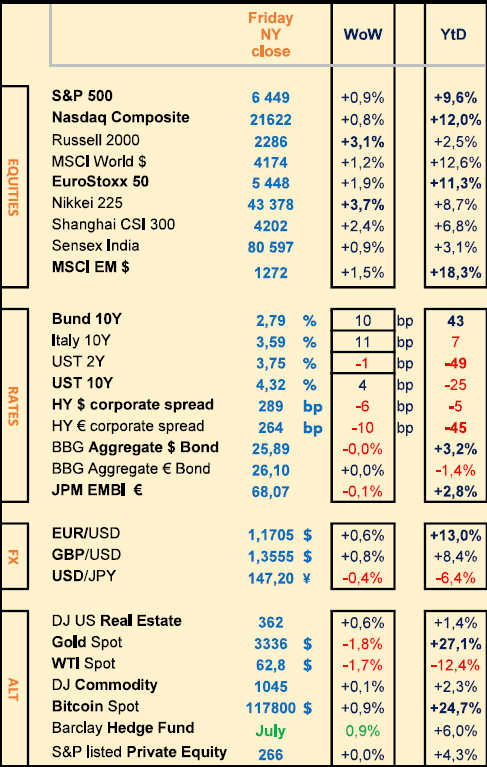

Last week: new ATH for US stocks on Sep FED rate cut expectation, due to lower US July CPI and hope of a UA-RU truce

WEEKLY TRENDS

WEEKLY TRENDS

- Lower July US headline CPI (Core was higher) coupled with hopes of a Ukraine-Russia conflict truce, and despite higher July US PPI, all stock indices progressed last week, with the Russell 2000 and the Nikkei 225 the most

- Short dated rates did not move much (longer end went up) the USD was slightly lower and the BTC slightly higher. Gold and Oil weakened on higher long US rates and hope of a Ukraine-Russia truce

- Meanwhile Trump decided to extend by 90 days his new tariffs on imported goods from China and cancelled his new tariffs on Gold

- All eyes will be on the Jackson Hole central bankers’ symposium next week, with ‘la pièce de résistance’ on Friday when Powell speaks. Interesting time with a not so well and revised US job market, added to a US strong inflation (stronger than the FED’s 2% target) and with a constant pressure from president Trump and treasury secretary Bessent

MARKETS

Equities

Earnings released stock weekly performances:

Tencent (+5%), TUI (+18%), Valneva (+26%)

Intel (+23%) on a rumoured potential stake from the US state

Cisco (-8%), Orsted (-32%), Corewave (-22%), Hapag Lloyd (-8%)

Rates

US curve (2-10 years) steepening higher at 57bps (+5). Long Bond yields higher (+10bps). The CME FedWatch tool now predicts a 93% probability of a 25bps FED cut in Sep, added to a 25bps cut in Oct and in December.

HY corporate spreads lower at 290bps for US (-5) at 265bps for EU (-10)

Commodities

Oil price lower (-1.5% on potential truce in UA) -7% for the month

Gold price lower (-2%, the worst week since June)

US

July CPI Headline at +2.7% yoy (vs +2.8% expected) Core at +3.1% yoy

July PPI (+0.9%, the biggest monthly rise since June 2022)

China

PBOC is to boost financing support for tech, consumption growth

Crypto

Solana (the SEC delayed its decision on a Solana ETF until Oct 16)

Under the watch

France-Italy Bond yields convergence (France’s 10 year Bond yield is just 0.15% below Italy’s, the closest since the 2008 crisis).

Nota Bene

Warren Buffet portfolio Q2 shakeup (+$1.6bn bet on UnitedHealth, exited $1bn stake in T-Mobile, trimmed Apple, Coca-Cola, Chevron and BofA)

SP500 (now has 27% of its value in stocks that have a P/E of at least 50, only one has a P/E less than 10, Comcast). US tech stocks make 45% of the SP500 and the top 10 stocks command a 40% share.

