Last week: Oracle & Broadcom disappoint; FED cut by 25bps; yield curve steepened; Gold/Silver higher while Oil is lower

WEEKLY TRENDS

WEEKLY TRENDS

- The earnings from Oracle and Broadcom disappointed the investors with the stocks ending the week at -13% and -8% respectively. Oracle presents $127bn of debts, a negative FCF (Free Cash Flow) of -$13bn supposedly becoming positive in 2028 only

- Some year-end adjustments continue to happen in stock indices (Russell is up 1.2% while Nasdaq is down 1.6%)

- For the 3rd time in a row, the FED/FOMC cut last week by 25bps as expected (9 in favour, 3 against). The Futures market is now pricing a 50% chance of a June 25bps rate cut next

- Silver was really the Hot thing last week with a surging price at $64 an ounce or +120% YTD (Gold YTD is at +64% while Copper is at +32%). Oil continues to outperform with a weekly -4.5% return, while the US yield curve continues to steepen (2yrs yield going lower coupled with the 10yrs going higher)

- M&As are back with Netflix onto Warner Brothers, Eli Lilly looking to buy Abivax and IBM buying Confluent for $11bn

- Next week we shall have rate decisions from the BoE, the BoJ and the ECB, in addition to the releases of US macro data long awaited (Nov NFP payroll and CPI inflation for Nov).

MARKETS

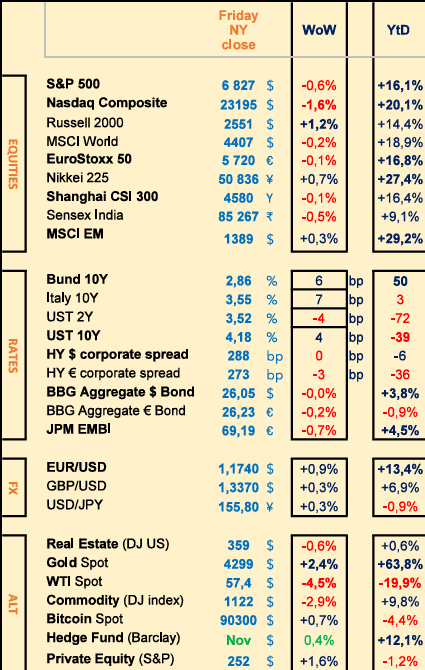

Equities

Weekly performances after earnings releases:

Oracle (-13%), Broadcom (-8%), Adobe (+2%), Synopsys (-3%)

M&A: Netflix is to buy Warner Bros ($72bn); IBM bought Confluent (+30%) for $11bn; Eli Lilly looking to buy Abivax (+15%)

Analysts: Bayer (JPM ‘o/w’ target €50), Galderma (JPM ‘o/w’ target ₣190), Engie (JPM ‘o/w’ target €24.50), Airbus (JPM ‘o/w’ target €255), ADP (MS ‘o/w’ target €140), Publicis (JPM ‘o/w’ target €130)

Rates

US curve steepening (2-10 years) higher at 66bps (+10bps)

HY corp. spreads stable with US at +290bps and EU at +275bps

Commodities

Oil price lower (-4.5%) EIA plans on a slightly lower US prod in 2026 (-0.1m b/day) while OPEC plans on a stronger demand (+1.3m b/day)

Gold price higher (+2.5%) - Silver higher at $62 (ATH)

Crypto

BTC higher (+1%) this time ended the week just above the $90k mark

US

After being closed for 43 days, the Federal Bureau of Statistics (Labor, Economic Analysis) are only beginning to catch up

Under the watch

Silver driven by collapsing Chinese inventories, tightening London liquidity, pre-emptive US tariffs, surging Indian demand, run into ETF and Options, Chinese tax on Gold pushing money into Silver

FED has started buying TBills last Friday ($40bn due in Dec) 2 weeks after QT ended

Nota Bene

Bank of America’s Chief Investment Strategist Hartnett is bullish on Commodities, he thinks that Oil & Energy stocks are the best contrarian bet for 2026

S&P500 profit margins rose to 13.5% in Q3 (ATH)

CALENDAR

Earnings releases :

US Abivax (15 Dec), Micron Tech (17), Nike, Fedex (18)

EU Vinci, ADP (16)

Macro releases:

US Nov NFP payroll (16 Dec), Nov CPI inflation (18)

Central Bank rate decisions :

ECB (17 Dec), BOE/MPC (18), BOJ (19)

WHAT ANALYSTS SAY

UBS GWM, 8 December 2025

Author: James Mazeau, Economist, Chief Investment Office

Oil prices are expected to remain strong, even if a peace agreement is reached between Ukraine and Russia.

