Last week : Oil much higher (+13%), US stock indices new ATH led by Tech, Gold lower (-2.5%) PE lower (-4%) Yields higher

WEEKLY TRENDS

WEEKLY TRENDS

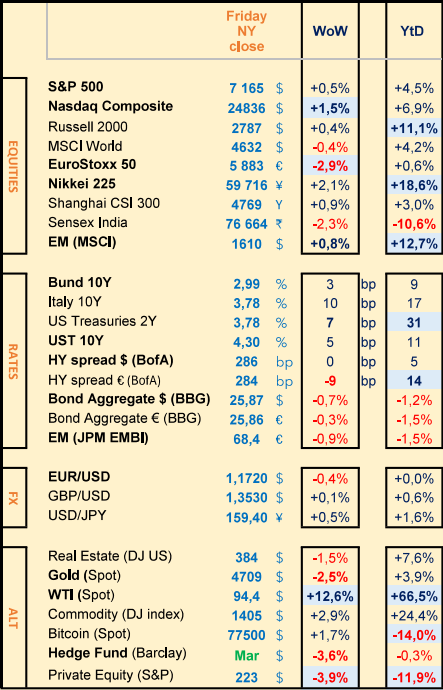

- SP500 at new record high, led by Tech and semi-conductors (Nvidia at new record high, AMD at +23%, Intel at +20% and TI at +19% WoW). Strong US Corporate earnings (84% of the SP500 stocks have now released their Q1 earnings better than estimates with an earnings growth rate of 15.1%).

- European stock indices were lower (Defense stocks like Thales showed a negative performance at -12% and Safran at -14% WoW). Oil was much higher at +13% but this was after an inverse move the previous week (-13%), note that former discounts on Russian and Iranian oil have turned into premia now. Bond yields were higher (+5 to 10bps) across the curve while Corporate HY credit margins remain below 300bps.

- Investors’ attention will be focused on 6 major US stocks releasing their Q1 earnings : Alphabet, Microsoft, Meta, Apple, Amazon and Eli Lilly, together with a series of 5 Central Banks rate decisions this coming week (Bank of Japan, Bank of Canada, the FED/FOMC, the ECB and the Bank of England/MPC). Note that Palantir, AMD, ARM Holdings, Novo Nordisk, will release their earnings the following week.

MARKETS

Equities

Q1 earnings weekly performances :

Tesla (-6%) Intel (+20%) Amex (-5%)

Rio Tinto (-1%) L’Oreal (+7%) Roche (+1%) Nestlé (+7%)

NB weekly : STMicro (+16%) RWE (+7%) Siemens Energy (+9%)

Biomerieux (-22%) EssilorLuxottica (-14%) Lululemon (-14%)

Bank analysts : STMicro (BNPP ‘o/w’ target €47) Saint Gobain (Barclays ‘o/w’ target €105) Siemens Energy (BofA ‘buy’ target €250) SGS (Citi ‘buy’ target ₣103) Galderma (Citi ‘buy’ target ₣185) ASM International (Citi ‘buy’ target €1000) Eiffage (MS ‘o/w’ target €186)

Rates

US curve steepening (2-10 years) stable at +52bps (-2bps)

HY corp. spreads lower : US at +285bps (stable) EU at +285bps (-10bps)

Commodities

Oil price WTI much higher (+13% vs -13% previous week) Asia’s oil buffer is shrinking, Russian crude in floating has fallen below 5m barrels (-75% since Feb) Hormuz Strait blockade contributed to a 10% global supply contraction

Gold price lower (-2.5%) impacted by higher US Bond yields

Crypto

BTC (+1.5%) ETH (+3%) SOL (+3.5%) XRP (+3.5%) Note MS and Amundi have both issued their own BTC ETF/ETP.

