Last week: Stocks lower, higher Yields & credit Spreads, lower USD & Gold - CB rates on hold - TTF Gas much higher

WEEKLY TRENDS

WEEKLY TRENDS

- Before the next earnings releases of major US capitalisations, investors and the market should have focused on Central Banks rate decisions together with macro figures releases, instead given the war with Iran and its consequences in the Hormuz strait, fears of inflation with a prolonged strait closure, meant that stocks got hammered last week across the board and rates were higher with credit spreads too

- Stock indices volatility (VIX) is at a high of 35% (like in 2022) through hedging demand (options). Technically, US indices have been trading below their 200DMAs since Thursday

- Central Banks are readjusting their reserves, Gold is consequently impacted and so is crude oil, especially the UK Brent keeping well north of $100 a barrel (US WTI was somewhat stable last week).

- Oil and gas production facilities in Qatar, in Saudi Arabia and in UAE, have been hit last week, with full capacity to be restored after a few years only

- We had a series of CB meetings last week, despite rates being kept unchanged, all meetings pointed towards higher rates and no more rate cuts this year

MARKETS

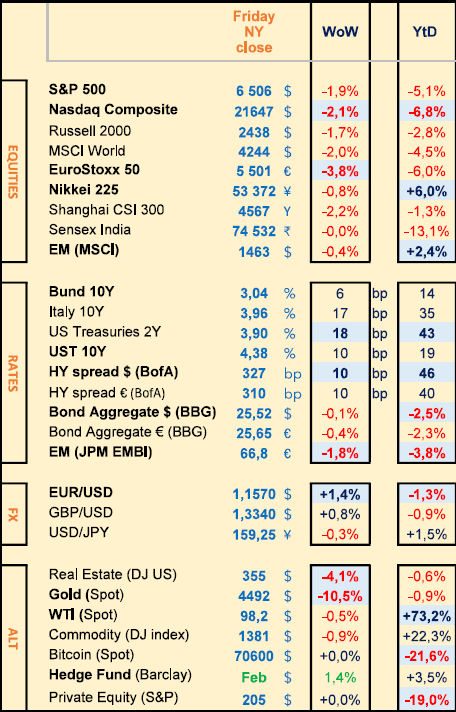

Equities

Q4 earnings weekly performances:

Atlas Copco (-7%), Vinci (-4%), Enel (-5%)

NB weekly: TotalEnergies (+6%), Hermès (-11%), Safran (-7%)

Bank analysts: Neste (Barclays ‘o/w’ target €32), Roche (HSBC ‘buy’ target ₣365), Total (Barclays ‘o/w’ target €94), Vinci (Barx ‘o/w’ target €160), Heidelberg Mat (MS ‘o/w’ target €219), Infineon (JPM ‘o/w’ target €48)

Rates

US curve steepening (2-10 years) lower at +48bps (-8bps)

HY corp. spreads higher : US at +325bps (+10) ; EU at +310bps (+10)

Commodities

Oil price WTI (-0.5%), Brent (+8%) Hormuz strait mostly closed, Qatar gas plant hit - UAE, Irak, Saudi Arabia, all reduced their oil production

Gold price much lower (-10%), Silver (-14%), Copper (-7%), while US Nat Gas (+3%), TTF Gas (+18%) and Aluminium (-6%)

Central Banks

RBA (+25bps), BOC (0), FED (0), BOE (0), ECB (0), SNB (0)

US

Feb PPI at +3.4% YoY (Core +3.5%) monthly reading at highest since July

Crypto

BTC (flat) ETH (-2%), SOL (-3.5%), XRP (-1%)

Under the watch

Share BuyBacks - blackout period (18 March until the end of April)

Large PE firms are also large Private Credit firms (Blackstone AuM PE $400bn vs PC $400bn, Apollo $150bn vs $700bn, KKR $200bn vs $300bn)

Nota Bene

Donald Trump threatened Iran on Saturday with new infrastructure hits should the Hormuz strait not be reopened within 48 hours

Ras Laffan Qatar LNG hit infrastructure, cut by 17%, with repairs taking 3 to 5 years (removing 30Mt from supply) hitting Asia mostly

CALENDAR

Earnings releases:

EU - not much until 31st March (Hermès)

Macro releases:

US - not much until 3rd April (NFP job report)

WHAT ANALYSTS SAY

PIMCO, 20 March 2026

Author: Konstantin Veit, Portfolio Manager - Tiffany Wilding, Economist

Whilst the ECB left its key interest rates unchanged, it adopted a more hawkish tone in light of recent developments in the Middle East.

