Last week: Fitch downgraded France to single A+; US stocks hit records on controlled US inflation, NFP yearly revision

WEEKLY TRENDS

WEEKLY TRENDS

- Late Friday Fitch rating agency downgraded France long term debt rating to single A+ vs AA– prior, citing political instability and uncertainty over ballooning public finances and record debts

- US CPI for August came out as expected at 2.9% p.a. and PPI came out lower at 2.6%. The BLS reported a large yearly NFP revision (-911 000 jobs creation)

- With a controlled inflation (yet far above the 2% target) the FED is now obliged to pivot towards its other mandate: maximum employment. According to the CME FedWatch tool, the Fed is expected to cut by 25bps on Wednesday and twice after that, before yearend

- US stocks rallied on the FED almost guaranteed cuts and hit new records, so did Gold and BTC. Oil is higher together with EU defense stocks after the Russian drones attack in Poland

- The ECB decided not to cut last week (it sees inflation at +1.9% in 2027) and the BOE/MPC is expected to do just the same on Thursday this week

- Else, against all odds, Oracle hit a record day performance at +36% on Tuesday after the close, as OpenAI ordered $300bn worth of Oracle Cloud

MARKETS

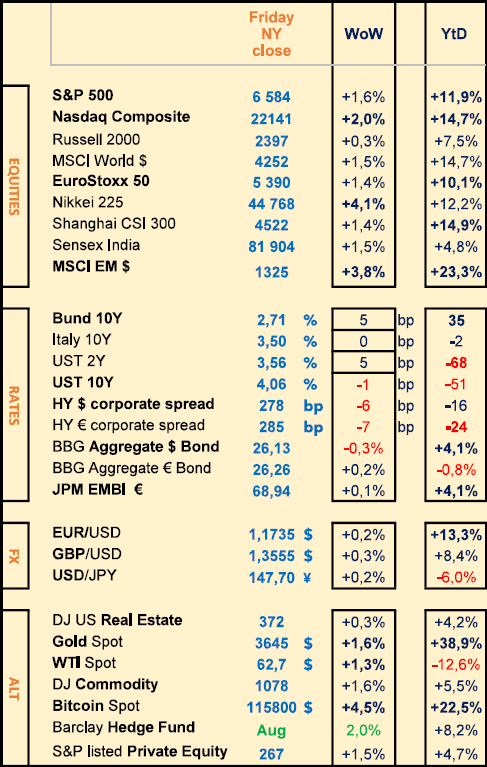

Equities

Specific stock weekly performances:

Oracle (+25% on OpenAI order), Alibaba (+14% on own AI chip), Inditex (+10% on outlook), Thales (+12%), BAE (+11%) on Russian drones in PL

M&A:

Anglo American (+12% merged with Tech Resources for $53bn)

Analysts: Publicis (MS ‘o/w’ target €114), Essilor (Barclays ‘o/w’ target €305), UBS (JPM ‘o/w’ target CHF 38), ABB (DB ‘sell’ target CHF 47)

Rates

US curve (2-10 years) steepening slightly down at 50bps (-5)

HY corporate spreads lower by 5bps (US at 280bps EU at 285bps)

Commodities

Oil price higher (+1.5%) on Russian drones attack in Poland

Gold price higher (+1.5%) new ATH at $3675 an ounce (on FED cuts)

Silver YTD performance is at +37%, while Platinum is at +40%

US

Aug CPI as expected at +2.9% (Core at 3.1%) Aug PPI lower at +2.6% (Core at 2.8%)

Crypto

BTC higher at +4.5% while ETH at +5% SOL at +15% and XRP at +6%. BTC ETF weekly flow (+$1.6bn) vs outstanding $150bn, representing 6.5% global BTC supply (BlackRock’s IBIT has a 40% market share)

Under the watch

France debt rating reviews (Moody’s 24 Oct ; S&P 28 Nov)

US budget and fiscal situation (Oct 14 US court decision over tariffs)

Nota Bene

JP Morgan forecast record US buybacks this year at $600bn

US Secretary for Commerce (Lutnick) pointed to Fannie Mae and Freddie Mac IPO this year

CALENDAR

Earnings releases: US FedEx (18 Sep), EU Vinci (16 Sep), Bolloré (17 Sep)

Macro releases: UK August CPI (17 Sep)

Central bank meetings: FED/FOMC (17 Sep), BOE/MPC (18 Sep)

WHAT ANALYSTS SAY

UBS Global Wealth Management, 8 September 2025

Author: James Mazeau, Economist (Chief Investment Office)

More vulnerable technology stocks

Nevertheless, the sector faces a more complex risk environment. In the short term, the largest platforms could see some pressure on their margins due to their massive investments in AI.