US

March PPI +4% vs +4.6% expected (Core at 3.8%)

Under the watch

UN warned Hormuz Strait disruption threatens 30% of global fertilizer trade at moment for spring planting

Nota Bene

USD global trade’s representation (90% in global FX trades, 60% in Foreign Debt issuances, 55% in currency Reserves, 55% in export Financing, 50% in FX Interbank deals)

Staff cuts for AI spending (Meta and Microsoft have both announced to cut thousands of staff as they spend billions of dollars in the battle to stay ahead in the AI race)

CALENDAR

Earnings: US Alphabet, Microsoft, Meta, Qualcomm, Amazon (29) Eli Lilly, Apple (30) Exxon (1st May)

EU Air Liquide (28) AstraZeneca, Total, GSK (29) Schneider Elec, UBS (30)

CB meetings : BOJ (28 April) BOC, FOMC/FED (29) ECB, BOE (30)

WHAT ANALYSTS SAY

Indosuez Wealth Management, 24 April 2026

Author : Arthur Homo, Fixed Income Research

The recovery in the construction sector is being driven more by infrastructure, public services and renovation projects than by a generalised boom in private construction. As these projects are capital-intensive, fragmented and often carried out over a short timeframe, contractors continue to prioritise flexibility. Indeed, having weathered years of squeezed margins, few contractors are prepared to commit capital to major equipment purchases at the start of a cycle, particularly as they face stricter environmental standards and uncertainties regarding the residual values of these assets. Leasing therefore remains the preferred solution.

This structural shift is unlikely to be reversed because it is being driven by regulation, sustainability requirements and the increasing complexity of equipment. Furthermore, Europe offers significant growth potential for the equipment rental industry. According to the European Rental Association (ERA), the rental penetration rate (the proportion of equipment demand met by rental rather than purchase) has risen steadily over the last ten years and stands at around 35–40%, whereas it exceeds 55% in the United States.

This year, the equipment rental market is expected to reach €34bn (ERA data for 17 European countries). Although growth projections vary considerably across markets (from +0.9% for France to +5.5% for Spain), the ERA forecasts total growth of +2.3% by 2026.

The likely increase in the penetration rate of vehicle hire will inevitably have significant financial implications for hire companies. Indeed, increased demand inevitably means investment in equipment. As the use of such equipment grows, rental companies must expand and modernise their fleets, and in particular acquire low-emission vehicles. Consequently, their capital expenditure, which has been limited over the past two years, will start to rise again.

This is expected to result in rising gross debt (after stabilising during the recession), a temporary reduction in cash flow (used to finance growth) and debt ratios that could become problematic if growth falls short of expectations or if equipment utilisation rates rise too slowly.

However, unlike in the previous cycle, the leasing sector is entering this recovery phase with two major strengths: greater pricing discipline and more robust structures. That said, the expansion of equipment fleets cannot be ignored, as it tends to focus all attention on debt ratios.

In Europe, the recovery in the construction sector clearly favours equipment hire over purchase. Demand dynamics, regulation and contractor behaviour all point to an increase in the penetration rate of rental. However, nothing comes for free: growth means capital requirements, and debt levels will return to the forefront of concerns as equipment fleets expand.The winners will be operators who can strike a balance between growth and discipline by investing selectively, maintaining an appropriate utilisation rate and preserving balance sheet flexibility.

For bond investors, the equipment rental segment remains an attractive way to gain exposure to the construction recovery, provided that debt levels are managed with care. If conditions are right, we can expect one or two major players in the rental sector to tap the euro bond market in the coming months for refinancing purposes. This could present attractive entry points.

Carmignac, 21 April 2026

Author : Kevin Thozet, Investment Committee Member

After six weeks of conflict in the Middle East, the trajectory of the equity markets may come as a surprise. Following a brief dip, stock indices have recouped most of their losses and, in the case of Iran, have even surpassed their pre-war levels. Should this be seen as a sign of complacent optimism or the result of a clear-eyed assessment of corporate fundamentals? An examination of the drivers of performance for the major global indices sheds light on this apparent paradox.