Gold, which began to recover after its fall at the end of October, is expected to continue to rise.

Ten days ago, oil prices fell to their lowest level in a month. This drop occurred as efforts continued to negotiate a peace agreement between Russia and Ukraine, which could increase energy supplies from Russia. Investors remain on the lookout for any signs of a ceasefire.

Numerous sticking points remain in the negotiations.

Investors are watching closely for any signs of decisive progress between Ukraine and Russia. According to UBS Research, an imminent end to the conflict remains unlikely. However, even if a peace agreement is reached, oil prices are expected to remain well supported, which is in line with its broader, positive outlook for commodities heading into 2026.

Oil prices have not followed the upward trend of other commodities this year, due to weaker-than-expected demand growth and abundant supply from the Americas and OPEC+. However, despite declining demand, there is no oversupply.

The recent increase in offshore oil levels, i.e. the amount of crude currently being transported by ships, has not translated into an accumulation in onshore stocks. On the contrary, data from the International Energy Agency (IEA) indicate a decline.

With regard to market balance in the coming months, limited growth in non-OPEC+ supply and an increase in global demand are expected. As a result, Brent crude is expected to be around $67 per barrel at the end of 2026.

On the Industrial Metals side.

As for industrial metals such as copper and aluminium, prices are expected to be supported by limited supply and rising demand.

Finally, gold, which began to recover after its fall at the end of October, should continue to rise.

This is because lower US interest rates reduce the opportunity cost of holding gold, and central banks are continuing to diversify their reserves to reduce their exposure to the US dollar.

As a result, Commodities are considered attractive.

BlackRock, 8 December 2025

Authors: Jean Boivin, Head of BR Investment Institute; Wei Li, Global Chief Investment Strategist

The gap in time between capex needs and eventual revenues means AI builders have started using debt to get over a financing “hump.” This frontloading of spending is necessary to realize eventual gains. Private sector leverage will add to a heavily indebted public sector, creating financial system vulnerabilities. Bond yield spikes could pose a risk to this financing. All this creates a very different investment environment with some core features. First, higher leverage will result in greater credit issuance across public and private markets. Second, a broadly higher cost of capital as this big borrowing puts upward pressure on interest rates. Third, before new pools of AI revenues spread across the economy, further concentrated market gains within tech will require big calls. And fourth, more room for alpha and active investing as those revenues spread beyond tech. All this means traditional approaches to portfolio construction need a rethink.

AI is not only an innovation itself but has the potential to innovate the process of innovation. AI could begin to generate, test and improve new concepts on its own. If that happens, the rate of discovery could accelerate, driving scientific breakthroughs such as in materials, drugs and technology. This self reinforcing loop of accelerating innovation is key to achieving the breakout.

We stay overweight U.S. stocks and the AI theme, supported by robust earnings expectations. The capex may pay off overall even if not for individual companies. The next phase may be more about energy and resolving bottlenecks.

One risk: a structurally higher cost of capital raises the cost of AI-related investment and affects the broader economy. A more leveraged system also creates vulnerabilities to shocks such as bond yield spikes tied to fiscal concerns or policy tensions between managing inflation and debt servicing costs. Indebted governments have less capacity to cushion such shocks.

We think investors should focus less on spreading risk indiscriminately and more on owning it more deliberately – in short, a more active approach. We think high-conviction strategies.

We see opportunities emerging where constraints will likely bite the most: power systems, grids, critical minerals and potential beneficiaries from permitting reform. Private capital will be central to bridging the gap between the current supply of energy and future demand as elevated debt limits government spending, in our view.

Hefty defense spending could create medium-term opportunities in European defense tech. We see the political focus on energy as a positive driver for European utilities.

