up to 500 megawatts (MW) of SMR capacity by the early 2030s. Google's plan to deploy 6 to 7 SMRs significantly boosts the credibility of this technology. The company aims to reduce the cost of nuclear power and ensure reliable, carbon-free energy for its AI and cloud operations.

Amazon

Amazon has signed several agreements to secure its nuclear energy supply. Amazon is partnering with Energy Northwest to build two SMR facilities in Washington State that are expected to produce 320 MW of clean energy (with an option to expand to 960 MW in the future). The company is also collaborating with X-energy to commercialise the Xe-100 technology, a small, high-temperature, gas-cooled modular reactor that guarantees reliable, carbon-free electricity. In addition, it has entered into a long-term partnership with Dominion Energy to power its Amazon Web Services data centres in Virginia with carbon-free electricity from existing nuclear power plants. Finally, Amazon has partnered with Talen Energy to build a data centre adjacent to Talen's Susquehanna nuclear plant in Pennsylvania, taking advantage of existing zero-carbon energy.

Meta

Meta has signed a contract with Constellation Energy for the Clinton Clean Energy Centre. Starting in 2027, this agreement will provide carbon-free electricity for 20 years. It will increase the capacity of the Clinton plant by approximately 30 MW and meet Meta's long-term energy needs for its AI-related activities.

Palantir

Palantir has announced a £100m agreement with Nuclear Company to develop a Nuclear Operating System (NOS) that manages reactor construction through its Foundry platform. The system supports supply chain, permitting, safety and progress control, aims to reduce delays and costs while increasing reliability.

Equinix

This month, Equinix announced the conclusion of several advanced nuclear agreements. Equinix is a global company specialising in data centres and digital infrastructure, supporting customers in the cloud, networking and enterprise worlds. It will collaborate with Oklo on a 500 MW agreement for innovative nuclear reactors for its data centres. It has also pre-ordered 20 Radiant micro reactors to provide clean, flexible, on-site energy. In addition, the company has entered into agreements with ULC-Energy and Stellaria, two next-generation nuclear energy developers, to purchase electricity on the European market.

Raiffeisen, 28 August 2025

Author: Geoffroy Brochard, Investment Advisor

When defence creates value

In turbulent times, the strongest companies are not necessarily the ones that make the most noise. Some, more discreet, draw their strength from what analysts call ‘moats’: those sustainable competitive advantages that make their model difficult to replicate. Whether in the form of patents, technological expertise, network effects, closed ecosystems or powerful brands, these are all barriers to entry that enable these companies to maintain their position, generally over the long term. These protections do not guarantee rapid growth, but they do ensure stable profitability, visibility on cash flows and greater resilience to macroeconomic uncertainties. In a world of uncertainty, the ability to preserve what has been built becomes a rare and valuable quality.

Defensive strategies that pay off

Depending on the sector, moats take very different forms. In the pharmaceutical industry, patents protect molecules for more than ten years, giving companies valuable time to make their research profitable. In manufacturing, ASML dominates the production of lithography machines thanks to its unrivalled technological expertise. In Switzerland, VAT Group has established itself in the vacuum valve market with a lead that is difficult to catch up with. In the consumer and luxury goods sector, brands such as Nestlé, LVMH and Hermès rely on their reputation, controlled distribution and well-crafted storytelling. This results in a loyal customer base, the ability to set prices, solid margins and a certain financial stability that transcends economic cycles.

An advantage that takes work

No moat is permanent. Innovation, regulation, changing habits or technology can all disrupt a model. A patent may expire, a brand may go out of fashion, or an emerging player may change the rules of the game. Even network effects can be reversed: a loss of user confidence can quickly overturn a previously dominant model. This is why a competitive advantage must be maintained, adapted and sometimes even redefined. It is not its size that matters, but rather its relevance over time. Successful companies are not just those that have a bulwark: they are those that ensure that it remains useful, solid and difficult to breach.

Between perceived quality and market reality

Even the best companies can disappoint if they are bought at too high a price. The performance of an investment depends as much on the strength of the model as on the valuation at the time of entry. The market may overestimate an advantage, with the price already factoring in years of future success. Conversely, some robust models may be temporarily undervalued due to scepticism or excessive caution. For long-term investors, opportunity arises from this imbalance. The best prospects are found in the combination of an established moat and reasonable valuation. These companies weather cycles with rare consistency while providing portfolios with a form of resilience that, over time, often translates into performance.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+374 43 00-43-82

Broker

broker@unibankinvest.am

research@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.