Last week: USD weaker; Stocks lower; Precious Metals and Oil higher; speculation BOJ/FED are to buy JPY; TACO

WEEKLY TRENDS

WEEKLY TRENDS

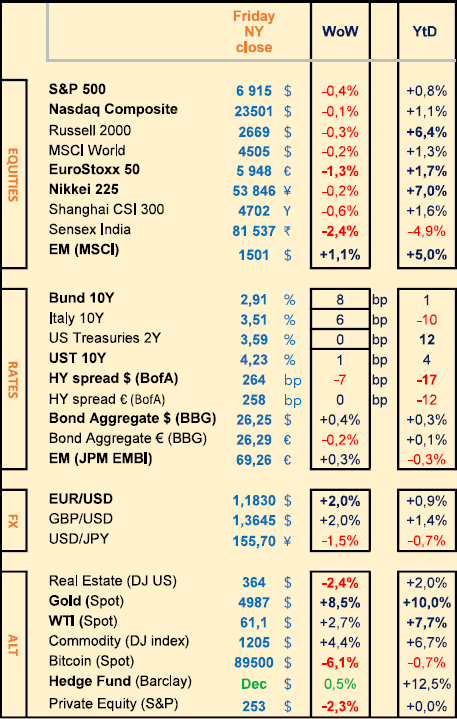

- Wild markets last week, after Trump’s renewed threats of tariffs towards the EU but finally dropped those mid way on Thursday (typical TACO trade: Trump Always Chickens Out, hence fairly stable US Treasuries in the end) having said that the USD finished the week a lot weaker (-2%) and Precious Metals hit new ATH (Gold +10% YTD, Silver +40%)

- Oil is higher on Trump’s intention to send the US navy fleet towards the Persian Gulf

- Speculation of a combined BOJ/FED intervention brought USDJPY to 155s on Friday after Japan MOF Katayama said she was watching the FX rate with a sense of urgency (BOJ left its base rate unchanged last week, JGB 30yr yield hit 3.6%). Else, we shall have the FOMC/FED decision next week (28 Jan) note that the markets Futures do not see any cut before June now

- Q4 corporate earnings will continue to be released with some of the Mag7 on Wednesday and Thursday (Microsoft, Meta, Apple, Tesla) together with US Oil corp. In Europe, we will have LVMH’s on Tuesday

- Note that we already had wild swings in individual equities including Intel, Abbott, Ubisoft, SanDisk, Carl Zeiss...

MARKETS

Equities

Q4 earnings weekly performances:

Intel (-8%), Abbott (-12%), Netflix (-2%), P&G (+4%), Schlumberger(+5%)

NB

SanDisk (+15%), Hecla Mining (+20%), Ubisoft (-38%), Carl Zeiss (-28%)

M&A: Beazley (+40%) the UK insurer refused a 2nd offer from Zurich Ins.

Bank analysts: Engie (MS ‘o/w’ target €26), Wise (BofA ‘buy’ target £11.25), ASM Int (GS ‘buy’ target €795), BE semi (GS ‘buy’ target €200)

Rates

US curve steepening (2-10 years) stable at 64bps

HY corp. spreads lower: US at +264bps (-5); EU at +258bps (stable)

Commodities

Oil price higher (+2.5%) helped with a weaker USD also due to renewed Iran concerns and cold weather in the US

Gold price higher (+8.5%) helped with a weaker USD - Silver hit $102 Spot (Shanghai at +35% premium over London and Tokyo at +42%)

UK

Jan PMI (Manufacturing 51.6 vs 50.6 exp and 50.6 prior); (Services 54.3 vs 51.7 exp and 51.4 prior)

US

Q3 GDP (revised at +4.4%) while Q4 is expected at +5.4%

Oct PCE (Core released at +2.7%, slightly lower by -0.1%)

Crypto

BTC (-6%), ETH (-11%), SOL (-8%), XRP (-5%)

Under the watch

BlackRock’s TCP Capital NAV dropped by 19% in Q4 2025

Nota Bene

Foreigners own 35% of USTs (Asia 15%; EU 14%), 65% held by US (Pension funds, Monetary Authority, Mutual Funds, Individuals)

CALENDAR

Earnings releases:

US Microsoft, Meta, Tesla (28 Jan), Apple (29), Exxon, Chevron (30)

EU LVMH (27), ASML Holding (28)

Central Bank rate decisions:

FED/FOMC (28 Jan), BOC (28 Jan)

WHAT ANALYSTS SAY

Julius Baer, 21 January 2026

Author: Christian Gattiker, Head of Research

How do the best-informed players perceive global vulnerabilities, often before the markets do?