CALENDAR

Upcoming earnings releases:

US HomeDepot (19 Aug), Analog Devices, Target, Alcon (20), Walmart (21)

UK BHP (19 Aug)

Upcoming central bank meetings: Jackson Hole (21-23 Aug), ECB (11 Sep), FED/FOMC (17 Sep), BOE/MPC (18 Sep)

WHAT ANALYSTS SAY

Aberdeen Investments, 14 August 2025

Author: Paola Bissoli, Business Development Director

Many investors follow the growth narrative – driven by tech giants, passive investing and global megatrends. But they often overlook one key element: income via dividends. Emerging markets are no longer just about growth. Over the past two decades, the number of companies paying dividends has risen sharply. Today, around 85% of emerging market companies pay dividends – a level comparable to that of developed markets. Nearly 40% of them offer a yield of more than 3%. What is surprising is that these dividends do not come solely from mature companies. Many are dynamic companies with strong balance sheets, robust cash flows and sustained growth – in sectors ranging from technology and infrastructure to consumer goods.

Saudi Arabia, the Emirates, Qatar and Oman: promising prospects

Markets such as Saudi Arabia and the United Arab Emirates, the most liquid and investable in the region, are home to certain companies with high dividends and robust growth potential. Even in commodity-driven economies, it is possible to practise rigorous stock selection – identifying companies whose specific characteristics can overcome macroeconomic and geopolitical headwinds. Saudi Arabia is benefiting from social reforms and demographic changes. The emergence of a growing consumer class makes companies such as Saudi National Bank (SNB) and Alkhorayef Water & Power Technologies particularly attractive – the latter operating in the essential water and wastewater treatment sectors.

The United Arab Emirates stands out for its liberal economy and international openness. A prime example is Empower (Emirates Central Cooling Systems Corporation), a provider of urban cooling solutions with an ambitious dividend policy. Around 70% of the country's electricity consumption is used for cooling, highlighting the relevance of the company. The local IPO market is also growing, with part of the growth in stock market indices being driven by new listed companies.

Qatar offers interesting opportunities related to the development of LNG as a transition fuel. Two companies are worth mentioning in this regard: Nakilat (Qatar Gas Transport Company Ltd.), which operates LNG carriers worldwide, and Milaha (Qatar Navigation), which is active in logistics, ship repair and port services. In Oman, still considered a frontier market, signs of momentum are emerging. Planned IPOs of public companies, particularly in energy and logistics, could offer opportunities for long-term investors willing to position themselves early.

Investors would be wise to reconsider their geographical biases. The combination of high and rising yields, solid fundamentals and growing regional importance makes emerging market income an attractive source of total return – well beyond the simple growth narrative. The Middle East, in particular, is becoming an area to watch closely, as a region that is still under-analysed and under-owned, offering a unique mix of structural transformation (diversification away from oil), a dynamic population, government-supported market development and listed companies combining growth potential with generous dividend payments.

Shroders, 14 August 2025

Author: Johanna Kyrlund, Group Chief Investment Officer

The main cloud on the horizon from a growth perspective is clearly the uncertainty surrounding tariffs, with a lack of clarity regarding their final rate and possible exemptions. Trump's postponement of the deadline for negotiating trade agreements, accompanied by aggressive rhetoric towards his partners, has not eased tensions. Market reactions to tariff threats have been muted, suggesting that investors view these announcements as a starting point in a broader negotiation process. While this interpretation has proven largely correct so far, it introduces the risk that markets may ultimately underestimate the US president's willingness to implement significantly higher tariffs than currently anticipated.

Our baseline scenario remains an effective tax rate of 12% – the highest level in post-war history, but one that implies that agreements will be reached. This leads us to believe that the risk of recession in the US is low, especially as the labour market remains strong and energy prices are contained.

We remain positive on equities, but the risks are skewed towards stagflation in the United States as the lagged effects of tariffs begin to impact the economy.

The biggest drag on equities is the extent to which bond markets can absorb the growing levels of debt resulting from increased government spending. James Carville, President Clinton's political advisor, said: ‘I'd like to come back in the form of the bond market. You can intimidate everyone.’

The Trump administration has taken an interest in the bond market and seems to understand the importance of its stability. Inflation expectations remain under control. Overall, the signs are still benign, but I am nevertheless monitoring a few trends:

First, the steepening of the long end of the yield curve. Long-term bond yields are rising faster than short-term bond yields, suggesting that concerns about spending are gradually being factored into bond valuations. There is no doubt that the long end of the curve is becoming more volatile.