Furthermore, after three years of strong performance, their valuations are no longer cheap, making technology stocks more vulnerable in the event of disappointing results or market mood swings.

The AI theme should reach maturity

Investors are advised to monitor several key catalysts. Firstly, the launch of new advanced AI models, progress in monetisation and forecasts for investment in AI. Secondly, seasonal factors that tend to support or weigh on technology valuations. And thirdly, the possibility of market expansion for advanced chips.

With the Nasdaq having nearly doubled since the launch of ChatGPT in late 2022, the AI theme is likely to mature and investors will need to become increasingly selective. We recommend diversified exposure to all three levels of the AI value chain (semiconductors, software and internet), while taking into account the relative AI sensitivity of the technology companies in their portfolios.

Will US inflation and employment figures accelerate the Fed's monetary easing?

The US Federal Reserve's (Fed) accommodative shift dates back just ten days, but its leaders were quick to point out both the possibility of rate cuts and the fact that these cuts would be conditional on economic statistics.

The PCE (Personal Consumption Expenditures) price index, the Fed's preferred inflation barometer, rose in line with forecasts in July. This should allow the central bank to focus more on the employment aspect of its mandate.

Resumption of the rate-cutting cycle in sight

UBS Research believes that the Fed will resume its rate-cutting cycle in September, with a total reduction of 100 basis points (bp) over the next four meetings. In this environment, high-quality bonds will be favoured in order to guarantee returns above those of cash. In addition, capital gains are expected if monetary policy becomes more accommodative.

Diversified portfolios containing well-selected, medium-duration corporate bonds can help cushion volatility, while gold remains attractive given the prospects for lower real rates and current geopolitical developments. UBS Research expects the price to reach $3,700 per ounce by the end of June 2026.

Carmignac, 8 September 2025

Author: Guillaume Rigeade, Fixed Income Manager

Population growth is slowing in developed countries and productivity gains are becoming scarce. In this world, resorting to debt to stimulate economies has become endemic. This has largely encouraged them to implement costly fiscal policies. The debt of a country such as Japan rose from 70% in the early 1990s to 255% at the end of 2023, placing it among the worst performers alongside Sudan (256%) and Lebanon (283%). The rise in interest rates in Japan has reduced the Japanese government's fiscal room for manoeuvre. It must now struggle to maintain positive growth in a relatively inflationary environment, which is causing increased mistrust among bond investors. The United States is also at the epicentre of fears, as the country is already operating with a significant level of debt (124% of GDP) and relatively short maturities, requiring it to refinance a third of its debt in the next twelve months. The eurozone finds itself in a similar situation, with announcements of record investment plans to ensure sovereignty in defence matters and to modernise infrastructure in order to revive growth in the region, which has been sluggish until now. Most countries have abandoned any form of discipline on their debt levels.

Debt as a driver of growth... up to a point

While Keynesian theory highlights the benefits of increasing public debt to finance labour-intensive projects (including infrastructure), we see certain limitations to this approach. The first cause is that an ineffective debt policy can result in a chronic trade deficit, in which case borrowing fuels a vicious circle of external imbalances. The case of France seems particularly interesting in this regard. The country has seen a sharp increase in its deficit despite repeated attempts at austerity measures, while posting barely positive growth. In addition, certain fundamental forces are only exacerbating the dynamics of government debt, particularly the interest burden on debt. In an environment where key interest rates have been on an upward trend in recent years, each refinancing of French debt results in an increase in this burden.

The Finance Committee's forecasters expect this burden to grow rapidly, reaching €72 billion by 2027, making it the second largest budget item after education. This spending surplus seems difficult to reconcile in the budget, given that income tax revenue amounts to just over €100 billion.

The result of this equation should therefore lead to this burden being financed by an increase in the deficit, which is already hovering at 5.8% of GDP at the end of 2024.