The ECB now expects inflation to be well above its target in the short term, before gradually returning to 2% over the course of next year.

Whilst President Christine Lagarde highlighted the differences compared with 2022, she also reaffirmed that the ECB would do whatever is necessary to ensure price stability in the medium term.

We believe it is still too early to form a firm view on the monetary policy response, as the intensity and duration of the disruptions remain uncertain. The ECB will pay particular attention to the spillover effects on core inflation and will monitor inflation expectations very closely.

At this stage, we mainly anticipate a hawkish shift in rhetoric, but believe that the threshold for the ECB to overlook inflation temporarily exceeding its target is now higher than it was before 2022. The initial conditions, a reaction function less dependent on a central scenario and a reduced reliance on macroeconomic models could argue for a more agile ECB. Should the ECB act later in the year, we do not, at this stage, anticipate a tightening greater than what is currently priced in by the markets.

Overall, the Fed has reaffirmed its patience regarding the timing of future rate cuts.

The US Federal Reserve kept its key interest rates unchanged in March, within a range of 3.5% to 3.75%, a widely anticipated decision against a particularly complex macroeconomic backdrop.

The slight upward revisions to short-term inflation projections suggest that Fed officials view the recent energy supply shock as largely transitory, rather than a driver of sustained inflation.

Overall, the Fed reaffirmed its patience regarding the timing of future rate cuts. The median path continues to point to eventual easing, but officials appear to favour waiting for greater clarity on the persistence of the oil shock. This caution reflects the uncertainties surrounding the conflict in Iran and the risks weighing on global energy supplies, as well as questions regarding the sustained pass-through of rising oil prices to wages and inflation expectations in the United States.

Given the risks weighing on both aspects of the dual mandate, the Fed’s new projections and its communication, we continue to anticipate a monetary status quo for most of 2026, before a gradual resumption of the easing cycle towards a neutral rate of just over 3%.

ING, 20 March 2026

Author: Fabienne Jaggy Moriggi, Structured Finance

Brent crude has surpassed $100 a barrel for the first time since 2022 and commodity markets are showing increasing fragility, successive geopolitical shocks, the global economic slowdown and the restructuring of trade flows are driving a lasting transformation of the markets. At the heart of these changes, three key dynamics dominate.

The first concerns geopolitical fragmentation. Sino-American rivalry, tensions in the Middle East and Ukraine, and the emergence of autonomous economic blocs are disrupting traditional supply routes. Market players are adapting to a multitude of regulations, sanctions and logistical constraints. Energy trade is being reshaped, regional trade-offs are once again becoming essential and are reinforcing the strategic importance of access to resources. This fragility became a reality in late February 2026, when US-Israeli strikes on Iran’s nuclear and energy infrastructure triggered a series of retaliatory measures, leading to the de facto closure of the Strait of Hormuz. This strategic corridor, through which around 20% of global oil consumption and a significant proportion of LNG passes, had never before been physically blocked. Brent crude reached $119.50, its highest level since 2022. In response, the IEA decided to release 400m barrels from global strategic reserves. In this context, banks play a vital role in supporting their clients with risk management and the financing of alternative supply chains.

The second factor is macroeconomic. Following a period of inflation and monetary tightening, global growth remains mixed. Demand for raw materials is positive but uneven: strong in the energy transition sector, but weaker in heavy industry. Rising oil prices are weighing on importing countries such as China, India, Japan and South Korea, which account for around 75% of oil exports and 59% of LNG exports passing through the Strait of Hormuz, exacerbating inflationary pressures and the economic slowdown.

