The 7 most important words: “Time has come for policy to adjust” J. Powell - meaning the first Fed rate pivot in 4 years

WEEKLY TRENDS

WEEKLY TRENDS

- The US non-farm payrolls were revised down unexpectedly by 818k from April 2023 through March 2024 (adding exceptionally 2.1m jobs instead of 2.9m) showing a much weaker US labour market which Jerome Powell responded to by indicating the Fed was finally preparing to ease rates for the first time in 4 years (a major switch and the beginning of what should be a new and long easing cycle)

- With many participants returning to work, liquidity will also come back, S&P and Nasdaq are both just a few points away from their ATH which most likely will be tested

- Focus will be placed on Nvidia’s Q2 earnings release on Wednesday after the close. Reminder: the FED meets on 17/18 Sep, the ECB on 12 Sep, the BOJ on 19/20, and the BOE on 19 Sep.

MARKETS

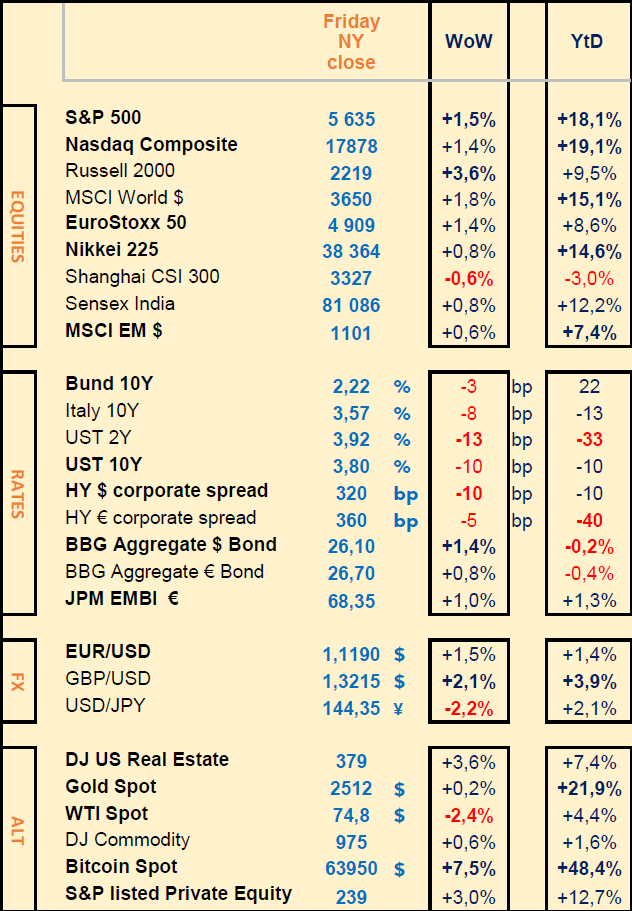

Equities

Another US stock rotation (Russell +3.5% while Nasdaq/S&P +1.5%)

Q2 earnings releases last week (stock WoW performance):

+++ UK JD Sports (+18%), Danish ALK (+14%), Swiss Huber/Suhner (+15%), US Target (+10%) and Swiss Re (+8%)

- - - US Macy’s (-10%), Norway Salmar (-9%), Danish GN (-10%), French Voltalia (-20%) and Dutch Redcare Pharmacy (-12%)

M&A: Walmart divested its 10% JD.com Chinese e-commerce holding (at an 11% discount for $3.6bn)

Analysts: Melrose (-6%) on UBS downgrade

Defense: Rheinmetall (-5%), Hensold (-8%), Saab (-8%)

Rates

US Treasury yields decreased WoW across the curve

Sep Fed rate cuts expected (-25bps, 2/3 chance, -50bps 1/3 chance) in 2024 (-100bps) in 2025 (a further -100bps)

US

Preliminary August PMI (Manufacturing at 48, the lowest reading in 8 months, Services at 55.2)

EU

Preliminary August PMI (Manufacturing at 45.6, Services at 53.3)

Japan

Before parliament on Friday, BOJ’s Governor Ueda said he will continue to adjust the degree of easing (economic forecasts dependent)

Commodities

Despite a much weaker US dollar (DXY index testing its support at 100) Gold and WTI are not benefitting from it. Silver and Aluminium are performing better, Cacao is up 14% Wow

Nota Bene

300 S&P500 stocks outperform the S&P index so far this quarter

Bank of America Global Fund Manager survey shows an August rotation into bonds, cash and healthcare versus equities (Japan and Eurozone)

US start-ups are going bust 7 times higher than in 2019

CALENDAR

WHAT ANALYSTS SAY

UBS, 22 August 2024 - The week ahead : Has the USD weakened too much?