Valuation multiples have not underpinned the markets: they have contracted overall. Dividends, for their part, have played only a marginal role. It is therefore the earnings effect – the earnings momentum – that explains the market rebound. Since the start of the Iran conflict, earnings growth forecasts for 2026 have been raised by more than 4%, bringing them to around +20% for the year for the global equity index!This factor explains the resilience of the markets despite the uncertainties. These positive earnings expectations contrast with a more constrained environment: tighter financial conditions, rising interest rates linked to higher inflation, slowing economic activity, and pressure on costs and margins that are already close to their peaks.

The markets have got it right: it is the energy sector’s profits that have been significantly revised upwards, by more than 35%, driven by the rebound in oil and gas prices. These alone account for the bulk of the upward revisions to EPS – and even more than the total in Europe or Japan. The materials sector is following a similar pattern. Technology, particularly in the US, is also seeing its outlook continue to be revised upwards; profits in this sector are now expected to rise by 15% this year, which is 6 percentage points higher than at the end of February.

Companies in the sector are reaping the full benefits of the AI investment cycle, but has the rise in energy prices been fully factored in?

Conversely, expectations for the consumer and industrial sectors have been revised downwards. Rising prices at the pump act as a tax on households and weigh on corporate margins. But these downward revisions have been relatively muted. At this stage, the energy shock is seen as powerful enough to boost the sector’s profits, yet not enough to derail the rest of the economic machine, which reflects a certain degree of optimism.

This is the tipping point.

The market downturn scenario involves a significant negative supply shock to growth, caused by disruptions linked to the closure of a shipping route through which 10–15% of global maritime trade passes, coupled with the spread of rising oil prices throughout the price chain. This is the stagflation scenario.

Conversely, the bullish scenario would be based on valuations returning to their pre-war (optimistic) levels (i.e. 17x to 20x earnings over the next 12 months) in the wake of a swift resolution to the crisis and a less pronounced monetary tightening than anticipated due to delayed negative effects on growth. Assuming earnings expectations remain unchanged, this would offer further upside potential of around 10% for equity markets.

Wisdom Tree, 23 April 2026

Authors : Mobeen Tahir, Director-Research

Countries that had moved away from nuclear power are now returning to it. Sweden currently operates 6 reactors, producing around 30% of its electricity, but it has closed 7 and has none under construction. Its decision in 2023 to replace a ‘100% renewable’ target with ‘100% fossil-free’ by 2040 marks a clear change of course, paving the way for new nuclear capacity. Sweden holds 27% of Europe’s known uranium reserves. This makes the commercial implications significant, not only at the national level but also for the wider uranium market. With demand set to outstrip supply, rising prices could encourage an intensification of mining activities. Sweden is not an isolated case.

As energy demand rises, particularly due to electricity-intensive industries such as AI, nuclear power is increasingly seen as a reliable source of baseload energy, capable of providing continuous, emission-free electricity on a large scale. At the same time, geopolitical tensions, notably the war in Iran, have reinforced the need to reduce dependence on fossil fuels.

Energy security is now just as important as sustainability.

Markets began to pay closer attention to this theme as early as 2024, when hyperscalers started signing major nuclear agreements to power their data centres. But momentum accelerated in May 2025, when Trump announced executive orders aimed at quadrupling US nuclear capacity by 2050. Expanding capacity on this scale over 25 years was not something the markets could ignore. The plan includes building new reactors, extending the lifespan of existing facilities, improving regulation and investing in technologies such as small modular reactors. New reactors have come online, and landmark initiatives, such as Microsoft’s agreement to reopen Three Mile Island, have become symbols of the nuclear renaissance. As investment in AI-related infrastructure grows, nuclear energy is increasingly linked to this broader trend.

