Last week: low US Aug job report; OPEC+ October production hike; French political turmoil; Japan PM Ishiba resigned

WEEKLY TRENDS

WEEKLY TRENDS

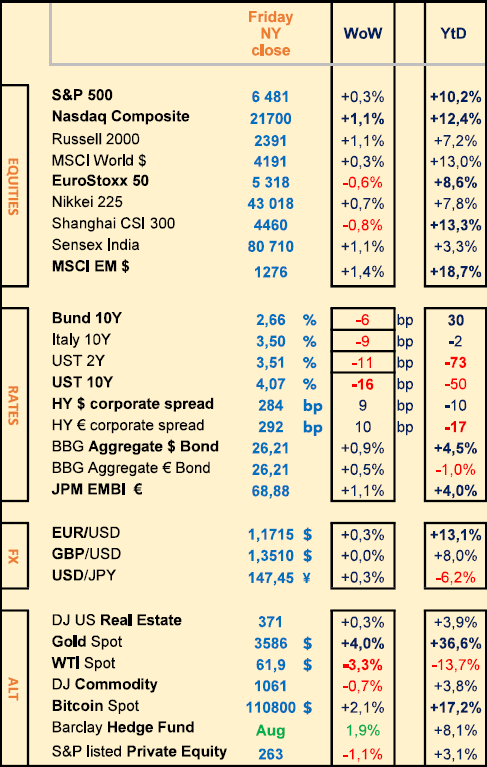

- The main markets element last week was the release of the US August job report (after so much doubts recently over the US statistics reliability) which turned out to be on a weaker note at +22k, validating in itself a September FED rate cut. Bond yields were lower across the board

- Strong individual equity performance from Alphabet (+11%) and Apple (+3%) boosted by a US Federal court decision mid-week (on Chrome navigator use) but an EU court decision on Friday ($3.45bn fine over ads) came in late to steal the show, Trump reacted almost immediately and threatened new trade actions against the EU

- In Japan PM Ishiba resigned on Sunday and the OPEC+ decided to hike its production starting October

- China showed strong August PMI last week, with a 15 month high at 53.0 vs 51.6 in July (the highest since May 2024)

- The ECB will meet this coming Thursday and the US shall release its Aug PPI and CPI respectively on Wednesday and Thursday. NB in France, on Sep 8 (PM confidence vote), followed by Sep 10 and Sep18 (planned unions strikes).

MARKETS

Equities

Earnings released stock weekly performances:

Broadcom (+9%), HP (+4%), Salesforce (-2%)

NB:

United Therapeutics (+31%), Ciena (+24%), Fresnillo (+18%)

Currys (+14%), Figma (-21%), CoreWeave (-13%), Temenos (-16%)

M&A:

Google (+11%), bought Wiz for $32bn

Analysts: SGS (BNP Exane ‘o/w’ target CHF 98), Siemens Energy (HSBC ‘buy’ target €110), Eiffage (JPM ‘o/w’ target €135), Nexans (GS ‘buy’ target €143), Holcim (GS ‘buy’ target CHF 75)

Rates

US curve (2-10 years) steepening slightly down at 55bps (-5). Bond yields lower across the board.

HY corporate spreads higher by 10bps (US at 285bps EU at 290bps)

Commodities

Oil price lower (-3%) higher US inventories, OPEC+ meeting potential production rise accord

Gold price higher (+4%) new ATH at $3560 an ounce (lower US yields)

NB: Silver YTD performance is at +41% vs Gold at +36%

US

Aug NFP lower at +22k vs +75k expected, prior at +79k

China

Aug PMI at a 15 month high (since May 2024) released at 53 vs 51.6 prior

Under the watch

France debt rating reviews (Fitch 12 Sep; Moody’s 24 Oct; S&P 28 Nov)

US budget and fiscal situation (Oct 14 US court decision over tariffs)

Nota Bene

DB, Siemens Energy, BBVA, Rheinmetall (join the EU50 on 22 Sep)

CALENDAR

Earnings releases: US Adobe (11 Sep)

Macro releases: US August PPI (10 Sep), CPI (11 Sep)

Upcoming central bank meetings: ECB (11 Sep), FED/FOMC (17 Sep), BOE/MPC (18 Sep)

WHAT ANALYSTS SAY

CME Group, 2 September 2025

Tariff tumult leads to major market moves

While tariffs have become a persistent feature in economic headlines, their real-world implementation is highly nuanced, creating significant ripple effects across commodity sectors. A new wave of tariffs impacted approximately 90 countries starting August 7, with some rates climbing as high as 50%, intensifying market uncertainty.

