Last week: UBS report credit scare; rotation (+EM / Japan equities); lower Bond yields; higher Gold; PE and BTC lower

WEEKLY TRENDS

WEEKLY TRENDS

- Everyone is talking about the UBS report on private credit risks, together with the AI impact onto the software industry. The previous has sent shivers in the PE and private credit markets last week, the latter has continued to impact Tech stocks altogether

- Despite amazing earnings and a strong outlook, Nvidia did not manage to close the week positively (-7%)

- Sovereign bonds benefitted from the overall private credit scare, despite a higher than expected US Jan PPI reading

- The stocks and equity sectors rotation continues with Hyperscalers (MAG7 like Microsoft and non MAG7 like Oracle, IBM and Palantir being hurt the most YTD). February has always been a volatile month for equities and 2026 is no different

- China reopened last Tuesday after a long week of new year celebrations, with Gold largely benefitting from it. Lower UST yields also impacted positively Gold. OPEC+ members meet this Sunday 1st of March and could well decide to increase their production starting April

- This coming week, we shall have new Q4 earnings releases from Broadcom, Costco, Thales, ASM Int., Bayer, among others and the BSL will report US Feb NFP on Friday.

MARKETS

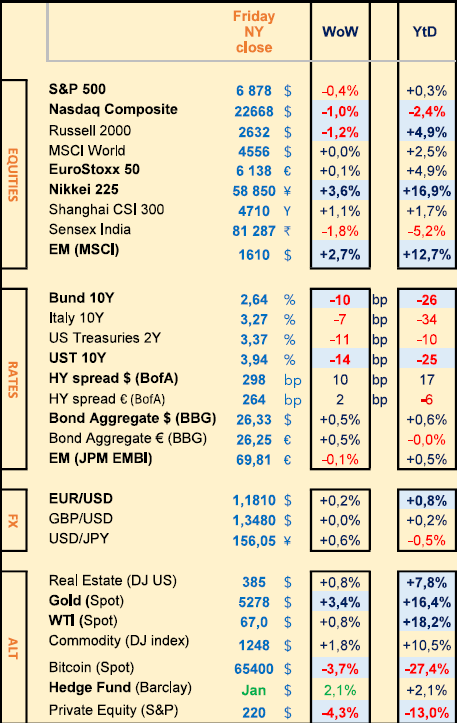

Equities

Q4 earnings weekly performances:

Salesforce (+7%), HSBC (+8%), Schneider Elec (+7%), Swiss Re (+5%), Nvidia (-7%), Holcim (-4%)

NB: Engie (+10%), Euronext (+10%), Dassault System (+6%)

Diageo (-10%), Novo Nordisk (-21%), Pernod Ricard (-10%)

Bank analysts: Siemens Energy (GS ‘buy’ target €185), Anheuser Inbev (MS ‘o/w’ target €74), Arcelormittal (MS ‘o/w’ target 54€)

Rates

US curve steepening (2-10 years) lower at +57bps (-3bps)

HY corp. spreads higher: US at +298bps (+10); EU stable at +264bps

Commodities

Oil price higher (+1%) US military around Hormuz strait; OPEC+ meets Sunday 1st March (could well decide to increase its production in April)

Gold price higher (+3.5%) China reopened last Tuesday (strong demand)

US

Jan PPI at +3.6% and Core at +2.9%

Crypto

BTC (-3.5%) 6th consecutive negative week; XRP (-2%)

Under the watch

MAG7 (YTD performances) Microsoft -19%, Apple -3%, Amazon -9%, Google/Alphabet -1%, Meta -2%, Nvidia -5%, Tesla -10%

Other Techs YTD performances: Oracle -26%, IBM -20%, AMD -9%, Palantir -21%, ASML +35%

Nota Bene

PE stocks YTD (Apollo -40%, Blackstone -43%, Ares -43%, KKR -46%, Blue Owl -60%) PE dry spell is worse than 2008 (Bain report)

$150bn of loans in CLOs face AI risk (according to JPM)