At the same time, China is making steady progress. Over the past 15 years, whilst others were reducing their capacity, China has significantly expanded its own. It now operates 61 reactors, has 38 under construction. Its approach has been industrial. Standardised designs, domestic supply chains and economies of scale have enabled faster and more cost-effective deployment.

Other countries are also getting involved. Many Asian economies, heavily reliant on fossil fuel imports, see nuclear power as a means of improving their energy security. Japan’s return to nuclear power is particularly notable. After Fukushima, the country had moved away from nuclear power, but it is now restarting its reactors and aims for at least 20% of its electricity to come from nuclear sources by 2030.

Investors often wonder whether, following a strong 2025, the opportunity is not already priced in. We believe it is not. The ambition to triple global capacity, or quadruple it in the US, is far from being reflected in the current pipeline. This will need to expand considerably, which brings with it uncertainties as to which companies will benefit.

What is clearer is that growth on this scale creates opportunities throughout the value chain, from uranium producers to service providers and technology developers. The case for nuclear power continues to strengthen, supported by public policy and rising demand.

Equities

Q1 earnings weekly performances :

Tesla (-6%) Intel (+20%) Amex (-5%)

Rio Tinto (-1%) L’Oreal (+7%) Roche (+1%) Nestlé (+7%)

NB weekly : STMicro (+16%) RWE (+7%) Siemens Energy (+9%)

Biomerieux (-22%) EssilorLuxottica (-14%) Lululemon (-14%)

Bank analysts : STMicro (BNPP ‘o/w’ target €47) Saint Gobain (Barclays ‘o/w’ target €105) Siemens Energy (BofA ‘buy’ target €250) SGS (Citi ‘buy’ target ₣103) Galderma (Citi ‘buy’ target ₣185) ASM International (Citi ‘buy’ target €1000) Eiffage (MS ‘o/w’ target €186)

Rates

US curve steepening (2-10 years) stable at +52bps (-2bps)

HY corp. spreads lower : US at +285bps (stable) EU at +285bps (-10bps)

Commodities

Oil price WTI much higher (+13% vs -13% previous week) Asia’s oil buffer is shrinking, Russian crude in floating has fallen below 5m barrels (-75% since Feb) Hormuz Strait blockade contributed to a 10% global supply contraction

Gold price lower (-2.5%) impacted by higher US Bond yields

Crypto

BTC (+1.5%) ETH (+3%) SOL (+3.5%) XRP (+3.5%) Note MS and Amundi have both issued their own BTC ETF/ETP.

US

March PPI +4% vs +4.6% expected (Core at 3.8%)

Under the watch

UN warned Hormuz Strait disruption threatens 30% of global fertilizer trade at moment for spring planting

Nota Bene

USD global trade’s representation (90% in global FX trades, 60% in Foreign Debt issuances, 55% in currency Reserves, 55% in export Financing, 50% in FX Interbank deals)

Staff cuts for AI spending (Meta and Microsoft have both announced to cut thousands of staff as they spend billions of dollars in the battle to stay ahead in the AI race)

CALENDAR

Earnings: US Alphabet, Microsoft, Meta, Qualcomm, Amazon (29) Eli Lilly, Apple (30) Exxon (1st May)

EU Air Liquide (28) AstraZeneca, Total, GSK (29) Schneider Elec, UBS (30)

CB meetings : BOJ (28 April) BOC, FOMC/FED (29) ECB, BOE (30)

WHAT ANALYSTS SAY

- Indosuez: Construction recovery, good news for equipment rental and for Bond investors

- Carmignac: Markets are holding up, primarily down to an optimistic earnings growth outlook

- Wisdom Tree: Nuclear energy, ambition to triple or quadruple the global capacity is not reflected in the current pipeline

Indosuez Wealth Management, 24 April 2026

Author : Arthur Homo, Fixed Income Research

The recovery in the construction sector is being driven more by infrastructure, public services and renovation projects than by a generalised boom in private construction. As these projects are capital-intensive, fragmented and often carried out over a short timeframe, contractors continue to prioritise flexibility. Indeed, having weathered years of squeezed margins, few contractors are prepared to commit capital to major equipment purchases at the start of a cycle, particularly as they face stricter environmental standards and uncertainties regarding the residual values of these assets. Leasing therefore remains the preferred solution.