Second, we need to monitor how Trump treats the Federal Reserve (Fed); a credible central bank is essential for the bond market to function properly, and how the succession of Fed Chair Jerome Powell is handled will be closely analysed.

Given rising debt levels, we continue to view bonds as an attractive source of yield, but not as a source of diversification. As we have emphasised on several occasions, we favour gold for this purpose.

Finally, a word on the US dollar. In discussions with clients around the world, I see that strategic allocations to the greenback are under review. After years of strong US outperformance, starting levels of dollar exposure are quite high, and there is recognition that some diversification is needed. However, these changes will take time. The dollar continues to offer unrivalled liquidity, so care must be taken not to overdo it.

As always when faced with daily headlines, investors must remain focused on medium-term trends. Despite changes in political consensus and asset correlations, our job as active managers remains the same: analyse fundamentals, examine risks, make decisions in the face of uncertainty and remain patient in our quest for performance.

UBP, 13 August 2025

Author: Michaël Lok, Group CIO, CO-CEO AM

Overly defensive positioning has failed to benefit from fluctuations stemming from tariff tensions. This excessive caution weighed on the semi-annual performances of portfolios overweight in cash. In our view, this trend is likely to intensify in the next few months, as the forthcoming rate cuts will further raise the opportunity cost of an outsized cash allocation.

Positive earnings surprise

American exceptionalism continues to hold its ground amid macroeconomic uncertainty. Over 70% of S&P 500 companies have beaten earnings estimates, with 82% surpassing revenue expectations. US banks kicked off the earnings season with upbeat signals on growth and consumer resilience amid inflationary pressure.

Notably, technology stocks have delivered significant surprises on the upside. Following Alphabet’s strong results, Meta reported accelerating sales growth while unveiling ambitious AI investment plans. Microsoft also posted robust gains in its cloud division, driven by sustained AI demand, while Apple recorded its strongest quarterly revenue growth in over three years. More mixed were Amazon’s results, which were dampened by cautious guidance for its cloud segment and significant AI-related spending.

The scope for a broad rally remains contained

A string of trade agreements between the US and key partners – as well as ongoing discussions with others – are helping to ease concerns about a trade war. In this period of détente, investors are progressively refocusing on economic indicators and corporate fundamentals.

Despite all these positive developments, the shrinking risk premium of 3.1% is constraining the equity upside, while the 10-year Treasury yield reaches 4.2%. This compounds demanding valuations, with the S&P 500 trading at 22.4 times forward earnings.

In fixed income, opting for a carry strategy focused on high-yield instruments may offer a buffer against the consequences of lower interest rates. In fact, year-to-date, USD-denominated high-yield bonds and subordinated bank debt (AT1s) have each returned 6.5%, outperforming the 10-year US Treasury, which stands at 4.4%.

In this environment, we favour a diversified allocation across asset classes to manage risk without sacrificing returns. Underinvested portfolios miss out not only on potential capital appreciation in equities and bonds, but also on the regular income derived from dividends and coupons.

Equities

Earnings released stock weekly performances:

Tencent (+5%), TUI (+18%), Valneva (+26%)

Intel (+23%) on a rumoured potential stake from the US state

Cisco (-8%), Orsted (-32%), Corewave (-22%), Hapag Lloyd (-8%)

Rates

US curve (2-10 years) steepening higher at 57bps (+5). Long Bond yields higher (+10bps). The CME FedWatch tool now predicts a 93% probability of a 25bps FED cut in Sep, added to a 25bps cut in Oct and in December.

HY corporate spreads lower at 290bps for US (-5) at 265bps for EU (-10)

Commodities

Oil price lower (-1.5% on potential truce in UA) -7% for the month

Gold price lower (-2%, the worst week since June)

US

July CPI Headline at +2.7% yoy (vs +2.8% expected) Core at +3.1% yoy

July PPI (+0.9%, the biggest monthly rise since June 2022)

China

PBOC is to boost financing support for tech, consumption growth

Crypto

Solana (the SEC delayed its decision on a Solana ETF until Oct 16)

Under the watch

France-Italy Bond yields convergence (France’s 10 year Bond yield is just 0.15% below Italy’s, the closest since the 2008 crisis).