Tech Fwd PE at par with Consumer Staples

CALENDAR

Earnings releases:

US CrowdStrike (3 March), Broadcom (4), Costco (5)

EU Bayer, Adidas (4 March), Lufthansa (6)

Macro data releases:

US Feb ISM Services (4 March), Feb NFP job report (6)

WHAT ANALYSTS SAY

UBS, 24 February 2026

Author: Matthew Mish, Strategist

Executive Summary: Quantifying a Tail Risk Scenario

Investors increasingly want to talk about AI disruption and our tail risk scenario: a rapid, severe AI disruption. This is not our baseline ; however, at the risk of Monday morning quarterbacking, over 80% of what is written below was published back in November. What is new: a clearer catalyst (rapid, severe AI disruption).

Here are the key points:

· in a tail scenario, assuming contagion impacts not modelled in our earlier note, we anticipate US HY, LL and PC defaults could rise to 3-6%, 8-10% and 14-15%, respectively. Across these three markets defaults and losses would approach $420bn and $300bn

· in an extreme case, regression analysis suggests US IG, HY and LL spreads could trade to 160-170, 575-675 and 800-900bps

· credit availability will tighten materially, particularly for firms dependent on leveraged finance markets - PC and LL issuance could decline 50-75% YoY.

· financials will be impacted through several channels. One is NFBI loans, currently $2.5tn including all undrawn commitments. In a tail scenario, we estimate $1.6-1.8tn in total drawn exposures, of which about 30-40% is to private equity/credit/BDCs or SPVs/CLOs/ABS and we would consider higher risk.

Private Credit’s Expansion Has Outpaced Economic Growth

Private credit has evolved into a structurally significant segment of the US corporate debt landscape, now rivaling some traditional bank and bond markets. Since 2015, loan markets have grown at a high-single to low-double-digit compound annual rate, with private credit and leveraged loans each representing 6% and 5% of GDP, respectively up from 1% and 5% in 2008. Investment-Grade credit has expanded to 25% of GDP, nearly doubling its 2008 share. This growth reflects a shift in origination from banks to private lenders, driven by regulation and a reach for yield amid low rates. However, the scale relative to GDP raises questions about systemic risk and the market’s capacity to absorb shocks.

Credit Fundamentals Are Deteriorating, Albeit Gradually

While default rates remain contained, stress indicators are rising. Private credit defaults are reportedly between 3% and 5%, and signs of strain such as interest paid-in-kind are nearing post-pandemic highs. Leverage ratios have crept higher, with debt-to-EBITDA reaching 7.5–8x in some sectors when excluding certain earnings adjustments. Interest coverage ratios have ticked higher, but remain under pressure from elevated rates, with middle-market deals hovering in the 1.7-1.8x range. These metrics suggest that while the market is not in crisis, it is increasingly kicking the can down the road and vulnerable to macroeconomic deterioration, sectoral disruptions or liquidity shocks.

Sector Concentration and Structural Weaknesses Amplify Tail Risks

The most acute risk is a sector-specific shock triggering cascading defaults. Historical précédents such as telecom in 2001 and energy in 2016 show how concentrated defaults can drive market-level default rates. One sector can account for 55-80% of market level defaults. Today’s private credit portfolios are heavily weighted toward services (25-30%), technology (20-25%), and healthcare (15-17%). Technology is especially vulnerable to disruption from AI adoption or rapid retrenchment. These risks are compounded by weakening covenants, aggressive earnings adjustments, and opaque valuations. First-lien recoveries in syndicated loans recently fell to the mid-50% range and as low as 30% for energy in 2016 indicating reduced downside protection.

Contagion Risk to Public Credit Markets Is Real and Underappreciated

Private credit stress is unlikely to remain contained. Borrowers increasingly tap both private and syndicated loan markets, with overlapping issuer and sector exposures and shared sponsors. Services and tech represent 15-20% of leveraged loan portfolios, mirroring private credit. On the lender side, the top 20 direct lenders not only dominate private credit AUM but also hold significant stakes in BDCs (45%), leveraged loans (20%), and high-yield bonds (25%). This interconnectedness means that a spike in private defaults could ripple across public markets, widening spreads and impairing liquidity.