This structural shift is unlikely to be reversed because it is being driven by regulation, sustainability requirements and the increasing complexity of equipment. Furthermore, Europe offers significant growth potential for the equipment rental industry. According to the European Rental Association (ERA), the rental penetration rate (the proportion of equipment demand met by rental rather than purchase) has risen steadily over the last ten years and stands at around 35–40%, whereas it exceeds 55% in the United States.

This year, the equipment rental market is expected to reach €34bn (ERA data for 17 European countries). Although growth projections vary considerably across markets (from +0.9% for France to +5.5% for Spain), the ERA forecasts total growth of +2.3% by 2026.

The likely increase in the penetration rate of vehicle hire will inevitably have significant financial implications for hire companies. Indeed, increased demand inevitably means investment in equipment. As the use of such equipment grows, rental companies must expand and modernise their fleets, and in particular acquire low-emission vehicles. Consequently, their capital expenditure, which has been limited over the past two years, will start to rise again.

This is expected to result in rising gross debt (after stabilising during the recession), a temporary reduction in cash flow (used to finance growth) and debt ratios that could become problematic if growth falls short of expectations or if equipment utilisation rates rise too slowly.

However, unlike in the previous cycle, the leasing sector is entering this recovery phase with two major strengths: greater pricing discipline and more robust structures. That said, the expansion of equipment fleets cannot be ignored, as it tends to focus all attention on debt ratios.

In Europe, the recovery in the construction sector clearly favours equipment hire over purchase. Demand dynamics, regulation and contractor behaviour all point to an increase in the penetration rate of rental. However, nothing comes for free: growth means capital requirements, and debt levels will return to the forefront of concerns as equipment fleets expand.The winners will be operators who can strike a balance between growth and discipline by investing selectively, maintaining an appropriate utilisation rate and preserving balance sheet flexibility.

For bond investors, the equipment rental segment remains an attractive way to gain exposure to the construction recovery, provided that debt levels are managed with care. If conditions are right, we can expect one or two major players in the rental sector to tap the euro bond market in the coming months for refinancing purposes. This could present attractive entry points.

Carmignac, 21 April 2026

Author : Kevin Thozet, Investment Committee Member

After six weeks of conflict in the Middle East, the trajectory of the equity markets may come as a surprise. Following a brief dip, stock indices have recouped most of their losses and, in the case of Iran, have even surpassed their pre-war levels. Should this be seen as a sign of complacent optimism or the result of a clear-eyed assessment of corporate fundamentals? An examination of the drivers of performance for the major global indices sheds light on this apparent paradox.

Valuation multiples have not underpinned the markets: they have contracted overall. Dividends, for their part, have played only a marginal role. It is therefore the earnings effect – the earnings momentum – that explains the market rebound. Since the start of the Iran conflict, earnings growth forecasts for 2026 have been raised by more than 4%, bringing them to around +20% for the year for the global equity index!This factor explains the resilience of the markets despite the uncertainties. These positive earnings expectations contrast with a more constrained environment: tighter financial conditions, rising interest rates linked to higher inflation, slowing economic activity, and pressure on costs and margins that are already close to their peaks.

The markets have got it right: it is the energy sector’s profits that have been significantly revised upwards, by more than 35%, driven by the rebound in oil and gas prices. These alone account for the bulk of the upward revisions to EPS – and even more than the total in Europe or Japan. The materials sector is following a similar pattern. Technology, particularly in the US, is also seeing its outlook continue to be revised upwards; profits in this sector are now expected to rise by 15% this year, which is 6 percentage points higher than at the end of February.

