Last week: 2 weeks war with Iran (inflation fears, growth reduction) lower stock indices, higher yields/credit margins

WEEKLY TRENDS

WEEKLY TRENDS

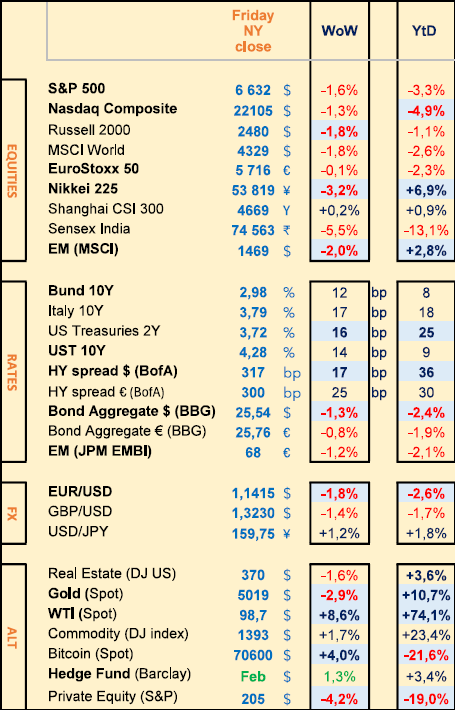

- Inflation fears and slower growth concerns after 15 days of war with Iran, continued to push Bond yields up (UST2Y up 25bps YTD) and marked down stock indices (Nasdaq is down -5% YTD). Technically, all the major US stock indices are trading just above their 200 Daily Moving Averages

- Investors are hedging against an S&P500 crash (Put Delta positioning is at a record high of $70bn)

- Private Credit concerns continued with Cliffwater $33bn private credit fund adding to the already long list of private credit funds that have capped their redemptions (Blue Owl, Blackstone, BlackRock and JP Morgan Chase)

- During those past weeks, the USD has raised significantly as a safe haven, impacting Gold price

- Crude Oil is still skyrocketing ($100 a barrel). The G7 have planned for their largest oil reserve release in history (400m barrels, or 32% of the current IEA reserves, at 1.24bn)

- Next week’s Central Banks’ meetings shall be under scrutiny (at least the governors’ speeches will be) with the FED, ECB, BOE, RBA, BOC and the SNB. Note that the Futures market now discounts only one FED rate cut this year (in September).

MARKETS

Equities

Q4 earnings weekly performances:

Oracle (+3%), Adobe (-11%), Inditex (+3%), Shell (+5%)

NB weekly: Soitec (+41%), BE Semi (+18%), JCDecaux (+18%), Zalando (+16%), Canal + (-23%), ID Logistics (-12%), Eurazeo (-9%)

Bank analysts: Hermès (HSBC ‘buy’ target €2350), Kering (HSBC ‘buy’ target €310), LVMH (HSBC ‘buy’ target €705), BNP (JPM ‘o/w’ target €106), Schneider Elec (GS ‘buy’ target €322), Bouygues (JPM ‘o/w’ target €62)

Rates

US curve steepening (2-10 years) stable at +56bps

HY corp. spreads higher : US at +315bps (+15); EU at +300bps (+25)

Commodities

Oil price higher (+9% WoW) due to the Hormuz strait closure (NB. US lifted some of its sanctions against Russian oil for 30 days until April 11)

Gold price lower (-3% WoW), Silver, Copper, US Natural Gas (flat on the week), TTF Gas (-21%), Steel (+2%), Aluminium (+2%)

US

Feb CPI at +2.4% (Core at +2.5%), Jan PCE at +2.8% vs +2.9% prior

Q4 GDP second estimate at +0.7% vs +1.4% expected

Crypto

BTC (+4% WoW). NB. Strategy (M. Saylor) bought 1360 BTC last week, Bitmine Imm Tech (T. Lee) bought 61000 ETH last week

Under the watch

Private Credit - after BlackRock, Blackstone, JP Morgan Chase, Blue Owl, it is now the turn of Cliffwater that had to cap redemptions (all around 5%). Investors want to redeem more than scheduled and this forces Private Credit Managers to sell loans to raise liquidity in an illiquid market by definition (leading to the marking down of portfolios at new lower traded market values)

Nota Bene

Financials are the worst performing sector in the S&P500 YTD (-11%)

CALENDAR

Earnings releases:

EU Vinci (17 March), Enel (19), Atlas Copco (20)

CB meetings:

RBA (17 March), BOC, FED/FOMC (18), BOE/MPC, ECB, SNB (19)

WHAT ANALYSTS SAY

DWS, 13 March 2026

Author: Christian Scherrmann, US Economist

It is difficult to imagine that US Federal Reserve officials will make any major changes to their monetary policy at their next meeting.