Nota Bene

Warren Buffet portfolio Q2 shakeup (+$1.6bn bet on UnitedHealth, exited $1bn stake in T-Mobile, trimmed Apple, Coca-Cola, Chevron and BofA)

SP500 (now has 27% of its value in stocks that have a P/E of at least 50, only one has a P/E less than 10, Comcast). US tech stocks make 45% of the SP500 and the top 10 stocks command a 40% share.

CALENDAR

Upcoming earnings releases:

US HomeDepot (19 Aug), Analog Devices, Target, Alcon (20), Walmart (21)

UK BHP (19 Aug)

Upcoming central bank meetings: Jackson Hole (21-23 Aug), ECB (11 Sep), FED/FOMC (17 Sep), BOE/MPC (18 Sep)

WHAT ANALYSTS SAY

- Aberdeen: Underestimated: dividend gems in the Middle East

- Shroders: Uncertainty reigns, but the bond market holds the key

- UBP: Staying invested remains a strategic lever

Aberdeen Investments, 14 August 2025

Author: Paola Bissoli, Business Development Director

Many investors follow the growth narrative – driven by tech giants, passive investing and global megatrends. But they often overlook one key element: income via dividends. Emerging markets are no longer just about growth. Over the past two decades, the number of companies paying dividends has risen sharply. Today, around 85% of emerging market companies pay dividends – a level comparable to that of developed markets. Nearly 40% of them offer a yield of more than 3%. What is surprising is that these dividends do not come solely from mature companies. Many are dynamic companies with strong balance sheets, robust cash flows and sustained growth – in sectors ranging from technology and infrastructure to consumer goods.

Saudi Arabia, the Emirates, Qatar and Oman: promising prospects

Markets such as Saudi Arabia and the United Arab Emirates, the most liquid and investable in the region, are home to certain companies with high dividends and robust growth potential. Even in commodity-driven economies, it is possible to practise rigorous stock selection – identifying companies whose specific characteristics can overcome macroeconomic and geopolitical headwinds. Saudi Arabia is benefiting from social reforms and demographic changes. The emergence of a growing consumer class makes companies such as Saudi National Bank (SNB) and Alkhorayef Water & Power Technologies particularly attractive – the latter operating in the essential water and wastewater treatment sectors.

The United Arab Emirates stands out for its liberal economy and international openness. A prime example is Empower (Emirates Central Cooling Systems Corporation), a provider of urban cooling solutions with an ambitious dividend policy. Around 70% of the country's electricity consumption is used for cooling, highlighting the relevance of the company. The local IPO market is also growing, with part of the growth in stock market indices being driven by new listed companies.

Qatar offers interesting opportunities related to the development of LNG as a transition fuel. Two companies are worth mentioning in this regard: Nakilat (Qatar Gas Transport Company Ltd.), which operates LNG carriers worldwide, and Milaha (Qatar Navigation), which is active in logistics, ship repair and port services. In Oman, still considered a frontier market, signs of momentum are emerging. Planned IPOs of public companies, particularly in energy and logistics, could offer opportunities for long-term investors willing to position themselves early.

Investors would be wise to reconsider their geographical biases. The combination of high and rising yields, solid fundamentals and growing regional importance makes emerging market income an attractive source of total return – well beyond the simple growth narrative. The Middle East, in particular, is becoming an area to watch closely, as a region that is still under-analysed and under-owned, offering a unique mix of structural transformation (diversification away from oil), a dynamic population, government-supported market development and listed companies combining growth potential with generous dividend payments.

Shroders, 14 August 2025

Author: Johanna Kyrlund, Group Chief Investment Officer

The main cloud on the horizon from a growth perspective is clearly the uncertainty surrounding tariffs, with a lack of clarity regarding their final rate and possible exemptions. Trump's postponement of the deadline for negotiating trade agreements, accompanied by aggressive rhetoric towards his partners, has not eased tensions. Market reactions to tariff threats have been muted, suggesting that investors view these announcements as a starting point in a broader negotiation process. While this interpretation has proven largely correct so far, it introduces the risk that markets may ultimately underestimate the US president's willingness to implement significantly higher tariffs than currently anticipated.