Debt liquidity: a challenge for market fluidity

While most central banks are able to reconcile the potential turmoil between ever-increasing debt supply and subdued investor demand, we are already seeing some disruption. Some recent auctions in Japan and the United States have met with timid demand, as investors are becoming increasingly critical of fiscal instability. A reversal of a £5 billion (0.2% of UK GDP) austerity plan on social benefits across the Channel was enough to trigger a sharp rise in UK interest rates. This is very bad news for the UK Debt Management Office, with yields on 20-year and longer maturities hovering above the levels seen at the peak of the crisis of confidence in Liz Truss's government in 2022.

Furthermore, the negative impact of higher long-term rates on the rest of the economy should not be overlooked, with a high potential for contagion to other financial and real assets.

If the future looks relatively bleak given these fiscal missteps, where can the light at the end of the tunnel be found?

Three main scenarios are emerging. Some advocate a top-down approach: ‘grow your way out of it’. Others, more interventionist, are banking on the idea of ‘print your way out of it’.But these strategies are coming up against an increasingly unstable environment. Japan, long held up as a laboratory for the sustainability of high debt thanks to massively negative real interest rates, shows that this model only works as long as long-term rates remain anchored – and natural buyers persist. In this context, light could also come from active and opportunistic management of bond portfolios.

Vanguard, 10 September 2025

Author: Joe Davis, World Chief Economist

Regardless of whether the economic impact of AI is positive or negative, the future could be conducive to active risk-taking in the bond markets. The interest rate environment is likely to be very different from what we experienced between 1983 and 2020. That period was very favourable for all bond investors. In a higher interest rate environment, active risk-taking is more likely to generate value.

Our research indicates a higher neutral rate in the United States over the next decade, compared to the low interest rate environment that prevailed before the Covid crisis, partly due to factors such as population ageing and rising structural deficits.

We therefore believe that US interest rates will remain above pre-pandemic levels for a long time. In all of our scenarios for the impact of AI on economic growth, we expect the US federal funds rate to remain above 4%, but for different reasons.

In the positive scenario

the 4% rate reflects higher economic growth. The yield curve could then remain flatter than some believe, creating opportunities for active risk-taking on duration. There may also be similar dynamics around credit.

In the pessimistic scenario

they indicate growing structural deficits and financial pressures on the US government. Inflationary pressures could also be stronger in this scenario. This would likely be a very different environment, in which rates could rise and the curve could steepen, creating opportunities for active risk-taking. Higher interest rates for a longer period of time would mean that price increases on securities would yield less and reinvestment at higher rates would yield more. Overall, we would enter an era where bonds offer more value in a portfolio than they did in the low interest rate environment that followed the global financial crisis.

In terms of active management within a bond allocation, neither environment appears as ‘easy’ as it may have been in previous decades, when interest rates had been on a downward trend since 1983. There will be many sources of volatility to navigate in order to mitigate the potentially negative price effects of a rising yield environment or to take advantage of price disruptions. In any case, the coming decade seems conducive to active management, as there will likely be sources of volatility to manage or exploit.

This seems particularly important if AI disappoints. In this scenario, underweighting equities and overweighting bonds could be beneficial, as this environment is expected to bring weaker growth, disappointing earnings growth and higher interest rates. Within their bond allocation, investors may benefit from overweighting corporate bonds (including high yield) relative to US Treasuries. This is because Treasury prices could come under pressure if investors become concerned about the sustainability of the US government's budget deficit.

Equities

Specific stock weekly performances:

Oracle (+25% on OpenAI order), Alibaba (+14% on own AI chip), Inditex (+10% on outlook), Thales (+12%), BAE (+11%) on Russian drones in PL

M&A:

Anglo American (+12% merged with Tech Resources for $53bn)

Analysts: Publicis (MS ‘o/w’ target €114), Essilor (Barclays ‘o/w’ target €305), UBS (JPM ‘o/w’ target CHF 38), ABB (DB ‘sell’ target CHF 47)

Rates

US curve (2-10 years) steepening slightly down at 50bps (-5)

HY corporate spreads lower by 5bps (US at 280bps EU at 285bps)

Commodities

Oil price higher (+1.5%) on Russian drones attack in Poland

Gold price higher (+1.5%) new ATH at $3675 an ounce (on FED cuts)

Silver YTD performance is at +37%, while Platinum is at +40%

US

Aug CPI as expected at +2.9% (Core at 3.1%) Aug PPI lower at +2.6% (Core at 2.8%)

