Last week: US June CPI & PPI remain well above the 2% FED’s target; strong start for US earnings; Genius Act adopted

WEEKLY TRENDS

WEEKLY TRENDS

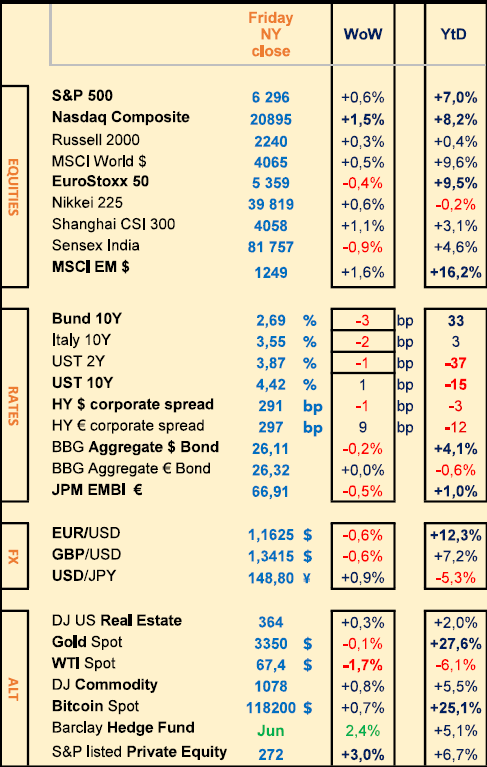

- US economy remains strong (June CPI YoY at 2.7% still above the FED’s target at 2%) while unemployment rate is at 4.1% (June figures) although the job NFP figures will most likely be revised down for the year

- FED officials, Daly and Waller, think the FED should lower its rates in July instead of September to remain in front of a slowly weakening private sector jobs market

- Yet, the Q2 earnings are off to a good start. The 6 major US banks together with some good corporate names, delivered solid results last week. 110 more S&P500 companies will report this coming week (incl. Alphabet, Tesla, IBM and Coca-Cola)

- Gold remained stable while Oil was under pressure last week, Bond yields were fairly stable and BTC hit a new ATH (US Congress adopted 3 major Acts last week, supporting the Stablecoins and the Cryptos like BTC/ETH)

- The ECB will meet on Thursday (no change expected)

MARKETS

Equities

Important weekly performances:

Circle (+19%, on us Congress adopting the Genius Act), SAAB (+14%, on strong outlook), ABB (+10%, on strong outlook), TSMC (+5%, on earnings)

JPM (+1.4%), Wells Fargo (-1.9%, poor outlook), BoNY (+2%), Citi (+8%)

Renault (-18%, on poor outlook), Elevance Health (-18%, on poor outlook)

Analysts:

Nokia (JPM ‘o/w’ target €5.6), Easyjet (JPM ‘o/w’ target £670), Experian (MS ‘o/w’ target £47), Dassault systemes (MS ‘o/w’ target €40.5)

Rates

US curve (2-10 years) steepening slightly higher at 55bps (Bond yields slightly lower across the board)

HY corporate spreads at 290/295bps (US & EU)

Commodities

Oil price lower (-1.5%) US inventories lost 3.9m barrels last week

Copper price slightly higher (+0.5%) pushed by strong US retail sales and Q2 China GDP released at 5.2% YoY (5.4% in Q1)

US

June CPI at 2.7% YoY (Core at 2.9%)

June PPI at 2.3% (Core at 2.6%) vs 2.7% prior in May

Crypto

BTC hit yet another ATH at $123k last Monday, while ETH went up by 22% last week at $3629 (ATH $4100 in 2021). All reacting to US Congress passing the Genius Act (Stablecoins) the Clarity Act (Cryptos) and the Anti-CBDC Act (CB digital currency).

Under the watch

Trump prepares executive order to open US retirement (401k) to Crypto investments (as well as Gold and Private Equity)

Nota Bene

US new trade barriers should on average hit 20% soon vs 2.5% in Jan.

CALENDAR

Upcoming earnings releases:

US Coca-Cola, Philip Morris (21 July), Alphabet, Tesla, IBM, AT&T (23)

EU SAP (22 July), LVMH, Roche, Nestlé, Total (24), Aon, VW (25)

Upcoming CB meetings :

ECB (24 July)

FOMC/FED (30 July)

BOJ (31 July)

BOE (7 Aug)

WHAT ANALYSTS SAY

VanEck, 15 July 2025

Author: Martijn Rozemuller, General Director Europe

The growing commitment of governments and major technology companies indicates that quantum computing may well be approaching a tipping point. According to McKinsey & Company, public investment now exceeds $42 billion, reflecting the strategic interest in this transformative technology. At the same time, the private sector is advancing rapidly, with more than 10,000 quantum-related patents filed in the last five years.