Our baseline scenario remains an effective tax rate of 12% – the highest level in post-war history, but one that implies that agreements will be reached. This leads us to believe that the risk of recession in the US is low, especially as the labour market remains strong and energy prices are contained.

We remain positive on equities, but the risks are skewed towards stagflation in the United States as the lagged effects of tariffs begin to impact the economy.

The biggest drag on equities is the extent to which bond markets can absorb the growing levels of debt resulting from increased government spending. James Carville, President Clinton's political advisor, said: ‘I'd like to come back in the form of the bond market. You can intimidate everyone.’

The Trump administration has taken an interest in the bond market and seems to understand the importance of its stability. Inflation expectations remain under control. Overall, the signs are still benign, but I am nevertheless monitoring a few trends:

First, the steepening of the long end of the yield curve. Long-term bond yields are rising faster than short-term bond yields, suggesting that concerns about spending are gradually being factored into bond valuations. There is no doubt that the long end of the curve is becoming more volatile.

Second, we need to monitor how Trump treats the Federal Reserve (Fed); a credible central bank is essential for the bond market to function properly, and how the succession of Fed Chair Jerome Powell is handled will be closely analysed.

Given rising debt levels, we continue to view bonds as an attractive source of yield, but not as a source of diversification. As we have emphasised on several occasions, we favour gold for this purpose.

Finally, a word on the US dollar. In discussions with clients around the world, I see that strategic allocations to the greenback are under review. After years of strong US outperformance, starting levels of dollar exposure are quite high, and there is recognition that some diversification is needed. However, these changes will take time. The dollar continues to offer unrivalled liquidity, so care must be taken not to overdo it.

As always when faced with daily headlines, investors must remain focused on medium-term trends. Despite changes in political consensus and asset correlations, our job as active managers remains the same: analyse fundamentals, examine risks, make decisions in the face of uncertainty and remain patient in our quest for performance.

UBP, 13 August 2025

Author: Michaël Lok, Group CIO, CO-CEO AM

Overly defensive positioning has failed to benefit from fluctuations stemming from tariff tensions. This excessive caution weighed on the semi-annual performances of portfolios overweight in cash. In our view, this trend is likely to intensify in the next few months, as the forthcoming rate cuts will further raise the opportunity cost of an outsized cash allocation.

Positive earnings surprise

American exceptionalism continues to hold its ground amid macroeconomic uncertainty. Over 70% of S&P 500 companies have beaten earnings estimates, with 82% surpassing revenue expectations. US banks kicked off the earnings season with upbeat signals on growth and consumer resilience amid inflationary pressure.

Notably, technology stocks have delivered significant surprises on the upside. Following Alphabet’s strong results, Meta reported accelerating sales growth while unveiling ambitious AI investment plans. Microsoft also posted robust gains in its cloud division, driven by sustained AI demand, while Apple recorded its strongest quarterly revenue growth in over three years. More mixed were Amazon’s results, which were dampened by cautious guidance for its cloud segment and significant AI-related spending.

The scope for a broad rally remains contained

A string of trade agreements between the US and key partners – as well as ongoing discussions with others – are helping to ease concerns about a trade war. In this period of détente, investors are progressively refocusing on economic indicators and corporate fundamentals.

Despite all these positive developments, the shrinking risk premium of 3.1% is constraining the equity upside, while the 10-year Treasury yield reaches 4.2%. This compounds demanding valuations, with the S&P 500 trading at 22.4 times forward earnings.

In fixed income, opting for a carry strategy focused on high-yield instruments may offer a buffer against the consequences of lower interest rates. In fact, year-to-date, USD-denominated high-yield bonds and subordinated bank debt (AT1s) have each returned 6.5%, outperforming the 10-year US Treasury, which stands at 4.4%.

In this environment, we favour a diversified allocation across asset classes to manage risk without sacrificing returns. Underinvested portfolios miss out not only on potential capital appreciation in equities and bonds, but also on the regular income derived from dividends and coupons.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+374 43 00-43-82

Broker

broker@unibankinvest.am

research@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.