The latest data show that inflation remains high, but that it has not been significantly driven by tariffs.

The narrative that inflation is ‘transitory’ is therefore likely to persist.

The recent Supreme Court ruling also suggests a reduction in uncertainty regarding trade policy, and perhaps even a slight fall in average tariffs.

Despite the volatility seen at the start of the year, the labour market continues to ease slightly. With an unemployment rate of 4.4%, there is little inflationary pressure from that quarter.

The outlook becomes more complex when considering the geopolitical situation.

The escalation in the Middle East and the sharp rise in oil prices pose an additional risk. Central banks generally view these energy shocks as a temporary impulse. Historically, these have generally been short-lived. In some cases, they even have a dampening effect on underlying inflationary trends, as rising energy costs reduce household purchasing power and curb demand for other goods.

The problem arises only when high energy prices persist over a long period. In this case, households and businesses might anticipate a general rise in prices. Energy prices can affect underlying inflation through second-round effects, such as wage demands, higher transport costs or broader cost pass-through. The 1970s and early 1980s provide a historical example: repeated oil shocks reinforced inflationary expectations and forced the US Federal Reserve, under the leadership of Paul Volcker, to tighten monetary policy drastically, leading to deep recessions.

Today, however, the US economy is significantly less dependent on oil than it was back then. This reduces the likelihood that energy price shocks will quickly translate into sustained higher inflation.

There is currently no question of second-round effects, and a monetary policy response this month would in any case do little to alter the geopolitical landscape. We therefore expect the US Federal Reserve to keep interest rates unchanged. The markets are thus focusing on the updated forecasts in March.

The usual picture is likely to be confirmed: higher expectations for headline inflation, but little change for core inflation, the labour market and economic growth.

Currently, forecasts point to just one interest rate cut for the current year, and this is precisely what the market will be watching: whether this interest rate cut will be maintained or whether it will already be reversed by central bankers.

DNB AM, 12 March 2026

Author: Anesa Mulabecirovic Sahnoun, Healthcare Analyst

The market for obesity treatments remains one of the most attractive areas of structural growth in the global healthcare sector. Demand continues to outstrip supply, and forecasts predict a market size exceeding $100bn by the end of the decade. For investors, the growth potential remains intact, but the focus is shifting from supply scarcity to competition, production capacity, price pressure and product differentiation. Eli Lilly is currently regarded as the company with the strongest short-term momentum and the most robust clinical leadership, thanks to its robust earnings growth and expanding pipeline of oral products. Novo Nordisk, by contrast, is in a transitional phase characterised by increased competition, price adjustments and reliance on the semaglutide franchise. This follows a significant re-rating of its market capitalisation, which has fallen from a peak of around $467bn in December 2023 to around $156bn today. Whilst Eli Lilly appears to be the company offering the best visibility in terms of growth, Novo Nordisk represents an opportunity for recovery based on data and execution. In an increasingly competitive environment, long-term leadership will be determined less by market size than by clinical results, tolerability, access and pricing discipline.

We are already seeing a shift from injections to tablets. Novo Nordisk’s oral medication Wegovy was launched at the start of the year, and Eli Lilly’s oral GLP-1 is expected to be approved in April and then brought to market. Oral therapies are expanding the market by lowering barriers to treatment initiation and enabling wider use in primary care and in the early stages of the disease. The industry estimates that oral GLP-1 treatments could eventually capture around 20–25% of the global GLP-1 market, whilst injectable formulations are expected to retain the largest market share due to their greater efficacy and longer duration of action. However, tablets could also intensify price competition and alter the product range within this category.

There is always a risk that increased scrutiny of doctors and payers will lead to stricter prescribing criteria and usage controls. One point of discussion is the loss of lean muscle mass alongside fat reduction. The loss of muscle mass may be clinically relevant, as muscles are important for metabolism, strength and general health. This has led to a focus on the ‘quality of weight loss’ rather than its extent. Consequently, the industry is developing next-generation therapeutic combinations aimed at preserving muscle mass, potentially creating a $5–10bn niche for complementary muscle-preserving therapies. Overall, this is more a sign of market maturation than a structural weakening of demand.