Financial Institutions Are Deeply Exposed to Private Credit

Banks and insurers have quietly built substantial exposure to private credit and alternatives. US and European banks hold $1.3 trn in loans and $1.1 bn in undrawn commitments to non-bank financial institutions (NBFIs). GSIBs account for 60% of the total. The fastest-growing categories include loans to SPVs, CLOs and ABS, closed-end investment and mutual funds, and private equity/credit funds and BDCs. Life insurers, specifically those linked to PE sponsors, have increased allocations to private credit and structured products, often relying on internal ratings. This raises concerns about capital adequacy and loss absorption in a downturn, particularly if defaults spike and valuations collapse.

We Don’t Have the Full Mosaic—But Idiosyncratic Risk Provides Opportunity

The private credit market is not in crisis, but the ingredients are present for a severe credit cycle. The key trigger is a shock to one of the key sectors. Size, leverage, sector concentration, and opacity all raise potential systemic risk, but limited transparency and disclosure make a proper calibration of macro risk challenging. Investors must monitor leading indicators defaults, PIKs, covenant breaches, and valuation marks at market and sector levels while demanding better disclosure and underwriting discipline. Policymakers and regulators should assess the implications of bank and insurer exposures, especially as private credit increasingly becomes a core funding source for high-growth sectors. However, overall idiosyncratic risk exposures provide single-name opportunities. Our analysis across banks, insurers, and BDCs globally suggests a wide range of private and alternative exposures could be impacted if we enter a private credit downturn.

BlackRock Investment Institute, 25 February 2026

Authors: Jean Boivin, Global Head of Research

The key message is clear:

we are entering a golden age for fixed income, and the opportunity lies in carry.

For European investors, the reset in yields and improved fundamentals make the region one of the most attractive globally.

In terms of positioning, we highlight the following themes:

· While global growth remains uneven, Europe is showing resilience, supported by easing inflationary pressures and a gradual normalisation of monetary policy. High yield levels, improved credit quality and favourable technical factors are creating a favourable environment for bond investors.

· With nominal yields around 3% and real yields close to 2%, their highest level in over a decade, income is once again becoming a significant driver of performance, after years of zero or negative real rates.

· Strong investor demand is supporting the market: European credit saw record inflows in 2025, as both institutional and retail investors gradually reallocated their cash.

· Changing market dynamics suggest that credit spreads, rather than duration, are now the most relevant source of opportunity. Although spreads are tight, BlackRock anticipates a broadly range-bound environment, with episodes of volatility generating selective entry points rather than continued compression.

· Maintain conviction on carry strategies in the short end of the credit curve, supported by targeted fiscal measures and solid technical factors.

Improvement in eurozone corporate fundamentals, including in the high-yield segment, where credit quality is now higher than in previous cycles.

Equities

Q4 earnings weekly performances:

Salesforce (+7%), HSBC (+8%), Schneider Elec (+7%), Swiss Re (+5%), Nvidia (-7%), Holcim (-4%)

NB: Engie (+10%), Euronext (+10%), Dassault System (+6%)

Diageo (-10%), Novo Nordisk (-21%), Pernod Ricard (-10%)

Bank analysts: Siemens Energy (GS ‘buy’ target €185), Anheuser Inbev (MS ‘o/w’ target €74), Arcelormittal (MS ‘o/w’ target 54€)

Rates

US curve steepening (2-10 years) lower at +57bps (-3bps)

HY corp. spreads higher: US at +298bps (+10); EU stable at +264bps

Commodities

Oil price higher (+1%) US military around Hormuz strait; OPEC+ meets Sunday 1st March (could well decide to increase its production in April)

Gold price higher (+3.5%) China reopened last Tuesday (strong demand)