Authors: Chief Investment Office GWM, Investment Research, Dominic Schnider, CFA, CAIA, Strategist

• The USD has weakened across the board recently. The latest pullback has pushed the dollar to key support levels and into oversold territory.

• Besides Jackson Hole, next week, activity data out of Europe, the US, and Japan are in focus and should provide valuable clues about the state of the global economy.

• In view of the recent USD pullback that could be followed by a potential consolidation and the longer term negative picture for the currency, we like to sell the downside risks in EURUSD for yield pickup. Alternatively, we like to be long the TWD vs. the IDR.

USD: Testing key support levels

The USD has weakened in recent weeks, with the initial pullback starting after the softer-than-expected US labor market report. However, the real weakness began to unfold as risk-sentiment recovered and investors sought better USD alternatives. EURUSD has broken above 1.10 and GBPUSD above 1.30. Those round numbers seem important, but even more important are the key technical levels, with EURUSD being close to the December 2023 high of 1.114 and GBPUSD to the July 2023 high of 1.314. The USD is close to such important support/resistance levels in many currency pairs. We believe a weaker USD in coming weeks is increasingly likely. Sharper moves are likely when such longterm highs and lows are being tested amid a changing fundamental backdrop.

EUR: EURUSD looking for new ranges

The EUR has stayed in tight ranges against most European currencies in recent weeks but saw bigger moves mainly against the JPY and recently against the USD. Next week’s most important data will be Europe’s inflation prints, starting Thursday with Spain and Germany, followed by the Eurozone inflation figures on Friday. We expect the numbers to decelerate and be within the expected ranges and therefore not affecting the ECB rate-cutting path. In our view, the ECB is on a predefined cycle of 25bps per quarter, and much would need to happen to change that course. With that view, we see a move higher in EURUSD to be driven mostly by US-centric news. Against other European peers, we see the EUR as slightly weaker.

GBP: The September-pause supports the pound

Next week will be light on the UK data front. Recent datapoints have remained rather upbeat, which led to markets to believe that the Bank of England will be the only major European central bank that will not cut rates in September. We agree with that view and expect the Bank of England to leave rates unchanged in September, delivering the next rate cut most likely in November. That stands in clear contrast to the ECB and the Fed, both of which we expect to cut rates in September. Sterling therefore has a good chance to beat the EUR and the USD in coming weeks, with GBPUSD moving further to 1.30 and EURGBP moving to 0.84.

CHF: One more rate cut

In the context of broad USD weakness, the Swiss franc has benefited over the last week with USDCHF grinding lower. As the Fed braces for a first-rate cut in September and fears of a US recession have alleviated with the latest macro data, other more pro-growth currencies have also rallied, leaving EURCHF stable amid better risk sentiment. Next week is light on Swiss data releases, with only the KOF sentiment indicator and the official reserves print due. The Swiss National Bank’s (SNB) potential activity on FX markets remains in focus, although CHF strength has been moderate lately. Despite a solid flash GDP print, we agree with market expectations of a 25bps rate cut from the SNB in September, which should leave the currency unscathed. EURCHF levels north of 0.96 should be used to hedge EUR longs.

JPY: Near-term consolidation

Japan is due to report retail sales and industrial production data next week, which is likely to show an ongoing improvement in economic dynamics. That said, we believe the BoJ is not in a hurry to hike rates in the coming months, which blunts the potential for another round of yen strength. Moreover, speculative positioning in the yen has already turned slightly net-long. This, coupled with the fact that Fed rate-cut expectations are already well priced, implies the USDJPY exchange rate should remain fairly stable in the near term, in a 145-150 range.

CNY: Policy easing likely to remain reactive and Gradual

CNY is spiralling higher against the USD to 7.13 as broad dollar weakening continued and China kept key lending benchmarks unchanged this week. The People’s Bank of China (PBoC) has been facing a dilemma—between balancing supporting demand and deflation pressures with rate cuts, and managing currency depreciation pressure with stable interest rates. We expect the Fed's imminent rate-cutting cycle to provide a more favorable time window for the PBoC to ease in Q4. China’s side of the story hasn't changed much—portfolio and direct investment inflows remain weak, while USD demand from Chinese corporates recently reached a record high. Given the attractive rates and macro backdrop, investors can consider diversifying their loan exposure with CNY.