Every January, all eyes turn to Davos: the World Economic Forum (WEF) brings together political decision-makers and gives rise to speculation about the direction of future markets and policies. Entertaining, certainly. But for investors, one document is far more revealing: the WEF's Global Risks Report. It reflects how the best-connected players perceive global vulnerabilities, often before the markets do.

I discovered the WEF's Global Risks Report in the run-up to the 2008 global financial crisis. What struck me was not so much its visionary nature, but its consistency: well-informed decision-makers had been pointing to systemic fragility for years before the global collapse. Since then, the centre of gravity has shifted significantly from the “pure” economy to geopolitics, technology, society and the environment. The only notable exception is 2020 : pandemics were not among the main concerns before, reminding us uncomfortably that we cannot predict everything, but only prepare for what appears on our radars.

So what does the 2026 edition teach us?

In a word: competition. The report describes 2026 as an ‘era of competition’ characterised by weakening cooperation mechanisms and prevailing uncertainty. Unsurprisingly, geo-economic confrontations rank first among short-term risks (trade, sanctions, investment controls and strategic use of supply chains), followed by armed conflicts between states. The overall tone of the survey is sombre: 50% of executives expect ‘turbulent’ or ‘stormy’ prospects for the next two years (rising to 57% for the next decade).

For investors, three major consequences emerge.

First, geopolitics has become a portfolio variable, rather than a secondary factor: hedging is not optional when conflicts and geo-economic tools top the list of risks.

Secondly, information integrity and cyber risks remain very high – disinformation and cyber insecurity are among the most serious short-term risks – so resilience is crucial at the corporate level and not just at the macroeconomic level.

Thirdly, long-term risks remain dominant: extreme weather events and environmental risks in the broad sense dominate the ten-year horizon, while the negative consequences of artificial intelligence are perceived as increasingly serious over time.

In practice, all of this argues in favour of real assets as stabilisers, rigorous stock selection and a lower risk premium on robust business models and strong governance. The report does not predict the future, but it does take stock of the current situation.

Vanguard, 19 January 2026

Authors: Jonathan Decurtins, Wholesale sector’s Head

AI-related stocks are appealing, but a well-diversified 60/40 portfolio, enriched with defensive components, remains the most solid strategy.

We believe it is time to return to the fundamentals of diversification and discipline. The classic 60/40 portfolio – 60% equities and 40% bonds – provides a solid foundation, particularly in times of media hype and uncertainty. By choosing a broadly diversified mix of equities, including international markets, and focusing on quality bonds, you can build a portfolio that can withstand a variety of scenarios.

There are many ETFs with significant exposure to technology that can be used to build the equity portion of the portfolio, including those that track the S&P 500 or Nasdaq. The message to retail investors is clear: resist the temptation to bet exclusively on AI. AI will undoubtedly have a major impact on the economy and the stock markets, but that does not mean that today's winners will necessarily be tomorrow's winners. The current environment calls for diversification and the inclusion of certain defensive components.

The reason is simple: a very limited number of stocks are actually driving the market rally. Research by Hendrik Bessembinder (2023) shows that between 1990 and 2020, only 159 stocks, out of a global universe of 64,000, were responsible for half of stock market returns. Identifying these winners would obviously be ideal, but highly concentrated portfolios actually increase the risk of loss.

Especially in the long term, a broadly diversified ETF portfolio offers the highest probability of return, as investing in a large number of companies increases the chances of including this select group of winners. By focusing on balance and discipline, you can build a portfolio that benefits from technological progress while remaining resilient to market volatility.