The opportunities are vast and innovation is advancing, but the barriers to entry are high.

Novo Nordisk and Eli Lilly benefit from their scale, production capacity, established relationships with payers and extensive experience. The current duopoly is expected to remain largely intact until new, differentiated products enter the market later this decade.

Ultimately, if competitors manage to demonstrate superior efficacy, better tolerability, more convenient dosing or more competitive pricing, market shares could shift. The market for obesity drugs remains structurally attractive, but it has entered a phase of heightened competition, where pricing, access and clinical differentiation will determine the long-term winners.

Adams Street Partners, 12 March 2026

Authors: 2026 Global Investor Survey

Adams Street Partners ‘Global Investor Survey 2026’ highlights a shift in investors’ behaviour in the private sector

· 90% of Limited Partners (LPs) believe that liquidity constraints will shape their strategy in 2026

· Europe has overtaken North America as the most attractive region for investors

· Concerns about tech disruption, investors expect managers to integrate AI into sourcing, due diligence and portfolio management

Liquidity is becoming central to strategy

Liquidity constraints are now the main challenge for private market investors. Nearly 90% of respondents believe that liquidity pressures will influence their strategy in 2026, and two-thirds anticipate a moderate or significant impact. Whilst distributions remain below historical norms, LPs are increasingly turning to secondary markets, particularly continuation vehicles, to manage their cash flows and rebalance their portfolios. Co-investments are also gaining popularity, offering direct access to quality assets at a lower overall cost. Against this backdrop of reduced liquidity, fundraising has slowed and fewer LPs are increasing their commitments to existing managers – just 53% compared to 67% previously – whilst appetite for new managers has fallen to its lowest level in five years.

In response, investors are focusing their capital on managers capable of generating repeatable alpha, with in-depth sector expertise and strong alignment of interests. Governance remains a key factor: 85% of LPs consider management team incentive structures to be a significant driver of outperformance in private markets.

Europe overtakes North America for the first time

One of the survey’s most striking findings is that Europe will overtake North America as the most attractive region for private market investments by 2026. Investors cite attractive valuations, government support and opportunities in the European mid-market as the main factors. Although North America remains at the heart of many portfolios, geopolitical tensions and concentration risks are prompting LPs to further diversify their geographical exposures. At the same time, geopolitical risk is becoming a major strategic consideration: nearly nine in ten LPs expect it to significantly influence private markets strategies, particularly due to tensions between the US and China.

AI is becoming an indispensable capability

Artificial intelligence is rapidly evolving from an investment theme into an operational requirement. Technological disruption is now cited by 28% of LPs as a major risk, up from 17% last year, illustrating the growing impact of AI on valuations, competition and business models. At the same time, technology and healthcare rank among the most attractive sectors for 2026, alongside co-investments, each cited by 39% of respondents. AI is no longer merely a differentiating factor, it has become a genuine driver of value creation. Investors expect managers not only to identify companies using AI, but also to integrate these technologies into their own processes, from sourcing through due diligence to the operational management of portfolios.”

Equities

Q4 earnings weekly performances:

Oracle (+3%), Adobe (-11%), Inditex (+3%), Shell (+5%)

NB weekly: Soitec (+41%), BE Semi (+18%), JCDecaux (+18%), Zalando (+16%), Canal + (-23%), ID Logistics (-12%), Eurazeo (-9%)

Bank analysts: Hermès (HSBC ‘buy’ target €2350), Kering (HSBC ‘buy’ target €310), LVMH (HSBC ‘buy’ target €705), BNP (JPM ‘o/w’ target €106), Schneider Elec (GS ‘buy’ target €322), Bouygues (JPM ‘o/w’ target €62)

Rates

US curve steepening (2-10 years) stable at +56bps

HY corp. spreads higher : US at +315bps (+15); EU at +300bps (+25)

Commodities

Oil price higher (+9% WoW) due to the Hormuz strait closure (NB. US lifted some of its sanctions against Russian oil for 30 days until April 11)

Gold price lower (-3% WoW), Silver, Copper, US Natural Gas (flat on the week), TTF Gas (-21%), Steel (+2%), Aluminium (+2%)