ILS: Bank of Israel to stick with caution

The Bank of Israel is likely to keep its policy rate on hold at 4.50% next week, despite disappointing economic growth in 2Q24. Inflation moved above the 3% target again (July: 3.2% y/y) and risks from the war to the budget and shekel remain dominant. The region is still at risk of an escalation in the ongoing conflict and the shekel remains driven by the security backdrop. The currency’s risk premium is high, and while a ceasefire agreement for Gaza could lead to a partial unwind, this has been elusive so far. Israeli and Hamas leadership have failed to reach common ground, even in the face of diplomatic efforts and renewed pressure in recent weeks. The main downside risk for the shekel remains a multi front war with Hezbollah, Iran, and its proxies.

Crude oil: Trading close to 2024 lows

Oil prices are trading close to the lows of this year and have given up most of the spot price gains seen in 2024. Still, investors that have been long crude this year, have made high-single digit returns thanks to roll gains due to a downward-sloped futures curve and the cash collateral from elevated US interest rates. Recession fears in the US following a weak job market report initiated the sell-off, and ongoing ceasefire hopes in Gaza have lowered crude's risk premium. Lastly, weak Chinese crude imports and refinery activity in July sparked fears of poor Chinese oil demand. China used to be an engine of oil demand growth, so the July weakness likely amplified demand concerns. We continue to expect Brent to recover into a USD 85-90/ bbl range over the coming months. Hence, we continue to recommend risk-seeking investors to sell the downside price risks in crude oil.

US natural gas: Lower prices trigger supply reductions

US natural gas prices temporarily fell again below the USD 2/mmbtu mark in early August, before rebounding to USD 2.1/mmbtu more recently. Congestion fears have dragged prices lower, and the lower prices are finally weighing on natural gas production. The outlook for prices in 2025 under a normal winter remains positive, although a large part of that price appreciation is already anticipated by markets. Still, winter weather remains a risk, particularly if it turns out to be very mild. Higher prices are needed in 2025 to support stronger export demand, in our view. High roll costs remain a drag on performance. Hence, we still recommend investors to stay on the sidelines.

Gold: Million-dollar bars

After reaching multiple record highs this year and outperforming major stock indexes, for the first time ever a single gold bar (400 ounces) is worth USD 1m. We believe gold has more room to run and reiterate our positive outlook, with a target of USD 2,600/oz by yearend and USD 2,700/oz by mid-2025. Key factors in our view include a revival of large inflows to ETFs—something that has been missing since April 2022. We also see a pickup in demand from speculators where net-long positions remain far from extreme. Outside these activities, we see central bank net-buying remaining elevated this year and next, albeit moderating from its record pace in 1H24. With holdings relative to total reserve assets still at modest levels and dedollarization trends persisting, we forecast central banks will buy 900-950 metric tonnes in 2024 (vs. +1,000 metric tons in 2023). Jewelry demand has also moderated, but seasonal tailwinds should rise from 4Q24. Moreover, we believe portfolio hedges, like gold, can help manage heightened uncertainty—about 5% within a USD-balanced portfolio is optimal.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+37410 59-55-56

Broker

+374 43 00-43-82

broker@unibankinvest.am

research@unibankinvest.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by OJSC Unibank (registered trademark – Unibank INVEST, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.

Equities

Another US stock rotation (Russell +3.5% while Nasdaq/S&P +1.5%)

Q2 earnings releases last week (stock WoW performance):

+++ UK JD Sports (+18%), Danish ALK (+14%), Swiss Huber/Suhner (+15%), US Target (+10%) and Swiss Re (+8%)

- - - US Macy’s (-10%), Norway Salmar (-9%), Danish GN (-10%), French Voltalia (-20%) and Dutch Redcare Pharmacy (-12%)

M&A: Walmart divested its 10% JD.com Chinese e-commerce holding (at an 11% discount for $3.6bn)

Analysts: Melrose (-6%) on UBS downgrade

Defense: Rheinmetall (-5%), Hensold (-8%), Saab (-8%)

Rates

US Treasury yields decreased WoW across the curve

Sep Fed rate cuts expected (-25bps, 2/3 chance, -50bps 1/3 chance) in 2024 (-100bps) in 2025 (a further -100bps)