China, a cornerstone market for American agricultural products, remains central to the ongoing trade uncertainty. More than halfway through August, the U.S. has yet to record a single soybean sale to China for the current or upcoming marketing year– a stark contrast to the 2023-2024 marketing year when 22% of the U.S. soybean crop was exported to China (China accounted for 54% of U.S. soybean exports). This absence of export sales coupled with trade uncertainty coincided with a highly active day in Agricultural options trading on August 12, which saw the second largest volume of the year at 891,391 contracts and open interest reaching 4,799,682. This surge in trading followed a surprising WASDE report released the same day, which forecast an additional 752 million bushels of corn for 2025 U.S. production.

Global trade uncertainty and tariffs are significantly impacting the metals sector, particularly across gold and copper. The copper market had anticipated broad tariffs in late July; however, the unexpected exemption of raw forms like cathodes and ores triggered the largest single-day selloff in copper's history on July 31, as traders unwound their positions. The gold market also faced a bout of speculative whiplash: the initial announcement of a 39% tariff on Swiss imports was later clarified by the White House, calming initial market volatility.

Uncertainty is also fuelling a surge in activity within the energy markets. The average daily volume (ADV) for Crude Oil Weekly options jumped 41% in August compared to July 2025, reflecting a growing demand for short-term hedging instruments. With OPEC meetings scheduled monthly through the end of the year, the potential for continued volatility remains high.

Geopolitical strategy is now a primary driver of volatility across all three major commodity sectors. The resulting price fluctuations are critical, directly influencing production costs, consumer prices and broader inflation expectations.

World Gold Council, 4 September 2025

Gold closing in on new highs

A strong rally into month-end saw gold reach US$3,429/oz (+4%), and as of the end of August, gold was up 31% for the year. Gold gained in all major currencies, despite a much weaker US dollar. And the positive momentum has carried on in early September. Our Gold Return Attribution Model (GRAM) suggests major contributors to August price performance were a drop in the US dollar early in the month, continued geopolitical tensions, and strong global gold ETF flows. More recently, a higher chance of a September rate cut has also played a role. Gold ETF flows provided plenty of support, especially late in the month, posting US$5.5bn (53t) of inflows, dominated by North America (US$4.1bn) and Europe (US$1.9bn), while Asia and other regions saw outflows. COMEX managed money net longs saw more restrained inflows of US$2bn (+16t).

Stubborn stagflation

US real rates may become more influential for gold in the near term as US investors grab the baton from emerging markets, and that influence could increase if rates were to fall. So far rates have been sticky, but that is more reflective of a growing unease about stagflation. Our quantitative analysis of various US investor types suggests that stagflation is of greatest concern to ETF investors, followed by retail bar and coin buyers. Fast money futures investors are more concerned with rate trajectory.

Passing the baton

The relationship between the price of gold and its core drivers shifts over time, sometimes reflecting who is most active in the market. For example, US real interest rates (opportunity cost) were tightly linked to movements in gold between 2007 and 2022. Last month we suggested that one reason for gold’s decoupling from rates post 2022 was the preponderance of emerging market demand from central banks and other investors, rather than a breakdown in US investor relationship with rates. Now that central banks and Asian investors have stepped back a bit, as indicated by our Gold Demand Trends data, local premia and intraday session returns, a tighter gold-rates relationship could re-establish itself and Western investors (particularly the US) could become more dominant in driving short-term returns. Should rates across the curve start to drop, a ramp up in gold buying could be triggered in the US. But we’re not seeing that quite yet. In fact, the curve is steepening as the short end drops on Fed cut hopes, but the long end remains high on risk premia and future inflation concerns.

What’s your flavour?

Our analysis suggests that ETF investors are the most sensitive to expectations of stagflation – statistically, significantly so. Bar and coin investors are next, although the average response is not statistically significant. On COMEX, non-reportable investors – who are said to be more representative of retail flows – have also responded positively, on average. But ‘fast money’ investors, many of whom are Commodity Trading Advisors (CTAs) appear less enamoured by stagflationary fears. This is possibly because they are more focused on interest rates – as we surmised last month. And, for CTAs, technical factors arguably play a role too. In other words, stagflation threatens higher rates, not lower as we are seeing at the moment, and fast money investors are perhaps less willing to participate until those start to soften.