The third dynamic concerns the structural transformation of markets. Needs related to decarbonisation, strategic metals, LNG and biofuels coexist with persistent demand for hydrocarbons. This ambivalence creates trading opportunities but heightens the demands on risk management, capital management and data. Resilient companies now view risk as a strategic resource. The current crisis highlights the reality of global energy security. Historically, coordinated releases of stocks have been used: 1991 (Gulf War), 2005 (Hurricane Katrina), 2011 (Libyan civil war), 2022 (invasion of Ukraine). In this context, the aim was to mitigate a potential loss of supply, not a physical closure of a major strait. The use of reserves reflects the severity of current tensions.

Commodities lie at the heart of a global system where volatility, geopolitical tensions and the energy transition intersect. The resilience of stakeholders will depend on their ability to navigate an environment where stability is no longer the norm, to secure their supplies and to fully integrate geo-energy risks into their strategic decisions. The Strait of Hormuz crisis is the first in history to involve a physical blockade of a major energy corridor. It invalidates crisis management models calibrated to historical precedents and forces organisations to reassess their fundamental assumptions regarding supply resilience. This shift marks a turning point: raw materials are no longer merely at the heart of economic trade, but also of geopolitical power dynamics.

Goldman Sachs, 21 March 2026

Authors: Oil Analyst

Our short-term views are :

1) Oil prices will likely continue to trend higher while Hormuz flows remain very low

2) Brent is likely to exceed its 2008 all time high if depressed flows keep the market focused on the risk of lengthier disruptions

3) Any rise in market perceived risks of US export restrictions is likely to widen the Brent-WTI gap further

Risks to long-term prices. Oil supply could be low for longer if production potential is damaged but higher if OPEC deploys spare capacity after reopening. Apparent demand could be higher on strategic stockpiling but weaker on demand destruction.

Risk 1 - price upside - low Oil output for longer

Looking at the 5 prior largest supply shocks of the past 50 years, we estimate an average hit to production of 42% after 4 years, often due to infrastructure damage and low investment. Iran and the 7 other Persian Gulf countries produced respectively 3.5m barrels/day and 2.1m b/day of crude in 2025 (together 30% of global crude).

Risk 2 - limit upside - OPEC stabilisation

OPEC could deploy substantial spare capacity after the Strait reopens to help stabilise tight markets

Risk 3 - price upside - higher strategic stockpiling

The Hormuz shock and lingering uncertainty may cause faster strategic stock building from 2027 because end-2026 reserves will likely be low and because countries may raise SPR targets

Risk 4 - price upside - slower demand growth

High prices may slow demand by accelerating fuel efficiency gains and shifts in other fuels and by slowing GDP

Net upside price risk

Our scenario analysis suggests that the risks to oil prices remain net skewed to the upside both in the near-term and in 2027. The persistence of several prior large supply shocks underscores the risk that oil prices may stay above $100 for longer in risk scenarios with lengthier disruptions and large persistent supply losses.

Equities

Q4 earnings weekly performances:

Atlas Copco (-7%), Vinci (-4%), Enel (-5%)

NB weekly: TotalEnergies (+6%), Hermès (-11%), Safran (-7%)

Bank analysts: Neste (Barclays ‘o/w’ target €32), Roche (HSBC ‘buy’ target ₣365), Total (Barclays ‘o/w’ target €94), Vinci (Barx ‘o/w’ target €160), Heidelberg Mat (MS ‘o/w’ target €219), Infineon (JPM ‘o/w’ target €48)

Rates

US curve steepening (2-10 years) lower at +48bps (-8bps)

HY corp. spreads higher : US at +325bps (+10) ; EU at +310bps (+10)

Commodities

Oil price WTI (-0.5%), Brent (+8%) Hormuz strait mostly closed, Qatar gas plant hit - UAE, Irak, Saudi Arabia, all reduced their oil production

Gold price much lower (-10%), Silver (-14%), Copper (-7%), while US Nat Gas (+3%), TTF Gas (+18%) and Aluminium (-6%)