US

Preliminary August PMI (Manufacturing at 48, the lowest reading in 8 months, Services at 55.2)

EU

Preliminary August PMI (Manufacturing at 45.6, Services at 53.3)

Japan

Before parliament on Friday, BOJ’s Governor Ueda said he will continue to adjust the degree of easing (economic forecasts dependent)

Commodities

Despite a much weaker US dollar (DXY index testing its support at 100) Gold and WTI are not benefitting from it. Silver and Aluminium are performing better, Cacao is up 14% Wow

Nota Bene

300 S&P500 stocks outperform the S&P index so far this quarter

Bank of America Global Fund Manager survey shows an August rotation into bonds, cash and healthcare versus equities (Japan and Eurozone)

US start-ups are going bust 7 times higher than in 2019

CALENDAR

- Corporate Q2 earnings: in the US Nvidia (28 Aug after close), PDD (26), Salesforce and Crowdstrike (28 Aug), Dell (29 Aug); in Europe Vinci (27), Pernod Ricard (29)

- Economic Data releases: US July PCE inflation (30 Aug)

WHAT ANALYSTS SAY

- UBS - Chief Investment Office GWM - Forex and Commodities

UBS, 22 August 2024 - The week ahead : Has the USD weakened too much?

Authors: Chief Investment Office GWM, Investment Research, Dominic Schnider, CFA, CAIA, Strategist

• The USD has weakened across the board recently. The latest pullback has pushed the dollar to key support levels and into oversold territory.

• Besides Jackson Hole, next week, activity data out of Europe, the US, and Japan are in focus and should provide valuable clues about the state of the global economy.

• In view of the recent USD pullback that could be followed by a potential consolidation and the longer term negative picture for the currency, we like to sell the downside risks in EURUSD for yield pickup. Alternatively, we like to be long the TWD vs. the IDR.

USD: Testing key support levels

The USD has weakened in recent weeks, with the initial pullback starting after the softer-than-expected US labor market report. However, the real weakness began to unfold as risk-sentiment recovered and investors sought better USD alternatives. EURUSD has broken above 1.10 and GBPUSD above 1.30. Those round numbers seem important, but even more important are the key technical levels, with EURUSD being close to the December 2023 high of 1.114 and GBPUSD to the July 2023 high of 1.314. The USD is close to such important support/resistance levels in many currency pairs. We believe a weaker USD in coming weeks is increasingly likely. Sharper moves are likely when such longterm highs and lows are being tested amid a changing fundamental backdrop.

EUR: EURUSD looking for new ranges

The EUR has stayed in tight ranges against most European currencies in recent weeks but saw bigger moves mainly against the JPY and recently against the USD. Next week’s most important data will be Europe’s inflation prints, starting Thursday with Spain and Germany, followed by the Eurozone inflation figures on Friday. We expect the numbers to decelerate and be within the expected ranges and therefore not affecting the ECB rate-cutting path. In our view, the ECB is on a predefined cycle of 25bps per quarter, and much would need to happen to change that course. With that view, we see a move higher in EURUSD to be driven mostly by US-centric news. Against other European peers, we see the EUR as slightly weaker.

GBP: The September-pause supports the pound

Next week will be light on the UK data front. Recent datapoints have remained rather upbeat, which led to markets to believe that the Bank of England will be the only major European central bank that will not cut rates in September. We agree with that view and expect the Bank of England to leave rates unchanged in September, delivering the next rate cut most likely in November. That stands in clear contrast to the ECB and the Fed, both of which we expect to cut rates in September. Sterling therefore has a good chance to beat the EUR and the USD in coming weeks, with GBPUSD moving further to 1.30 and EURGBP moving to 0.84.

CHF: One more rate cut

In the context of broad USD weakness, the Swiss franc has benefited over the last week with USDCHF grinding lower. As the Fed braces for a first-rate cut in September and fears of a US recession have alleviated with the latest macro data, other more pro-growth currencies have also rallied, leaving EURCHF stable amid better risk sentiment. Next week is light on Swiss data releases, with only the KOF sentiment indicator and the official reserves print due. The Swiss National Bank’s (SNB) potential activity on FX markets remains in focus, although CHF strength has been moderate lately. Despite a solid flash GDP print, we agree with market expectations of a 25bps rate cut from the SNB in September, which should leave the currency unscathed. EURCHF levels north of 0.96 should be used to hedge EUR longs.