Companies in the sector are reaping the full benefits of the AI investment cycle, but has the rise in energy prices been fully factored in?

Conversely, expectations for the consumer and industrial sectors have been revised downwards. Rising prices at the pump act as a tax on households and weigh on corporate margins. But these downward revisions have been relatively muted. At this stage, the energy shock is seen as powerful enough to boost the sector’s profits, yet not enough to derail the rest of the economic machine, which reflects a certain degree of optimism.

This is the tipping point.

The market downturn scenario involves a significant negative supply shock to growth, caused by disruptions linked to the closure of a shipping route through which 10–15% of global maritime trade passes, coupled with the spread of rising oil prices throughout the price chain. This is the stagflation scenario.

Conversely, the bullish scenario would be based on valuations returning to their pre-war (optimistic) levels (i.e. 17x to 20x earnings over the next 12 months) in the wake of a swift resolution to the crisis and a less pronounced monetary tightening than anticipated due to delayed negative effects on growth. Assuming earnings expectations remain unchanged, this would offer further upside potential of around 10% for equity markets.

Wisdom Tree, 23 April 2026

Authors : Mobeen Tahir, Director-Research

Countries that had moved away from nuclear power are now returning to it. Sweden currently operates 6 reactors, producing around 30% of its electricity, but it has closed 7 and has none under construction. Its decision in 2023 to replace a ‘100% renewable’ target with ‘100% fossil-free’ by 2040 marks a clear change of course, paving the way for new nuclear capacity. Sweden holds 27% of Europe’s known uranium reserves. This makes the commercial implications significant, not only at the national level but also for the wider uranium market. With demand set to outstrip supply, rising prices could encourage an intensification of mining activities. Sweden is not an isolated case.

As energy demand rises, particularly due to electricity-intensive industries such as AI, nuclear power is increasingly seen as a reliable source of baseload energy, capable of providing continuous, emission-free electricity on a large scale. At the same time, geopolitical tensions, notably the war in Iran, have reinforced the need to reduce dependence on fossil fuels.

Energy security is now just as important as sustainability.

Markets began to pay closer attention to this theme as early as 2024, when hyperscalers started signing major nuclear agreements to power their data centres. But momentum accelerated in May 2025, when Trump announced executive orders aimed at quadrupling US nuclear capacity by 2050. Expanding capacity on this scale over 25 years was not something the markets could ignore. The plan includes building new reactors, extending the lifespan of existing facilities, improving regulation and investing in technologies such as small modular reactors. New reactors have come online, and landmark initiatives, such as Microsoft’s agreement to reopen Three Mile Island, have become symbols of the nuclear renaissance. As investment in AI-related infrastructure grows, nuclear energy is increasingly linked to this broader trend.

At the same time, China is making steady progress. Over the past 15 years, whilst others were reducing their capacity, China has significantly expanded its own. It now operates 61 reactors, has 38 under construction. Its approach has been industrial. Standardised designs, domestic supply chains and economies of scale have enabled faster and more cost-effective deployment.

Other countries are also getting involved. Many Asian economies, heavily reliant on fossil fuel imports, see nuclear power as a means of improving their energy security. Japan’s return to nuclear power is particularly notable. After Fukushima, the country had moved away from nuclear power, but it is now restarting its reactors and aims for at least 20% of its electricity to come from nuclear sources by 2030.

Investors often wonder whether, following a strong 2025, the opportunity is not already priced in. We believe it is not. The ambition to triple global capacity, or quadruple it in the US, is far from being reflected in the current pipeline. This will need to expand considerably, which brings with it uncertainties as to which companies will benefit.

What is clearer is that growth on this scale creates opportunities throughout the value chain, from uranium producers to service providers and technology developers. The case for nuclear power continues to strengthen, supported by public policy and rising demand.

Contacts

8 Kievyan Street, Yerevan, Armenia

+374 10 712 259

+374 43 004 182

unibankinvest@unibank.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.