In summary

Gold’s sensitivity to US real interest rates may increase as Western investors, particularly in the US, take a more active role amid softer demand from emerging markets. While rates in the long end remain sticky, this reflects growing stagflation concerns – an environment that has historically supported gold. Among US investor segments, ETF holders show the strongest response to stagflation risks and have picked up their pace of investment over the last few weeks, not just in the US but in Europe too – where real rates are still rising – suggesting risk drivers are offsetting rates-based drivers. Futures traders appear more focused on rate dynamics. As the yield curve steepens (driven by lower front-end rates) and inflation fears persist, the interplay between macroeconomic signals and investor behaviour will be key in shaping gold’s next move.

JP Morgan, 2 September 2025

Author : Gérard Reber, US equity Analyst

We haven't seen such enthusiasm for a new technology in over 30 years. The arrival of ChatGPT just under 3 years ago democratised what is now known as ‘generative artificial intelligence’ (GEN AI). The current frenzy therefore raises a key question: are we witnessing the formation of a new technology bubble?

Certain parallels between the technology bubble of the late 1990s and the current AI boom are hard to ignore. Both periods are characterised by a whirlwind of innovation and profound long-term impacts. In the late 1990s, the internet represented a new frontier: it sparked a wave of technological advances and massive investment that allowed the digital economy to flourish. Today, AI is taking centre stage, driven by breakthroughs in machine learning and natural language processing that are capturing the imagination and attracting capital. In both cases, media hype and investor appetite led to the overvaluation of certain companies, but they also highlighted the transformative potential of these technological revolutions. While there are similarities, it is important to note that today's context and characteristics are unique. The AI sector, for example, benefits from more mature technologies, companies with strong balance sheets, and a much broader range of applications than the internet in its early days.

Unlike in the dot-com era, today's AI leaders are already generating substantial cash flows while reinvesting in the next major technological shift. As is often the case, these platform disruptions pave the way for even more profound innovations that can transform the economy for a decade or more. We therefore remain extremely confident in AI's potential to permanently reshape all sectors of the economy.

10 years ago, cloud computing was an emerging sector in which companies were investing huge sums in infrastructure and development. The promise was clear: to revolutionise the way organisations operate by offering scalable IT resources that were accessible on demand. But at the time, profitability remained uncertain and business models were yet to be defined, raising questions about the relevance of such expenditure. Today, AI is experiencing a similar dynamic. Companies are betting big on its potential to transform entire industries. Whether it's machine learning or natural language processing, progress is rapid and impressive, but the financial stakes remain high and the industry still faces several challenges. In both cases, the gamble is based on a conviction: long-term benefits and the transformative power of technology. Just as cloud computing has become a cornerstone of modern operations, the hope is that AI will deliver on its promises despite the current uncertainties and financial risks.

Generative artificial intelligence (Gen AI) undoubtedly has the potential to be as profitable as cloud computing – if not more so. This potential is based on two major drivers: the diversity of its use cases in virtually all sectors, and its ability to generate cost savings. Gen AI is already being applied in many areas, from healthcare and finance to entertainment and education. Beyond savings, Gen AI drives innovation. It fosters the emergence of new products and services, while enhancing existing technologies such as cloud computing, which it enriches with advanced analytics, personalisation and automation capabilities. This combination offers businesses more comprehensive solutions with higher added value. The second quarter results bear this out: the strong growth in cloud revenues is due to AI, which is becoming a significant driver of this business. This growing demand for AI as a sign of an imminent turning point in the adoption of Gen AI-related workloads by businesses.

Equities

Earnings released stock weekly performances:

Broadcom (+9%), HP (+4%), Salesforce (-2%)

NB:

United Therapeutics (+31%), Ciena (+24%), Fresnillo (+18%)

Currys (+14%), Figma (-21%), CoreWeave (-13%), Temenos (-16%)

M&A:

Google (+11%), bought Wiz for $32bn

Analysts: SGS (BNP Exane ‘o/w’ target CHF 98), Siemens Energy (HSBC ‘buy’ target €110), Eiffage (JPM ‘o/w’ target €135), Nexans (GS ‘buy’ target €143), Holcim (GS ‘buy’ target CHF 75)

Rates

US curve (2-10 years) steepening slightly down at 55bps (-5). Bond yields lower across the board.