Economic opportunities are already being explored in several sectors. In finance, for example, quantum computing could be used to optimise investment portfolios, refine risk analysis and detect fraud – while posing a threat to current encryption standards in the longer term.

In healthcare, it offers promising prospects for drug discovery, molecular simulation and medical data analysis. A notable example is the collaboration between IBM and the Cleveland Clinic in the United States, which led to the installation of the first quantum computer dedicated to healthcare in 2023. Among its various applications, it is used to improve machine learning models for prescribing antibiotics.

To better understand the situation, it is important to note that quantum computing is currently transitioning from theoretical research to an early commercial exploration phase – a period marked by both rapid advances and major technical challenges. As part of this transition, several companies are now offering quantum computers – either by physically delivering them or by providing remote access via cloud platforms. Over the past six months, major players in the industry have announced notable hardware advances: Google unveiled its Willow chip, Microsoft unveiled its Majorana processor, and Amazon announced Ocelot, which uses ‘cat’ qubits to improve error correction. While these developments are promising, they primarily reflect hardware advances and do not yet translate into immediate commercial utility. Most current systems still operate in what is known as the NISQ (Noisy Intermediate-Scale Quantum) era – a phase where performance is impressive on an experimental level, but limited by high error rates and a lack of scalability. These systems remain largely experimental at this stage and are not yet suitable for large-scale practical applications. As a result, the current enthusiasm is based more on long-term potential than on proven performance. The gap between laboratory breakthroughs and widespread deployment remains significant – and closing it will require continuous innovation and rigorous execution. Leading companies recognise these challenges and have established clear roadmaps to address them. IBM, for example, recently updated its quantum roadmap, with the goal of delivering a fault-tolerant quantum computer by 2029 (Example).

Quantum computing may be reaching a tipping point, with the potential to spur a wave of major innovations. As an emerging technology, its development will likely be uneven, and widespread adoption is far from guaranteed.

Investors aware of its long-term potential would therefore be well advised to follow its progress closely. The next breakthrough could be closer than we think – and for those who are prepared, it could represent a unique opportunity to engage in one of the most promising technological fields of our time.

Mandarine Gestion, 16 July 2025

Author: Augustin Lecoq, Equity Fund Manager

An unexpected depth of rating

In terms of its stock market, Japan has a very rich and deep listing, with around 4,000 listed companies, and is also notable for its proportion of small businesses, which account for around two-thirds of the total. Being listed remains the Holy Grail for any Japanese entrepreneur. It is therefore easy to find companies where the interests of investors and company directors, who are often majority shareholders, are aligned. ‘Kabunushi Yutai’ also create a virtuous circle with individuals through the distribution of vouchers and gifts to shareholders.

Welcome reforms

Faced with this problem, the Tokyo Stock Exchange has implemented measures to improve the situation, asking the least valued companies to take concrete action. First through recommendations in 2023, then by increasing pressure in 2024. This represents a real upheaval in Japanese capitalism, which has long been accustomed to cross-shareholdings between customers and suppliers and the accumulation of excessive cash reserves.

Beyond valuation issues, many microcaps are turning operational challenges into opportunities in a multitude of niches :

· The ageing population is a boon for the M&A advisory sector, with executives averaging 62 years of age and 52% of them having no natural successor.

· Japan is also lagging far behind in terms of digitalisation. Although it is at the forefront of hardware, its companies are virtually absent from the international software market, offering a boulevard of growth for companies capable of attracting talent, such as SRE, I'LL, System Support, TDC, Techmatrix, Baudroie and many others, to help the country bridge this gap.

· Faced with an increase in natural disasters, Raito Kogyo is capitalising on the recognition of its landslide prevention systems, while TRE provides post-disaster waste management, as it did recently in Fukushima.

· To combat rural depopulation, S-Pool has launched supervised farms to promote the professional integration of people with disabilities. As for Lacto Japan, the leading importer of powdered milk, it is benefiting from the crisis in the dairy industry, despite rising consumption.

· Even in the face of declining birth rates, IBJ benefits from a government aid system for its marriage agency service dedicated to Japanese people wishing to marry.

These structural advantages make Japan an ideal playground for selecting small, differentiated stocks. This region represents 25% of our investment universe, on a par with the United States and Europe, and offers genuine diversification within a global equity allocation.

Carmignac, 14 July 2025

Author: Xavier Hovasse, EM equity fund manager

China's evolution and its great leap forward in AI

Ten years ago, the quality of Chinese products was criticised for being far inferior to that of American or German products. This is no longer the case today. The country is home to some of the best scientists and engineers of the new generation, trained by its excellent education system, and has significantly strengthened its industrial capabilities and skills. China is now a world leader in renewable energy, electric vehicles (EVs) and artificial intelligence (AI). It is now the world's leading exporter of cars, with BYD selling more vehicles in Europe than Tesla.