US

Jan PPI at +3.6% and Core at +2.9%

Crypto

BTC (-3.5%) 6th consecutive negative week; XRP (-2%)

Under the watch

MAG7 (YTD performances) Microsoft -19%, Apple -3%, Amazon -9%, Google/Alphabet -1%, Meta -2%, Nvidia -5%, Tesla -10%

Other Techs YTD performances: Oracle -26%, IBM -20%, AMD -9%, Palantir -21%, ASML +35%

Nota Bene

PE stocks YTD (Apollo -40%, Blackstone -43%, Ares -43%, KKR -46%, Blue Owl -60%) PE dry spell is worse than 2008 (Bain report)

$150bn of loans in CLOs face AI risk (according to JPM)

Tech Fwd PE at par with Consumer Staples

CALENDAR

Earnings releases:

US CrowdStrike (3 March), Broadcom (4), Costco (5)

EU Bayer, Adidas (4 March), Lufthansa (6)

Macro data releases:

US Feb ISM Services (4 March), Feb NFP job report (6)

WHAT ANALYSTS SAY

- UBS: AI disruption and private credit: what is the risk scenario?

- BlackRock: Bond outlook for the first quarter of 2026

UBS, 24 February 2026

Author: Matthew Mish, Strategist

Executive Summary: Quantifying a Tail Risk Scenario

Investors increasingly want to talk about AI disruption and our tail risk scenario: a rapid, severe AI disruption. This is not our baseline ; however, at the risk of Monday morning quarterbacking, over 80% of what is written below was published back in November. What is new: a clearer catalyst (rapid, severe AI disruption).

Here are the key points:

· in a tail scenario, assuming contagion impacts not modelled in our earlier note, we anticipate US HY, LL and PC defaults could rise to 3-6%, 8-10% and 14-15%, respectively. Across these three markets defaults and losses would approach $420bn and $300bn

· in an extreme case, regression analysis suggests US IG, HY and LL spreads could trade to 160-170, 575-675 and 800-900bps

· credit availability will tighten materially, particularly for firms dependent on leveraged finance markets - PC and LL issuance could decline 50-75% YoY.

· financials will be impacted through several channels. One is NFBI loans, currently $2.5tn including all undrawn commitments. In a tail scenario, we estimate $1.6-1.8tn in total drawn exposures, of which about 30-40% is to private equity/credit/BDCs or SPVs/CLOs/ABS and we would consider higher risk.

Private Credit’s Expansion Has Outpaced Economic Growth

Private credit has evolved into a structurally significant segment of the US corporate debt landscape, now rivaling some traditional bank and bond markets. Since 2015, loan markets have grown at a high-single to low-double-digit compound annual rate, with private credit and leveraged loans each representing 6% and 5% of GDP, respectively up from 1% and 5% in 2008. Investment-Grade credit has expanded to 25% of GDP, nearly doubling its 2008 share. This growth reflects a shift in origination from banks to private lenders, driven by regulation and a reach for yield amid low rates. However, the scale relative to GDP raises questions about systemic risk and the market’s capacity to absorb shocks.

Credit Fundamentals Are Deteriorating, Albeit Gradually

While default rates remain contained, stress indicators are rising. Private credit defaults are reportedly between 3% and 5%, and signs of strain such as interest paid-in-kind are nearing post-pandemic highs. Leverage ratios have crept higher, with debt-to-EBITDA reaching 7.5–8x in some sectors when excluding certain earnings adjustments. Interest coverage ratios have ticked higher, but remain under pressure from elevated rates, with middle-market deals hovering in the 1.7-1.8x range. These metrics suggest that while the market is not in crisis, it is increasingly kicking the can down the road and vulnerable to macroeconomic deterioration, sectoral disruptions or liquidity shocks.