JPY: Near-term consolidation

Japan is due to report retail sales and industrial production data next week, which is likely to show an ongoing improvement in economic dynamics. That said, we believe the BoJ is not in a hurry to hike rates in the coming months, which blunts the potential for another round of yen strength. Moreover, speculative positioning in the yen has already turned slightly net-long. This, coupled with the fact that Fed rate-cut expectations are already well priced, implies the USDJPY exchange rate should remain fairly stable in the near term, in a 145-150 range.

CNY: Policy easing likely to remain reactive and Gradual

CNY is spiralling higher against the USD to 7.13 as broad dollar weakening continued and China kept key lending benchmarks unchanged this week. The People’s Bank of China (PBoC) has been facing a dilemma—between balancing supporting demand and deflation pressures with rate cuts, and managing currency depreciation pressure with stable interest rates. We expect the Fed's imminent rate-cutting cycle to provide a more favorable time window for the PBoC to ease in Q4. China’s side of the story hasn't changed much—portfolio and direct investment inflows remain weak, while USD demand from Chinese corporates recently reached a record high. Given the attractive rates and macro backdrop, investors can consider diversifying their loan exposure with CNY.

ILS: Bank of Israel to stick with caution

The Bank of Israel is likely to keep its policy rate on hold at 4.50% next week, despite disappointing economic growth in 2Q24. Inflation moved above the 3% target again (July: 3.2% y/y) and risks from the war to the budget and shekel remain dominant. The region is still at risk of an escalation in the ongoing conflict and the shekel remains driven by the security backdrop. The currency’s risk premium is high, and while a ceasefire agreement for Gaza could lead to a partial unwind, this has been elusive so far. Israeli and Hamas leadership have failed to reach common ground, even in the face of diplomatic efforts and renewed pressure in recent weeks. The main downside risk for the shekel remains a multi front war with Hezbollah, Iran, and its proxies.

Crude oil: Trading close to 2024 lows

Oil prices are trading close to the lows of this year and have given up most of the spot price gains seen in 2024. Still, investors that have been long crude this year, have made high-single digit returns thanks to roll gains due to a downward-sloped futures curve and the cash collateral from elevated US interest rates. Recession fears in the US following a weak job market report initiated the sell-off, and ongoing ceasefire hopes in Gaza have lowered crude's risk premium. Lastly, weak Chinese crude imports and refinery activity in July sparked fears of poor Chinese oil demand. China used to be an engine of oil demand growth, so the July weakness likely amplified demand concerns. We continue to expect Brent to recover into a USD 85-90/ bbl range over the coming months. Hence, we continue to recommend risk-seeking investors to sell the downside price risks in crude oil.

US natural gas: Lower prices trigger supply reductions

US natural gas prices temporarily fell again below the USD 2/mmbtu mark in early August, before rebounding to USD 2.1/mmbtu more recently. Congestion fears have dragged prices lower, and the lower prices are finally weighing on natural gas production. The outlook for prices in 2025 under a normal winter remains positive, although a large part of that price appreciation is already anticipated by markets. Still, winter weather remains a risk, particularly if it turns out to be very mild. Higher prices are needed in 2025 to support stronger export demand, in our view. High roll costs remain a drag on performance. Hence, we still recommend investors to stay on the sidelines.

Gold: Million-dollar bars

After reaching multiple record highs this year and outperforming major stock indexes, for the first time ever a single gold bar (400 ounces) is worth USD 1m. We believe gold has more room to run and reiterate our positive outlook, with a target of USD 2,600/oz by yearend and USD 2,700/oz by mid-2025. Key factors in our view include a revival of large inflows to ETFs—something that has been missing since April 2022. We also see a pickup in demand from speculators where net-long positions remain far from extreme. Outside these activities, we see central bank net-buying remaining elevated this year and next, albeit moderating from its record pace in 1H24. With holdings relative to total reserve assets still at modest levels and dedollarization trends persisting, we forecast central banks will buy 900-950 metric tonnes in 2024 (vs. +1,000 metric tons in 2023). Jewelry demand has also moderated, but seasonal tailwinds should rise from 4Q24. Moreover, we believe portfolio hedges, like gold, can help manage heightened uncertainty—about 5% within a USD-balanced portfolio is optimal.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+37410 59-55-56

Broker

+374 43 00-43-82

broker@unibankinvest.am

research@unibankinvest.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by OJSC Unibank (registered trademark – Unibank INVEST, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.