In the field of AI, two years ago it was assumed that the United States would naturally dominate. However, DeepSeek has overturned this assumption and is now positioning itself as a serious contender in the AI race. As the world's second largest economy, China has an exceptional education system focused on science and mathematics, supported by massive government investment. US measures to restrict exports of electronic chips to China have failed. Jensen Huang, CEO of Nvidia, recently warned that Chinese companies specialising in AI are now ‘formidable’. The world is now realising that China is no longer just a low-cost manufacturing hub; it can dominate global manufacturing in almost every field. Furthermore, it is the leading trading partner for almost all emerging markets.

Beyond China, Asia remains attractive

Although attention is focused on China, Asia as a whole continues to prosper. Today, 100% of Nvidia's graphics processing units (GPUs) are manufactured by Taiwanese company TSMC, and most of its memory products come from South Korean company Hynix. The artificial intelligence revolution depends on Asia.

As for India, the country is reminiscent of China 20 years ago, with an economic model resembling ‘state capitalism’. This type of economic governance is based on a long-term vision, political stability and the mantra ‘Made in India’. In our view, this will bear fruit largely thanks to tensions between the United States and China, but also thanks to a huge and predominantly English-speaking population, a high-quality education system and an industry protected by the government, the cornerstone of Prime Minister Narendra Modi's leadership during his three terms in office. The Indian economy is expected to grow by 6% to 7% per year over the next 10 to 15 years, with very well-managed companies and, unlike China, no overcapacity. Indeed, returns on investment remain high, unlike the supply-driven Chinese economy.

Latin America, the winner of Donald Trump's new policies

Some emerging countries, such as Mexico, are benefiting from trade wars thanks to their attractiveness for the ‘relocation of production chains’ from the United States. Mexican President Claudia Sheinbaum recently strengthened relations with the United States, notably by cooperating to improve security along the border. In the south, we remain optimistic about Brazil. Brazilian equities, particularly those in the utilities sector, are significantly undervalued. Among the world's largest countries, Brazil has the highest real interest rates, above 7%, making the Brazilian real particularly attractive. Finally, in Argentina, the fiscal situation has improved significantly, moving from a large deficit to a surplus under Javier Milei's leadership, and sovereign bonds have seen an impressive recovery.

China is not the only safe bet in emerging markets; it is, of course, an integral part of them, but emerging markets as a whole are full of dynamic, global companies that are leaders in all sectors. And today, with the tailwind of Donald Trump's second term, the time seems more propitious than ever to invest in this asset class.

Equities

Important weekly performances:

Circle (+19%, on us Congress adopting the Genius Act), SAAB (+14%, on strong outlook), ABB (+10%, on strong outlook), TSMC (+5%, on earnings)

JPM (+1.4%), Wells Fargo (-1.9%, poor outlook), BoNY (+2%), Citi (+8%)

Renault (-18%, on poor outlook), Elevance Health (-18%, on poor outlook)

Analysts:

Nokia (JPM ‘o/w’ target €5.6), Easyjet (JPM ‘o/w’ target £670), Experian (MS ‘o/w’ target £47), Dassault systemes (MS ‘o/w’ target €40.5)

Rates

US curve (2-10 years) steepening slightly higher at 55bps (Bond yields slightly lower across the board)

HY corporate spreads at 290/295bps (US & EU)

Commodities

Oil price lower (-1.5%) US inventories lost 3.9m barrels last week

Copper price slightly higher (+0.5%) pushed by strong US retail sales and Q2 China GDP released at 5.2% YoY (5.4% in Q1)

US

June CPI at 2.7% YoY (Core at 2.9%)

June PPI at 2.3% (Core at 2.6%) vs 2.7% prior in May

Crypto

BTC hit yet another ATH at $123k last Monday, while ETH went up by 22% last week at $3629 (ATH $4100 in 2021). All reacting to US Congress passing the Genius Act (Stablecoins) the Clarity Act (Cryptos) and the Anti-CBDC Act (CB digital currency).

Under the watch

Trump prepares executive order to open US retirement (401k) to Crypto investments (as well as Gold and Private Equity)

Nota Bene

US new trade barriers should on average hit 20% soon vs 2.5% in Jan.

CALENDAR

Upcoming earnings releases:

US Coca-Cola, Philip Morris (21 July), Alphabet, Tesla, IBM, AT&T (23)

EU SAP (22 July), LVMH, Roche, Nestlé, Total (24), Aon, VW (25)

Upcoming CB meetings :

ECB (24 July)

FOMC/FED (30 July)

BOJ (31 July)

BOE (7 Aug)

WHAT ANALYSTS SAY

- VanEck: Quantum computing enters a new era

- Mandarine Gestion: Japan: the next destination for investors?