Stablecoin adoption is widening and is increasingly integrated into mainstream payment systems. Beyond banking, we see potential for adoption in cross-border payments. Additionally, in EMs, stablecoins could be used domestically as an alternative to local currency, broadening dollar access but challenging monetary control if domestic currency use declines, supporting the dollar.

We like EM hard currency debt tactically given attractive income, limited issuance and stronger sovereign balance sheets. On a long-term horizon, we favor EM equities at the cross current of mega forces, like India.

HSBC GPBW, 12 December 2025

Author: Georgios Leontaris, Chief Investment Officer, EMEA

Global spending on generative AI is expected to exceed $640 billion in 2025, with approximately 80% allocated to hardware such as semiconductors and data centre systems. Attention is currently shifting from upstream enablers, such as chip manufacturers, semiconductor equipment and hardware, to downstream software and AI users who are capitalising on the commercialisation of this technology. These include AI agents, intelligent robotics, autonomous driving systems, next-generation medicines, AI-enabled computers and smartphones. The AI ecosystem is now a global network linking North American leadership in cloud and software, European expertise in industrial software and data governance, and Asian dominance in manufacturing, automation and robotics.

In terms of applications, automation is perhaps one of the most immediate and interesting results of AI in terms of investment. Improvements in computer vision, sensory feedback and autonomous processing enable machines to independently perform multi-step tasks. Industrial robotics, logistics and precision manufacturing are benefiting from this development. China now accounts for more than half of global industrial robot installations, a share that continues to grow as domestic suppliers strengthen their capabilities.

The security sector is also experiencing rapid expansion. The convergence of AI with aerospace, satellite and cybersecurity technologies is redefining how nations and businesses protect their data, infrastructure and assets. Low-orbit satellites and micro-drones are revolutionising connectivity and surveillance, while facial recognition and biometric systems are enhancing security in both civilian and military applications.

Cybersecurity remains a high-growth segment, with global spending expected to increase at a compound annual rate of 11% through 2030, while offering long-term opportunities related to the growing need for digital resilience in a connected world. At a regional level, North American companies dominate the software and data infrastructure sector; Europe excels in industrial automation and digital regulation; and Asia leads in computer hardware manufacturing and robotics. This dispersion leads to diversification across the AI value chain, balancing political risk while capturing different phases of technological development. Energy and infrastructure appear to be secondary beneficiaries. The considerable computing needs of AI are accelerating demand for renewable and stable energy sources, stimulating investment in grid modernisation, storage and clean energy.

As adoption becomes more widespread and monetisation accelerates, the winners will likely be companies that combine technological expertise with financial discipline and are able to commercialise AI sustainably across multiple sectors and regions.

While volatility is inevitable in a rapidly evolving field, the long-term trajectory remains clear. AI is not a passing technology cycle, but a structural driver of global productivity and competitiveness, with an impact comparable to that of past industrial revolutions.

In the years ahead, seizing the growing global opportunities associated with AI adoption and monetisation will require looking beyond hardware and hype to the companies and systems that are integrating intelligence into the global economic fabric. Thus, AI is no longer a speculative frontier: it is the cornerstone of the next cycle of global growth.

Equities

Weekly performances after earnings releases:

Oracle (-13%), Broadcom (-8%), Adobe (+2%), Synopsys (-3%)

M&A: Netflix is to buy Warner Bros ($72bn); IBM bought Confluent (+30%) for $11bn; Eli Lilly looking to buy Abivax (+15%)

Analysts: Bayer (JPM ‘o/w’ target €50), Galderma (JPM ‘o/w’ target ₣190), Engie (JPM ‘o/w’ target €24.50), Airbus (JPM ‘o/w’ target €255), ADP (MS ‘o/w’ target €140), Publicis (JPM ‘o/w’ target €130)

Rates

US curve steepening (2-10 years) higher at 66bps (+10bps)

HY corp. spreads stable with US at +290bps and EU at +275bps

Commodities

Oil price lower (-4.5%) EIA plans on a slightly lower US prod in 2026 (-0.1m b/day) while OPEC plans on a stronger demand (+1.3m b/day)

Gold price higher (+2.5%) - Silver higher at $62 (ATH)