HY corporate spreads higher by 10bps (US at 285bps EU at 290bps)

Commodities

Oil price lower (-3%) higher US inventories, OPEC+ meeting potential production rise accord

Gold price higher (+4%) new ATH at $3560 an ounce (lower US yields)

NB: Silver YTD performance is at +41% vs Gold at +36%

US

Aug NFP lower at +22k vs +75k expected, prior at +79k

China

Aug PMI at a 15 month high (since May 2024) released at 53 vs 51.6 prior

Under the watch

France debt rating reviews (Fitch 12 Sep; Moody’s 24 Oct; S&P 28 Nov)

US budget and fiscal situation (Oct 14 US court decision over tariffs)

Nota Bene

DB, Siemens Energy, BBVA, Rheinmetall (join the EU50 on 22 Sep)

CALENDAR

Earnings releases: US Adobe (11 Sep)

Macro releases: US August PPI (10 Sep), CPI (11 Sep)

Upcoming central bank meetings: ECB (11 Sep), FED/FOMC (17 Sep), BOE/MPC (18 Sep)

WHAT ANALYSTS SAY

- CME Group: Commodities update

- World Gold Council: Stubborn stagflation

- JP Morgan: Should we fear a generative bubble?

CME Group, 2 September 2025

Tariff tumult leads to major market moves

While tariffs have become a persistent feature in economic headlines, their real-world implementation is highly nuanced, creating significant ripple effects across commodity sectors. A new wave of tariffs impacted approximately 90 countries starting August 7, with some rates climbing as high as 50%, intensifying market uncertainty.

China, a cornerstone market for American agricultural products, remains central to the ongoing trade uncertainty. More than halfway through August, the U.S. has yet to record a single soybean sale to China for the current or upcoming marketing year– a stark contrast to the 2023-2024 marketing year when 22% of the U.S. soybean crop was exported to China (China accounted for 54% of U.S. soybean exports). This absence of export sales coupled with trade uncertainty coincided with a highly active day in Agricultural options trading on August 12, which saw the second largest volume of the year at 891,391 contracts and open interest reaching 4,799,682. This surge in trading followed a surprising WASDE report released the same day, which forecast an additional 752 million bushels of corn for 2025 U.S. production.

Global trade uncertainty and tariffs are significantly impacting the metals sector, particularly across gold and copper. The copper market had anticipated broad tariffs in late July; however, the unexpected exemption of raw forms like cathodes and ores triggered the largest single-day selloff in copper's history on July 31, as traders unwound their positions. The gold market also faced a bout of speculative whiplash: the initial announcement of a 39% tariff on Swiss imports was later clarified by the White House, calming initial market volatility.

Uncertainty is also fuelling a surge in activity within the energy markets. The average daily volume (ADV) for Crude Oil Weekly options jumped 41% in August compared to July 2025, reflecting a growing demand for short-term hedging instruments. With OPEC meetings scheduled monthly through the end of the year, the potential for continued volatility remains high.

Geopolitical strategy is now a primary driver of volatility across all three major commodity sectors. The resulting price fluctuations are critical, directly influencing production costs, consumer prices and broader inflation expectations.

World Gold Council, 4 September 2025

Gold closing in on new highs

A strong rally into month-end saw gold reach US$3,429/oz (+4%), and as of the end of August, gold was up 31% for the year. Gold gained in all major currencies, despite a much weaker US dollar. And the positive momentum has carried on in early September. Our Gold Return Attribution Model (GRAM) suggests major contributors to August price performance were a drop in the US dollar early in the month, continued geopolitical tensions, and strong global gold ETF flows. More recently, a higher chance of a September rate cut has also played a role. Gold ETF flows provided plenty of support, especially late in the month, posting US$5.5bn (53t) of inflows, dominated by North America (US$4.1bn) and Europe (US$1.9bn), while Asia and other regions saw outflows. COMEX managed money net longs saw more restrained inflows of US$2bn (+16t).

Stubborn stagflation

US real rates may become more influential for gold in the near term as US investors grab the baton from emerging markets, and that influence could increase if rates were to fall. So far rates have been sticky, but that is more reflective of a growing unease about stagflation. Our quantitative analysis of various US investor types suggests that stagflation is of greatest concern to ETF investors, followed by retail bar and coin buyers. Fast money futures investors are more concerned with rate trajectory.

Passing the baton

The relationship between the price of gold and its core drivers shifts over time, sometimes reflecting who is most active in the market. For example, US real interest rates (opportunity cost) were tightly linked to movements in gold between 2007 and 2022. Last month we suggested that one reason for gold’s decoupling from rates post 2022 was the preponderance of emerging market demand from central banks and other investors, rather than a breakdown in US investor relationship with rates. Now that central banks and Asian investors have stepped back a bit, as indicated by our Gold Demand Trends data, local premia and intraday session returns, a tighter gold-rates relationship could re-establish itself and Western investors (particularly the US) could become more dominant in driving short-term returns. Should rates across the curve start to drop, a ramp up in gold buying could be triggered in the US. But we’re not seeing that quite yet. In fact, the curve is steepening as the short end drops on Fed cut hopes, but the long end remains high on risk premia and future inflation concerns.