Crypto

BTC higher at +4.5% while ETH at +5% SOL at +15% and XRP at +6%. BTC ETF weekly flow (+$1.6bn) vs outstanding $150bn, representing 6.5% global BTC supply (BlackRock’s IBIT has a 40% market share)

Under the watch

France debt rating reviews (Moody’s 24 Oct ; S&P 28 Nov)

US budget and fiscal situation (Oct 14 US court decision over tariffs)

Nota Bene

JP Morgan forecast record US buybacks this year at $600bn

US Secretary for Commerce (Lutnick) pointed to Fannie Mae and Freddie Mac IPO this year

CALENDAR

Earnings releases: US FedEx (18 Sep), EU Vinci (16 Sep), Bolloré (17 Sep)

Macro releases: UK August CPI (17 Sep)

Central bank meetings: FED/FOMC (17 Sep), BOE/MPC (18 Sep)

WHAT ANALYSTS SAY

- UBS: Technology sector: catalysts to watch

- Carmignac: Budgetary derailment: the markets wake up

- Vanguard: Active bond management in the age of AI

UBS Global Wealth Management, 8 September 2025

Author: James Mazeau, Economist (Chief Investment Office)

More vulnerable technology stocks

Nevertheless, the sector faces a more complex risk environment. In the short term, the largest platforms could see some pressure on their margins due to their massive investments in AI.

Furthermore, after three years of strong performance, their valuations are no longer cheap, making technology stocks more vulnerable in the event of disappointing results or market mood swings.

The AI theme should reach maturity

Investors are advised to monitor several key catalysts. Firstly, the launch of new advanced AI models, progress in monetisation and forecasts for investment in AI. Secondly, seasonal factors that tend to support or weigh on technology valuations. And thirdly, the possibility of market expansion for advanced chips.

With the Nasdaq having nearly doubled since the launch of ChatGPT in late 2022, the AI theme is likely to mature and investors will need to become increasingly selective. We recommend diversified exposure to all three levels of the AI value chain (semiconductors, software and internet), while taking into account the relative AI sensitivity of the technology companies in their portfolios.

Will US inflation and employment figures accelerate the Fed's monetary easing?

The US Federal Reserve's (Fed) accommodative shift dates back just ten days, but its leaders were quick to point out both the possibility of rate cuts and the fact that these cuts would be conditional on economic statistics.

The PCE (Personal Consumption Expenditures) price index, the Fed's preferred inflation barometer, rose in line with forecasts in July. This should allow the central bank to focus more on the employment aspect of its mandate.

Resumption of the rate-cutting cycle in sight

UBS Research believes that the Fed will resume its rate-cutting cycle in September, with a total reduction of 100 basis points (bp) over the next four meetings. In this environment, high-quality bonds will be favoured in order to guarantee returns above those of cash. In addition, capital gains are expected if monetary policy becomes more accommodative.

Diversified portfolios containing well-selected, medium-duration corporate bonds can help cushion volatility, while gold remains attractive given the prospects for lower real rates and current geopolitical developments. UBS Research expects the price to reach $3,700 per ounce by the end of June 2026.

Carmignac, 8 September 2025

Author: Guillaume Rigeade, Fixed Income Manager

Population growth is slowing in developed countries and productivity gains are becoming scarce. In this world, resorting to debt to stimulate economies has become endemic. This has largely encouraged them to implement costly fiscal policies. The debt of a country such as Japan rose from 70% in the early 1990s to 255% at the end of 2023, placing it among the worst performers alongside Sudan (256%) and Lebanon (283%). The rise in interest rates in Japan has reduced the Japanese government's fiscal room for manoeuvre. It must now struggle to maintain positive growth in a relatively inflationary environment, which is causing increased mistrust among bond investors. The United States is also at the epicentre of fears, as the country is already operating with a significant level of debt (124% of GDP) and relatively short maturities, requiring it to refinance a third of its debt in the next twelve months. The eurozone finds itself in a similar situation, with announcements of record investment plans to ensure sovereignty in defence matters and to modernise infrastructure in order to revive growth in the region, which has been sluggish until now. Most countries have abandoned any form of discipline on their debt levels.