It is also important to select ‘value’ options, i.e. ETFs that invest in companies with lower valuations. It is also possible to consider portfolios composed of companies paying higher dividends, simply via an ETF. Finally, it is important to maintain sufficient geographical diversification. In addition to ETFs invested in US equities, there are solutions based on indices composed of European, Pacific or emerging market securities.

There are also attractive opportunities in the bond portion of the portfolio. After years of disappointing performance, bonds are once again offering real returns above expected inflation. They also provide the necessary diversification if AI-driven growth disappoints. We currently believe that the best prospects are in the US bond market, which remains the deepest and most liquid in the world. US bonds are expected to offer yields close to current levels, regardless of central bank policy.

And for those who prefer simplicity and do not wish to make tactical choices, there are multi-asset ETFs. These allow investors to invest simultaneously in equities and bonds, according to the desired ratio, with automatic rebalancing. The 60/40 portfolio has never been so simple and affordable. In summary, the 60/40 portfolio with defensive touches remains an extremely solid foundation for the long term, even in the age of AI.

Equities

Q4 earnings weekly performances:

Intel (-8%), Abbott (-12%), Netflix (-2%), P&G (+4%), Schlumberger(+5%)

NB

SanDisk (+15%), Hecla Mining (+20%), Ubisoft (-38%), Carl Zeiss (-28%)

M&A: Beazley (+40%) the UK insurer refused a 2nd offer from Zurich Ins.

Bank analysts: Engie (MS ‘o/w’ target €26), Wise (BofA ‘buy’ target £11.25), ASM Int (GS ‘buy’ target €795), BE semi (GS ‘buy’ target €200)

Rates

US curve steepening (2-10 years) stable at 64bps

HY corp. spreads lower: US at +264bps (-5); EU at +258bps (stable)

Commodities

Oil price higher (+2.5%) helped with a weaker USD also due to renewed Iran concerns and cold weather in the US

Gold price higher (+8.5%) helped with a weaker USD - Silver hit $102 Spot (Shanghai at +35% premium over London and Tokyo at +42%)

UK

Jan PMI (Manufacturing 51.6 vs 50.6 exp and 50.6 prior); (Services 54.3 vs 51.7 exp and 51.4 prior)

US

Q3 GDP (revised at +4.4%) while Q4 is expected at +5.4%

Oct PCE (Core released at +2.7%, slightly lower by -0.1%)

Crypto

BTC (-6%), ETH (-11%), SOL (-8%), XRP (-5%)

Under the watch

BlackRock’s TCP Capital NAV dropped by 19% in Q4 2025

Nota Bene

Foreigners own 35% of USTs (Asia 15%; EU 14%), 65% held by US (Pension funds, Monetary Authority, Mutual Funds, Individuals)

CALENDAR

Earnings releases:

US Microsoft, Meta, Tesla (28 Jan), Apple (29), Exxon, Chevron (30)

EU LVMH (27), ASML Holding (28)

Central Bank rate decisions:

FED/FOMC (28 Jan), BOC (28 Jan)

WHAT ANALYSTS SAY

- Julius Baer: Davos, "Game of Zones"

- Vanguard: AI, keeping a cool head in 2026

Julius Baer, 21 January 2026

Author: Christian Gattiker, Head of Research

How do the best-informed players perceive global vulnerabilities, often before the markets do?

Every January, all eyes turn to Davos: the World Economic Forum (WEF) brings together political decision-makers and gives rise to speculation about the direction of future markets and policies. Entertaining, certainly. But for investors, one document is far more revealing: the WEF's Global Risks Report. It reflects how the best-connected players perceive global vulnerabilities, often before the markets do.

I discovered the WEF's Global Risks Report in the run-up to the 2008 global financial crisis. What struck me was not so much its visionary nature, but its consistency: well-informed decision-makers had been pointing to systemic fragility for years before the global collapse. Since then, the centre of gravity has shifted significantly from the “pure” economy to geopolitics, technology, society and the environment. The only notable exception is 2020 : pandemics were not among the main concerns before, reminding us uncomfortably that we cannot predict everything, but only prepare for what appears on our radars.