What’s your flavour?

Our analysis suggests that ETF investors are the most sensitive to expectations of stagflation – statistically, significantly so. Bar and coin investors are next, although the average response is not statistically significant. On COMEX, non-reportable investors – who are said to be more representative of retail flows – have also responded positively, on average. But ‘fast money’ investors, many of whom are Commodity Trading Advisors (CTAs) appear less enamoured by stagflationary fears. This is possibly because they are more focused on interest rates – as we surmised last month. And, for CTAs, technical factors arguably play a role too. In other words, stagflation threatens higher rates, not lower as we are seeing at the moment, and fast money investors are perhaps less willing to participate until those start to soften.

In summary

Gold’s sensitivity to US real interest rates may increase as Western investors, particularly in the US, take a more active role amid softer demand from emerging markets. While rates in the long end remain sticky, this reflects growing stagflation concerns – an environment that has historically supported gold. Among US investor segments, ETF holders show the strongest response to stagflation risks and have picked up their pace of investment over the last few weeks, not just in the US but in Europe too – where real rates are still rising – suggesting risk drivers are offsetting rates-based drivers. Futures traders appear more focused on rate dynamics. As the yield curve steepens (driven by lower front-end rates) and inflation fears persist, the interplay between macroeconomic signals and investor behaviour will be key in shaping gold’s next move.

JP Morgan, 2 September 2025

Author : Gérard Reber, US equity Analyst

We haven't seen such enthusiasm for a new technology in over 30 years. The arrival of ChatGPT just under 3 years ago democratised what is now known as ‘generative artificial intelligence’ (GEN AI). The current frenzy therefore raises a key question: are we witnessing the formation of a new technology bubble?

Certain parallels between the technology bubble of the late 1990s and the current AI boom are hard to ignore. Both periods are characterised by a whirlwind of innovation and profound long-term impacts. In the late 1990s, the internet represented a new frontier: it sparked a wave of technological advances and massive investment that allowed the digital economy to flourish. Today, AI is taking centre stage, driven by breakthroughs in machine learning and natural language processing that are capturing the imagination and attracting capital. In both cases, media hype and investor appetite led to the overvaluation of certain companies, but they also highlighted the transformative potential of these technological revolutions. While there are similarities, it is important to note that today's context and characteristics are unique. The AI sector, for example, benefits from more mature technologies, companies with strong balance sheets, and a much broader range of applications than the internet in its early days.

Unlike in the dot-com era, today's AI leaders are already generating substantial cash flows while reinvesting in the next major technological shift. As is often the case, these platform disruptions pave the way for even more profound innovations that can transform the economy for a decade or more. We therefore remain extremely confident in AI's potential to permanently reshape all sectors of the economy.

10 years ago, cloud computing was an emerging sector in which companies were investing huge sums in infrastructure and development. The promise was clear: to revolutionise the way organisations operate by offering scalable IT resources that were accessible on demand. But at the time, profitability remained uncertain and business models were yet to be defined, raising questions about the relevance of such expenditure. Today, AI is experiencing a similar dynamic. Companies are betting big on its potential to transform entire industries. Whether it's machine learning or natural language processing, progress is rapid and impressive, but the financial stakes remain high and the industry still faces several challenges. In both cases, the gamble is based on a conviction: long-term benefits and the transformative power of technology. Just as cloud computing has become a cornerstone of modern operations, the hope is that AI will deliver on its promises despite the current uncertainties and financial risks.

Generative artificial intelligence (Gen AI) undoubtedly has the potential to be as profitable as cloud computing – if not more so. This potential is based on two major drivers: the diversity of its use cases in virtually all sectors, and its ability to generate cost savings. Gen AI is already being applied in many areas, from healthcare and finance to entertainment and education. Beyond savings, Gen AI drives innovation. It fosters the emergence of new products and services, while enhancing existing technologies such as cloud computing, which it enriches with advanced analytics, personalisation and automation capabilities. This combination offers businesses more comprehensive solutions with higher added value. The second quarter results bear this out: the strong growth in cloud revenues is due to AI, which is becoming a significant driver of this business. This growing demand for AI as a sign of an imminent turning point in the adoption of Gen AI-related workloads by businesses.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+374 43 00-43-82

Broker

broker@unibankinvest.am

research@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.