Crypto

BTC higher (+1%) this time ended the week just above the $90k mark

US

After being closed for 43 days, the Federal Bureau of Statistics (Labor, Economic Analysis) are only beginning to catch up

Under the watch

Silver driven by collapsing Chinese inventories, tightening London liquidity, pre-emptive US tariffs, surging Indian demand, run into ETF and Options, Chinese tax on Gold pushing money into Silver

FED has started buying TBills last Friday ($40bn due in Dec) 2 weeks after QT ended

Nota Bene

Bank of America’s Chief Investment Strategist Hartnett is bullish on Commodities, he thinks that Oil & Energy stocks are the best contrarian bet for 2026

S&P500 profit margins rose to 13.5% in Q3 (ATH)

CALENDAR

Earnings releases :

US Abivax (15 Dec), Micron Tech (17), Nike, Fedex (18)

EU Vinci, ADP (16)

Macro releases:

US Nov NFP payroll (16 Dec), Nov CPI inflation (18)

Central Bank rate decisions :

ECB (17 Dec), BOE/MPC (18), BOJ (19)

WHAT ANALYSTS SAY

- UBS: Positive outlook for the Commodities markets in 2026

- BlackRock: 2026 Global Outlock, pushing limits

- HSBC: the AI evolution, seizing the next wave of global productivity

UBS GWM, 8 December 2025

Author: James Mazeau, Economist, Chief Investment Office

Oil prices are expected to remain strong, even if a peace agreement is reached between Ukraine and Russia.

Gold, which began to recover after its fall at the end of October, is expected to continue to rise.

Ten days ago, oil prices fell to their lowest level in a month. This drop occurred as efforts continued to negotiate a peace agreement between Russia and Ukraine, which could increase energy supplies from Russia. Investors remain on the lookout for any signs of a ceasefire.

Numerous sticking points remain in the negotiations.

Investors are watching closely for any signs of decisive progress between Ukraine and Russia. According to UBS Research, an imminent end to the conflict remains unlikely. However, even if a peace agreement is reached, oil prices are expected to remain well supported, which is in line with its broader, positive outlook for commodities heading into 2026.

Oil prices have not followed the upward trend of other commodities this year, due to weaker-than-expected demand growth and abundant supply from the Americas and OPEC+. However, despite declining demand, there is no oversupply.

The recent increase in offshore oil levels, i.e. the amount of crude currently being transported by ships, has not translated into an accumulation in onshore stocks. On the contrary, data from the International Energy Agency (IEA) indicate a decline.

With regard to market balance in the coming months, limited growth in non-OPEC+ supply and an increase in global demand are expected. As a result, Brent crude is expected to be around $67 per barrel at the end of 2026.

On the Industrial Metals side.

As for industrial metals such as copper and aluminium, prices are expected to be supported by limited supply and rising demand.

Finally, gold, which began to recover after its fall at the end of October, should continue to rise.

This is because lower US interest rates reduce the opportunity cost of holding gold, and central banks are continuing to diversify their reserves to reduce their exposure to the US dollar.

As a result, Commodities are considered attractive.

BlackRock, 8 December 2025

Authors: Jean Boivin, Head of BR Investment Institute; Wei Li, Global Chief Investment Strategist

The gap in time between capex needs and eventual revenues means AI builders have started using debt to get over a financing “hump.” This frontloading of spending is necessary to realize eventual gains. Private sector leverage will add to a heavily indebted public sector, creating financial system vulnerabilities. Bond yield spikes could pose a risk to this financing. All this creates a very different investment environment with some core features. First, higher leverage will result in greater credit issuance across public and private markets. Second, a broadly higher cost of capital as this big borrowing puts upward pressure on interest rates. Third, before new pools of AI revenues spread across the economy, further concentrated market gains within tech will require big calls. And fourth, more room for alpha and active investing as those revenues spread beyond tech. All this means traditional approaches to portfolio construction need a rethink.

AI is not only an innovation itself but has the potential to innovate the process of innovation. AI could begin to generate, test and improve new concepts on its own. If that happens, the rate of discovery could accelerate, driving scientific breakthroughs such as in materials, drugs and technology. This self reinforcing loop of accelerating innovation is key to achieving the breakout.