US

Feb CPI at +2.4% (Core at +2.5%), Jan PCE at +2.8% vs +2.9% prior

Q4 GDP second estimate at +0.7% vs +1.4% expected

Crypto

BTC (+4% WoW). NB. Strategy (M. Saylor) bought 1360 BTC last week, Bitmine Imm Tech (T. Lee) bought 61000 ETH last week

Under the watch

Private Credit - after BlackRock, Blackstone, JP Morgan Chase, Blue Owl, it is now the turn of Cliffwater that had to cap redemptions (all around 5%). Investors want to redeem more than scheduled and this forces Private Credit Managers to sell loans to raise liquidity in an illiquid market by definition (leading to the marking down of portfolios at new lower traded market values)

Nota Bene

Financials are the worst performing sector in the S&P500 YTD (-11%)

CALENDAR

Earnings releases:

EU Vinci (17 March), Enel (19), Atlas Copco (20)

CB meetings:

RBA (17 March), BOC, FED/FOMC (18), BOE/MPC, ECB, SNB (19)

WHAT ANALYSTS SAY

- DWS: US inflation remains high but has not been significantly driven by tariffs

- DNB: The market for weight-loss products will soon be worth over $100 bn

- Adams Street Partners: Global Investor Survey - a major realignment in the private sector

DWS, 13 March 2026

Author: Christian Scherrmann, US Economist

It is difficult to imagine that US Federal Reserve officials will make any major changes to their monetary policy at their next meeting.

The latest data show that inflation remains high, but that it has not been significantly driven by tariffs.

The narrative that inflation is ‘transitory’ is therefore likely to persist.

The recent Supreme Court ruling also suggests a reduction in uncertainty regarding trade policy, and perhaps even a slight fall in average tariffs.

Despite the volatility seen at the start of the year, the labour market continues to ease slightly. With an unemployment rate of 4.4%, there is little inflationary pressure from that quarter.

The outlook becomes more complex when considering the geopolitical situation.

The escalation in the Middle East and the sharp rise in oil prices pose an additional risk. Central banks generally view these energy shocks as a temporary impulse. Historically, these have generally been short-lived. In some cases, they even have a dampening effect on underlying inflationary trends, as rising energy costs reduce household purchasing power and curb demand for other goods.

The problem arises only when high energy prices persist over a long period. In this case, households and businesses might anticipate a general rise in prices. Energy prices can affect underlying inflation through second-round effects, such as wage demands, higher transport costs or broader cost pass-through. The 1970s and early 1980s provide a historical example: repeated oil shocks reinforced inflationary expectations and forced the US Federal Reserve, under the leadership of Paul Volcker, to tighten monetary policy drastically, leading to deep recessions.

Today, however, the US economy is significantly less dependent on oil than it was back then. This reduces the likelihood that energy price shocks will quickly translate into sustained higher inflation.

There is currently no question of second-round effects, and a monetary policy response this month would in any case do little to alter the geopolitical landscape. We therefore expect the US Federal Reserve to keep interest rates unchanged. The markets are thus focusing on the updated forecasts in March.

The usual picture is likely to be confirmed: higher expectations for headline inflation, but little change for core inflation, the labour market and economic growth.

Currently, forecasts point to just one interest rate cut for the current year, and this is precisely what the market will be watching: whether this interest rate cut will be maintained or whether it will already be reversed by central bankers.

DNB AM, 12 March 2026

Author: Anesa Mulabecirovic Sahnoun, Healthcare Analyst

The market for obesity treatments remains one of the most attractive areas of structural growth in the global healthcare sector. Demand continues to outstrip supply, and forecasts predict a market size exceeding $100bn by the end of the decade. For investors, the growth potential remains intact, but the focus is shifting from supply scarcity to competition, production capacity, price pressure and product differentiation. Eli Lilly is currently regarded as the company with the strongest short-term momentum and the most robust clinical leadership, thanks to its robust earnings growth and expanding pipeline of oral products. Novo Nordisk, by contrast, is in a transitional phase characterised by increased competition, price adjustments and reliance on the semaglutide franchise. This follows a significant re-rating of its market capitalisation, which has fallen from a peak of around $467bn in December 2023 to around $156bn today. Whilst Eli Lilly appears to be the company offering the best visibility in terms of growth, Novo Nordisk represents an opportunity for recovery based on data and execution. In an increasingly competitive environment, long-term leadership will be determined less by market size than by clinical results, tolerability, access and pricing discipline.