Sector Concentration and Structural Weaknesses Amplify Tail Risks

The most acute risk is a sector-specific shock triggering cascading defaults. Historical précédents such as telecom in 2001 and energy in 2016 show how concentrated defaults can drive market-level default rates. One sector can account for 55-80% of market level defaults. Today’s private credit portfolios are heavily weighted toward services (25-30%), technology (20-25%), and healthcare (15-17%). Technology is especially vulnerable to disruption from AI adoption or rapid retrenchment. These risks are compounded by weakening covenants, aggressive earnings adjustments, and opaque valuations. First-lien recoveries in syndicated loans recently fell to the mid-50% range and as low as 30% for energy in 2016 indicating reduced downside protection.

Contagion Risk to Public Credit Markets Is Real and Underappreciated

Private credit stress is unlikely to remain contained. Borrowers increasingly tap both private and syndicated loan markets, with overlapping issuer and sector exposures and shared sponsors. Services and tech represent 15-20% of leveraged loan portfolios, mirroring private credit. On the lender side, the top 20 direct lenders not only dominate private credit AUM but also hold significant stakes in BDCs (45%), leveraged loans (20%), and high-yield bonds (25%). This interconnectedness means that a spike in private defaults could ripple across public markets, widening spreads and impairing liquidity.

Financial Institutions Are Deeply Exposed to Private Credit

Banks and insurers have quietly built substantial exposure to private credit and alternatives. US and European banks hold $1.3 trn in loans and $1.1 bn in undrawn commitments to non-bank financial institutions (NBFIs). GSIBs account for 60% of the total. The fastest-growing categories include loans to SPVs, CLOs and ABS, closed-end investment and mutual funds, and private equity/credit funds and BDCs. Life insurers, specifically those linked to PE sponsors, have increased allocations to private credit and structured products, often relying on internal ratings. This raises concerns about capital adequacy and loss absorption in a downturn, particularly if defaults spike and valuations collapse.

We Don’t Have the Full Mosaic—But Idiosyncratic Risk Provides Opportunity

The private credit market is not in crisis, but the ingredients are present for a severe credit cycle. The key trigger is a shock to one of the key sectors. Size, leverage, sector concentration, and opacity all raise potential systemic risk, but limited transparency and disclosure make a proper calibration of macro risk challenging. Investors must monitor leading indicators defaults, PIKs, covenant breaches, and valuation marks at market and sector levels while demanding better disclosure and underwriting discipline. Policymakers and regulators should assess the implications of bank and insurer exposures, especially as private credit increasingly becomes a core funding source for high-growth sectors. However, overall idiosyncratic risk exposures provide single-name opportunities. Our analysis across banks, insurers, and BDCs globally suggests a wide range of private and alternative exposures could be impacted if we enter a private credit downturn.

BlackRock Investment Institute, 25 February 2026

Authors: Jean Boivin, Global Head of Research

The key message is clear:

we are entering a golden age for fixed income, and the opportunity lies in carry.

For European investors, the reset in yields and improved fundamentals make the region one of the most attractive globally.

In terms of positioning, we highlight the following themes:

· While global growth remains uneven, Europe is showing resilience, supported by easing inflationary pressures and a gradual normalisation of monetary policy. High yield levels, improved credit quality and favourable technical factors are creating a favourable environment for bond investors.

· With nominal yields around 3% and real yields close to 2%, their highest level in over a decade, income is once again becoming a significant driver of performance, after years of zero or negative real rates.

· Strong investor demand is supporting the market: European credit saw record inflows in 2025, as both institutional and retail investors gradually reallocated their cash.

· Changing market dynamics suggest that credit spreads, rather than duration, are now the most relevant source of opportunity. Although spreads are tight, BlackRock anticipates a broadly range-bound environment, with episodes of volatility generating selective entry points rather than continued compression.

· Maintain conviction on carry strategies in the short end of the credit curve, supported by targeted fiscal measures and solid technical factors.

Improvement in eurozone corporate fundamentals, including in the high-yield segment, where credit quality is now higher than in previous cycles.

Contacts

8 Kievyan Street, Yerevan, Armenia

+374 10 712 259

+374 43 004 182

unibankinvest@unibank.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.