We stay overweight U.S. stocks and the AI theme, supported by robust earnings expectations. The capex may pay off overall even if not for individual companies. The next phase may be more about energy and resolving bottlenecks.

One risk: a structurally higher cost of capital raises the cost of AI-related investment and affects the broader economy. A more leveraged system also creates vulnerabilities to shocks such as bond yield spikes tied to fiscal concerns or policy tensions between managing inflation and debt servicing costs. Indebted governments have less capacity to cushion such shocks.

We think investors should focus less on spreading risk indiscriminately and more on owning it more deliberately – in short, a more active approach. We think high-conviction strategies.

We see opportunities emerging where constraints will likely bite the most: power systems, grids, critical minerals and potential beneficiaries from permitting reform. Private capital will be central to bridging the gap between the current supply of energy and future demand as elevated debt limits government spending, in our view.

Hefty defense spending could create medium-term opportunities in European defense tech. We see the political focus on energy as a positive driver for European utilities.

Stablecoin adoption is widening and is increasingly integrated into mainstream payment systems. Beyond banking, we see potential for adoption in cross-border payments. Additionally, in EMs, stablecoins could be used domestically as an alternative to local currency, broadening dollar access but challenging monetary control if domestic currency use declines, supporting the dollar.

We like EM hard currency debt tactically given attractive income, limited issuance and stronger sovereign balance sheets. On a long-term horizon, we favor EM equities at the cross current of mega forces, like India.

HSBC GPBW, 12 December 2025

Author: Georgios Leontaris, Chief Investment Officer, EMEA

Global spending on generative AI is expected to exceed $640 billion in 2025, with approximately 80% allocated to hardware such as semiconductors and data centre systems. Attention is currently shifting from upstream enablers, such as chip manufacturers, semiconductor equipment and hardware, to downstream software and AI users who are capitalising on the commercialisation of this technology. These include AI agents, intelligent robotics, autonomous driving systems, next-generation medicines, AI-enabled computers and smartphones. The AI ecosystem is now a global network linking North American leadership in cloud and software, European expertise in industrial software and data governance, and Asian dominance in manufacturing, automation and robotics.

In terms of applications, automation is perhaps one of the most immediate and interesting results of AI in terms of investment. Improvements in computer vision, sensory feedback and autonomous processing enable machines to independently perform multi-step tasks. Industrial robotics, logistics and precision manufacturing are benefiting from this development. China now accounts for more than half of global industrial robot installations, a share that continues to grow as domestic suppliers strengthen their capabilities.

The security sector is also experiencing rapid expansion. The convergence of AI with aerospace, satellite and cybersecurity technologies is redefining how nations and businesses protect their data, infrastructure and assets. Low-orbit satellites and micro-drones are revolutionising connectivity and surveillance, while facial recognition and biometric systems are enhancing security in both civilian and military applications.

Cybersecurity remains a high-growth segment, with global spending expected to increase at a compound annual rate of 11% through 2030, while offering long-term opportunities related to the growing need for digital resilience in a connected world. At a regional level, North American companies dominate the software and data infrastructure sector; Europe excels in industrial automation and digital regulation; and Asia leads in computer hardware manufacturing and robotics. This dispersion leads to diversification across the AI value chain, balancing political risk while capturing different phases of technological development. Energy and infrastructure appear to be secondary beneficiaries. The considerable computing needs of AI are accelerating demand for renewable and stable energy sources, stimulating investment in grid modernisation, storage and clean energy.

As adoption becomes more widespread and monetisation accelerates, the winners will likely be companies that combine technological expertise with financial discipline and are able to commercialise AI sustainably across multiple sectors and regions.

While volatility is inevitable in a rapidly evolving field, the long-term trajectory remains clear. AI is not a passing technology cycle, but a structural driver of global productivity and competitiveness, with an impact comparable to that of past industrial revolutions.

In the years ahead, seizing the growing global opportunities associated with AI adoption and monetisation will require looking beyond hardware and hype to the companies and systems that are integrating intelligence into the global economic fabric. Thus, AI is no longer a speculative frontier: it is the cornerstone of the next cycle of global growth.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+374 43 00-43-82

Broker

broker@unibankinvest.am

research@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.