We are already seeing a shift from injections to tablets. Novo Nordisk’s oral medication Wegovy was launched at the start of the year, and Eli Lilly’s oral GLP-1 is expected to be approved in April and then brought to market. Oral therapies are expanding the market by lowering barriers to treatment initiation and enabling wider use in primary care and in the early stages of the disease. The industry estimates that oral GLP-1 treatments could eventually capture around 20–25% of the global GLP-1 market, whilst injectable formulations are expected to retain the largest market share due to their greater efficacy and longer duration of action. However, tablets could also intensify price competition and alter the product range within this category.

There is always a risk that increased scrutiny of doctors and payers will lead to stricter prescribing criteria and usage controls. One point of discussion is the loss of lean muscle mass alongside fat reduction. The loss of muscle mass may be clinically relevant, as muscles are important for metabolism, strength and general health. This has led to a focus on the ‘quality of weight loss’ rather than its extent. Consequently, the industry is developing next-generation therapeutic combinations aimed at preserving muscle mass, potentially creating a $5–10bn niche for complementary muscle-preserving therapies. Overall, this is more a sign of market maturation than a structural weakening of demand.

The opportunities are vast and innovation is advancing, but the barriers to entry are high.

Novo Nordisk and Eli Lilly benefit from their scale, production capacity, established relationships with payers and extensive experience. The current duopoly is expected to remain largely intact until new, differentiated products enter the market later this decade.

Ultimately, if competitors manage to demonstrate superior efficacy, better tolerability, more convenient dosing or more competitive pricing, market shares could shift. The market for obesity drugs remains structurally attractive, but it has entered a phase of heightened competition, where pricing, access and clinical differentiation will determine the long-term winners.

Adams Street Partners, 12 March 2026

Authors: 2026 Global Investor Survey

Adams Street Partners ‘Global Investor Survey 2026’ highlights a shift in investors’ behaviour in the private sector

· 90% of Limited Partners (LPs) believe that liquidity constraints will shape their strategy in 2026

· Europe has overtaken North America as the most attractive region for investors

· Concerns about tech disruption, investors expect managers to integrate AI into sourcing, due diligence and portfolio management

Liquidity is becoming central to strategy

Liquidity constraints are now the main challenge for private market investors. Nearly 90% of respondents believe that liquidity pressures will influence their strategy in 2026, and two-thirds anticipate a moderate or significant impact. Whilst distributions remain below historical norms, LPs are increasingly turning to secondary markets, particularly continuation vehicles, to manage their cash flows and rebalance their portfolios. Co-investments are also gaining popularity, offering direct access to quality assets at a lower overall cost. Against this backdrop of reduced liquidity, fundraising has slowed and fewer LPs are increasing their commitments to existing managers – just 53% compared to 67% previously – whilst appetite for new managers has fallen to its lowest level in five years.

In response, investors are focusing their capital on managers capable of generating repeatable alpha, with in-depth sector expertise and strong alignment of interests. Governance remains a key factor: 85% of LPs consider management team incentive structures to be a significant driver of outperformance in private markets.

Europe overtakes North America for the first time

One of the survey’s most striking findings is that Europe will overtake North America as the most attractive region for private market investments by 2026. Investors cite attractive valuations, government support and opportunities in the European mid-market as the main factors. Although North America remains at the heart of many portfolios, geopolitical tensions and concentration risks are prompting LPs to further diversify their geographical exposures. At the same time, geopolitical risk is becoming a major strategic consideration: nearly nine in ten LPs expect it to significantly influence private markets strategies, particularly due to tensions between the US and China.

AI is becoming an indispensable capability

Artificial intelligence is rapidly evolving from an investment theme into an operational requirement. Technological disruption is now cited by 28% of LPs as a major risk, up from 17% last year, illustrating the growing impact of AI on valuations, competition and business models. At the same time, technology and healthcare rank among the most attractive sectors for 2026, alongside co-investments, each cited by 39% of respondents. AI is no longer merely a differentiating factor, it has become a genuine driver of value creation. Investors expect managers not only to identify companies using AI, but also to integrate these technologies into their own processes, from sourcing through due diligence to the operational management of portfolios.”

Contacts

8 Kievyan Street, Yerevan, Armenia

+374 10 712 259

+374 43 004 182

unibankinvest@unibank.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.