So what does the 2026 edition teach us?

In a word: competition. The report describes 2026 as an ‘era of competition’ characterised by weakening cooperation mechanisms and prevailing uncertainty. Unsurprisingly, geo-economic confrontations rank first among short-term risks (trade, sanctions, investment controls and strategic use of supply chains), followed by armed conflicts between states. The overall tone of the survey is sombre: 50% of executives expect ‘turbulent’ or ‘stormy’ prospects for the next two years (rising to 57% for the next decade).

For investors, three major consequences emerge.

First, geopolitics has become a portfolio variable, rather than a secondary factor: hedging is not optional when conflicts and geo-economic tools top the list of risks.

Secondly, information integrity and cyber risks remain very high – disinformation and cyber insecurity are among the most serious short-term risks – so resilience is crucial at the corporate level and not just at the macroeconomic level.

Thirdly, long-term risks remain dominant: extreme weather events and environmental risks in the broad sense dominate the ten-year horizon, while the negative consequences of artificial intelligence are perceived as increasingly serious over time.

In practice, all of this argues in favour of real assets as stabilisers, rigorous stock selection and a lower risk premium on robust business models and strong governance. The report does not predict the future, but it does take stock of the current situation.

Vanguard, 19 January 2026

Authors: Jonathan Decurtins, Wholesale sector’s Head

AI-related stocks are appealing, but a well-diversified 60/40 portfolio, enriched with defensive components, remains the most solid strategy.

We believe it is time to return to the fundamentals of diversification and discipline. The classic 60/40 portfolio – 60% equities and 40% bonds – provides a solid foundation, particularly in times of media hype and uncertainty. By choosing a broadly diversified mix of equities, including international markets, and focusing on quality bonds, you can build a portfolio that can withstand a variety of scenarios.

There are many ETFs with significant exposure to technology that can be used to build the equity portion of the portfolio, including those that track the S&P 500 or Nasdaq. The message to retail investors is clear: resist the temptation to bet exclusively on AI. AI will undoubtedly have a major impact on the economy and the stock markets, but that does not mean that today's winners will necessarily be tomorrow's winners. The current environment calls for diversification and the inclusion of certain defensive components.

The reason is simple: a very limited number of stocks are actually driving the market rally. Research by Hendrik Bessembinder (2023) shows that between 1990 and 2020, only 159 stocks, out of a global universe of 64,000, were responsible for half of stock market returns. Identifying these winners would obviously be ideal, but highly concentrated portfolios actually increase the risk of loss.

Especially in the long term, a broadly diversified ETF portfolio offers the highest probability of return, as investing in a large number of companies increases the chances of including this select group of winners. By focusing on balance and discipline, you can build a portfolio that benefits from technological progress while remaining resilient to market volatility.

It is also important to select ‘value’ options, i.e. ETFs that invest in companies with lower valuations. It is also possible to consider portfolios composed of companies paying higher dividends, simply via an ETF. Finally, it is important to maintain sufficient geographical diversification. In addition to ETFs invested in US equities, there are solutions based on indices composed of European, Pacific or emerging market securities.

There are also attractive opportunities in the bond portion of the portfolio. After years of disappointing performance, bonds are once again offering real returns above expected inflation. They also provide the necessary diversification if AI-driven growth disappoints. We currently believe that the best prospects are in the US bond market, which remains the deepest and most liquid in the world. US bonds are expected to offer yields close to current levels, regardless of central bank policy.

And for those who prefer simplicity and do not wish to make tactical choices, there are multi-asset ETFs. These allow investors to invest simultaneously in equities and bonds, according to the desired ratio, with automatic rebalancing. The 60/40 portfolio has never been so simple and affordable. In summary, the 60/40 portfolio with defensive touches remains an extremely solid foundation for the long term, even in the age of AI.

Contacts

8 Kievyan Street, Yerevan, Armenia

+374 10 712 259

+374 43 004 182

unibankinvest@unibank.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.