Central Banks

RBA (+25bps), BOC (0), FED (0), BOE (0), ECB (0), SNB (0)

US

Feb PPI at +3.4% YoY (Core +3.5%) monthly reading at highest since July

Crypto

BTC (flat) ETH (-2%), SOL (-3.5%), XRP (-1%)

Under the watch

Share BuyBacks - blackout period (18 March until the end of April)

Large PE firms are also large Private Credit firms (Blackstone AuM PE $400bn vs PC $400bn, Apollo $150bn vs $700bn, KKR $200bn vs $300bn)

Nota Bene

Donald Trump threatened Iran on Saturday with new infrastructure hits should the Hormuz strait not be reopened within 48 hours

Ras Laffan Qatar LNG hit infrastructure, cut by 17%, with repairs taking 3 to 5 years (removing 30Mt from supply) hitting Asia mostly

CALENDAR

Earnings releases:

EU - not much until 31st March (Hermès)

Macro releases:

US - not much until 3rd April (NFP job report)

WHAT ANALYSTS SAY

- PIMCO: The ECB, a turning point in communication - caution was in order at the FED's March meeting

- ING: Raw materials and geopolitical tensions

- Goldman Sachs: Oil analysis, higher prices for longer?

PIMCO, 20 March 2026

Author: Konstantin Veit, Portfolio Manager - Tiffany Wilding, Economist

Whilst the ECB left its key interest rates unchanged, it adopted a more hawkish tone in light of recent developments in the Middle East.

The ECB now expects inflation to be well above its target in the short term, before gradually returning to 2% over the course of next year.

Whilst President Christine Lagarde highlighted the differences compared with 2022, she also reaffirmed that the ECB would do whatever is necessary to ensure price stability in the medium term.

We believe it is still too early to form a firm view on the monetary policy response, as the intensity and duration of the disruptions remain uncertain. The ECB will pay particular attention to the spillover effects on core inflation and will monitor inflation expectations very closely.

At this stage, we mainly anticipate a hawkish shift in rhetoric, but believe that the threshold for the ECB to overlook inflation temporarily exceeding its target is now higher than it was before 2022. The initial conditions, a reaction function less dependent on a central scenario and a reduced reliance on macroeconomic models could argue for a more agile ECB. Should the ECB act later in the year, we do not, at this stage, anticipate a tightening greater than what is currently priced in by the markets.

Overall, the Fed has reaffirmed its patience regarding the timing of future rate cuts.

The US Federal Reserve kept its key interest rates unchanged in March, within a range of 3.5% to 3.75%, a widely anticipated decision against a particularly complex macroeconomic backdrop.

The slight upward revisions to short-term inflation projections suggest that Fed officials view the recent energy supply shock as largely transitory, rather than a driver of sustained inflation.

Overall, the Fed reaffirmed its patience regarding the timing of future rate cuts. The median path continues to point to eventual easing, but officials appear to favour waiting for greater clarity on the persistence of the oil shock. This caution reflects the uncertainties surrounding the conflict in Iran and the risks weighing on global energy supplies, as well as questions regarding the sustained pass-through of rising oil prices to wages and inflation expectations in the United States.

Given the risks weighing on both aspects of the dual mandate, the Fed’s new projections and its communication, we continue to anticipate a monetary status quo for most of 2026, before a gradual resumption of the easing cycle towards a neutral rate of just over 3%.

ING, 20 March 2026

Author: Fabienne Jaggy Moriggi, Structured Finance

Brent crude has surpassed $100 a barrel for the first time since 2022 and commodity markets are showing increasing fragility, successive geopolitical shocks, the global economic slowdown and the restructuring of trade flows are driving a lasting transformation of the markets. At the heart of these changes, three key dynamics dominate.