Debt as a driver of growth... up to a point

While Keynesian theory highlights the benefits of increasing public debt to finance labour-intensive projects (including infrastructure), we see certain limitations to this approach. The first cause is that an ineffective debt policy can result in a chronic trade deficit, in which case borrowing fuels a vicious circle of external imbalances. The case of France seems particularly interesting in this regard. The country has seen a sharp increase in its deficit despite repeated attempts at austerity measures, while posting barely positive growth. In addition, certain fundamental forces are only exacerbating the dynamics of government debt, particularly the interest burden on debt. In an environment where key interest rates have been on an upward trend in recent years, each refinancing of French debt results in an increase in this burden.

The Finance Committee's forecasters expect this burden to grow rapidly, reaching €72 billion by 2027, making it the second largest budget item after education. This spending surplus seems difficult to reconcile in the budget, given that income tax revenue amounts to just over €100 billion.

The result of this equation should therefore lead to this burden being financed by an increase in the deficit, which is already hovering at 5.8% of GDP at the end of 2024.

Debt liquidity: a challenge for market fluidity

While most central banks are able to reconcile the potential turmoil between ever-increasing debt supply and subdued investor demand, we are already seeing some disruption. Some recent auctions in Japan and the United States have met with timid demand, as investors are becoming increasingly critical of fiscal instability. A reversal of a £5 billion (0.2% of UK GDP) austerity plan on social benefits across the Channel was enough to trigger a sharp rise in UK interest rates. This is very bad news for the UK Debt Management Office, with yields on 20-year and longer maturities hovering above the levels seen at the peak of the crisis of confidence in Liz Truss's government in 2022.

Furthermore, the negative impact of higher long-term rates on the rest of the economy should not be overlooked, with a high potential for contagion to other financial and real assets.

If the future looks relatively bleak given these fiscal missteps, where can the light at the end of the tunnel be found?

Three main scenarios are emerging. Some advocate a top-down approach: ‘grow your way out of it’. Others, more interventionist, are banking on the idea of ‘print your way out of it’.But these strategies are coming up against an increasingly unstable environment. Japan, long held up as a laboratory for the sustainability of high debt thanks to massively negative real interest rates, shows that this model only works as long as long-term rates remain anchored – and natural buyers persist. In this context, light could also come from active and opportunistic management of bond portfolios.

Vanguard, 10 September 2025

Author: Joe Davis, World Chief Economist

Regardless of whether the economic impact of AI is positive or negative, the future could be conducive to active risk-taking in the bond markets. The interest rate environment is likely to be very different from what we experienced between 1983 and 2020. That period was very favourable for all bond investors. In a higher interest rate environment, active risk-taking is more likely to generate value.

Our research indicates a higher neutral rate in the United States over the next decade, compared to the low interest rate environment that prevailed before the Covid crisis, partly due to factors such as population ageing and rising structural deficits.

We therefore believe that US interest rates will remain above pre-pandemic levels for a long time. In all of our scenarios for the impact of AI on economic growth, we expect the US federal funds rate to remain above 4%, but for different reasons.

In the positive scenario

the 4% rate reflects higher economic growth. The yield curve could then remain flatter than some believe, creating opportunities for active risk-taking on duration. There may also be similar dynamics around credit.

In the pessimistic scenario

they indicate growing structural deficits and financial pressures on the US government. Inflationary pressures could also be stronger in this scenario. This would likely be a very different environment, in which rates could rise and the curve could steepen, creating opportunities for active risk-taking. Higher interest rates for a longer period of time would mean that price increases on securities would yield less and reinvestment at higher rates would yield more. Overall, we would enter an era where bonds offer more value in a portfolio than they did in the low interest rate environment that followed the global financial crisis.

In terms of active management within a bond allocation, neither environment appears as ‘easy’ as it may have been in previous decades, when interest rates had been on a downward trend since 1983. There will be many sources of volatility to navigate in order to mitigate the potentially negative price effects of a rising yield environment or to take advantage of price disruptions. In any case, the coming decade seems conducive to active management, as there will likely be sources of volatility to manage or exploit.

This seems particularly important if AI disappoints. In this scenario, underweighting equities and overweighting bonds could be beneficial, as this environment is expected to bring weaker growth, disappointing earnings growth and higher interest rates. Within their bond allocation, investors may benefit from overweighting corporate bonds (including high yield) relative to US Treasuries. This is because Treasury prices could come under pressure if investors become concerned about the sustainability of the US government's budget deficit.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+374 43 00-43-82

Broker

broker@unibankinvest.am

research@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.