The first concerns geopolitical fragmentation. Sino-American rivalry, tensions in the Middle East and Ukraine, and the emergence of autonomous economic blocs are disrupting traditional supply routes. Market players are adapting to a multitude of regulations, sanctions and logistical constraints. Energy trade is being reshaped, regional trade-offs are once again becoming essential and are reinforcing the strategic importance of access to resources. This fragility became a reality in late February 2026, when US-Israeli strikes on Iran’s nuclear and energy infrastructure triggered a series of retaliatory measures, leading to the de facto closure of the Strait of Hormuz. This strategic corridor, through which around 20% of global oil consumption and a significant proportion of LNG passes, had never before been physically blocked. Brent crude reached $119.50, its highest level since 2022. In response, the IEA decided to release 400m barrels from global strategic reserves. In this context, banks play a vital role in supporting their clients with risk management and the financing of alternative supply chains.

The second factor is macroeconomic. Following a period of inflation and monetary tightening, global growth remains mixed. Demand for raw materials is positive but uneven: strong in the energy transition sector, but weaker in heavy industry. Rising oil prices are weighing on importing countries such as China, India, Japan and South Korea, which account for around 75% of oil exports and 59% of LNG exports passing through the Strait of Hormuz, exacerbating inflationary pressures and the economic slowdown.

The third dynamic concerns the structural transformation of markets. Needs related to decarbonisation, strategic metals, LNG and biofuels coexist with persistent demand for hydrocarbons. This ambivalence creates trading opportunities but heightens the demands on risk management, capital management and data. Resilient companies now view risk as a strategic resource. The current crisis highlights the reality of global energy security. Historically, coordinated releases of stocks have been used: 1991 (Gulf War), 2005 (Hurricane Katrina), 2011 (Libyan civil war), 2022 (invasion of Ukraine). In this context, the aim was to mitigate a potential loss of supply, not a physical closure of a major strait. The use of reserves reflects the severity of current tensions.

Commodities lie at the heart of a global system where volatility, geopolitical tensions and the energy transition intersect. The resilience of stakeholders will depend on their ability to navigate an environment where stability is no longer the norm, to secure their supplies and to fully integrate geo-energy risks into their strategic decisions. The Strait of Hormuz crisis is the first in history to involve a physical blockade of a major energy corridor. It invalidates crisis management models calibrated to historical precedents and forces organisations to reassess their fundamental assumptions regarding supply resilience. This shift marks a turning point: raw materials are no longer merely at the heart of economic trade, but also of geopolitical power dynamics.

Goldman Sachs, 21 March 2026

Authors: Oil Analyst

Our short-term views are :

1) Oil prices will likely continue to trend higher while Hormuz flows remain very low

2) Brent is likely to exceed its 2008 all time high if depressed flows keep the market focused on the risk of lengthier disruptions

3) Any rise in market perceived risks of US export restrictions is likely to widen the Brent-WTI gap further

Risks to long-term prices. Oil supply could be low for longer if production potential is damaged but higher if OPEC deploys spare capacity after reopening. Apparent demand could be higher on strategic stockpiling but weaker on demand destruction.

Risk 1 - price upside - low Oil output for longer

Looking at the 5 prior largest supply shocks of the past 50 years, we estimate an average hit to production of 42% after 4 years, often due to infrastructure damage and low investment. Iran and the 7 other Persian Gulf countries produced respectively 3.5m barrels/day and 2.1m b/day of crude in 2025 (together 30% of global crude).

Risk 2 - limit upside - OPEC stabilisation

OPEC could deploy substantial spare capacity after the Strait reopens to help stabilise tight markets

Risk 3 - price upside - higher strategic stockpiling

The Hormuz shock and lingering uncertainty may cause faster strategic stock building from 2027 because end-2026 reserves will likely be low and because countries may raise SPR targets

Risk 4 - price upside - slower demand growth

High prices may slow demand by accelerating fuel efficiency gains and shifts in other fuels and by slowing GDP

Net upside price risk

Our scenario analysis suggests that the risks to oil prices remain net skewed to the upside both in the near-term and in 2027. The persistence of several prior large supply shocks underscores the risk that oil prices may stay above $100 for longer in risk scenarios with lengthier disruptions and large persistent supply losses.

Contacts

8 Kievyan Street, Yerevan, Armenia

+374 10 712 259

+374 43 004 182

unibankinvest@unibank.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.