- Carmignac: Restoring emerging markets to their former glory

VanEck, 15 July 2025

Author: Martijn Rozemuller, General Director Europe

The growing commitment of governments and major technology companies indicates that quantum computing may well be approaching a tipping point. According to McKinsey & Company, public investment now exceeds $42 billion, reflecting the strategic interest in this transformative technology. At the same time, the private sector is advancing rapidly, with more than 10,000 quantum-related patents filed in the last five years.

Economic opportunities are already being explored in several sectors. In finance, for example, quantum computing could be used to optimise investment portfolios, refine risk analysis and detect fraud – while posing a threat to current encryption standards in the longer term.

In healthcare, it offers promising prospects for drug discovery, molecular simulation and medical data analysis. A notable example is the collaboration between IBM and the Cleveland Clinic in the United States, which led to the installation of the first quantum computer dedicated to healthcare in 2023. Among its various applications, it is used to improve machine learning models for prescribing antibiotics.

To better understand the situation, it is important to note that quantum computing is currently transitioning from theoretical research to an early commercial exploration phase – a period marked by both rapid advances and major technical challenges. As part of this transition, several companies are now offering quantum computers – either by physically delivering them or by providing remote access via cloud platforms. Over the past six months, major players in the industry have announced notable hardware advances: Google unveiled its Willow chip, Microsoft unveiled its Majorana processor, and Amazon announced Ocelot, which uses ‘cat’ qubits to improve error correction. While these developments are promising, they primarily reflect hardware advances and do not yet translate into immediate commercial utility. Most current systems still operate in what is known as the NISQ (Noisy Intermediate-Scale Quantum) era – a phase where performance is impressive on an experimental level, but limited by high error rates and a lack of scalability. These systems remain largely experimental at this stage and are not yet suitable for large-scale practical applications. As a result, the current enthusiasm is based more on long-term potential than on proven performance. The gap between laboratory breakthroughs and widespread deployment remains significant – and closing it will require continuous innovation and rigorous execution. Leading companies recognise these challenges and have established clear roadmaps to address them. IBM, for example, recently updated its quantum roadmap, with the goal of delivering a fault-tolerant quantum computer by 2029 (Example).

Quantum computing may be reaching a tipping point, with the potential to spur a wave of major innovations. As an emerging technology, its development will likely be uneven, and widespread adoption is far from guaranteed.

Investors aware of its long-term potential would therefore be well advised to follow its progress closely. The next breakthrough could be closer than we think – and for those who are prepared, it could represent a unique opportunity to engage in one of the most promising technological fields of our time.

Mandarine Gestion, 16 July 2025

Author: Augustin Lecoq, Equity Fund Manager

An unexpected depth of rating

In terms of its stock market, Japan has a very rich and deep listing, with around 4,000 listed companies, and is also notable for its proportion of small businesses, which account for around two-thirds of the total. Being listed remains the Holy Grail for any Japanese entrepreneur. It is therefore easy to find companies where the interests of investors and company directors, who are often majority shareholders, are aligned. ‘Kabunushi Yutai’ also create a virtuous circle with individuals through the distribution of vouchers and gifts to shareholders.

Welcome reforms

Faced with this problem, the Tokyo Stock Exchange has implemented measures to improve the situation, asking the least valued companies to take concrete action. First through recommendations in 2023, then by increasing pressure in 2024. This represents a real upheaval in Japanese capitalism, which has long been accustomed to cross-shareholdings between customers and suppliers and the accumulation of excessive cash reserves.

Beyond valuation issues, many microcaps are turning operational challenges into opportunities in a multitude of niches :

· The ageing population is a boon for the M&A advisory sector, with executives averaging 62 years of age and 52% of them having no natural successor.

· Japan is also lagging far behind in terms of digitalisation. Although it is at the forefront of hardware, its companies are virtually absent from the international software market, offering a boulevard of growth for companies capable of attracting talent, such as SRE, I'LL, System Support, TDC, Techmatrix, Baudroie and many others, to help the country bridge this gap.

· Faced with an increase in natural disasters, Raito Kogyo is capitalising on the recognition of its landslide prevention systems, while TRE provides post-disaster waste management, as it did recently in Fukushima.

· To combat rural depopulation, S-Pool has launched supervised farms to promote the professional integration of people with disabilities. As for Lacto Japan, the leading importer of powdered milk, it is benefiting from the crisis in the dairy industry, despite rising consumption.

· Even in the face of declining birth rates, IBJ benefits from a government aid system for its marriage agency service dedicated to Japanese people wishing to marry.

These structural advantages make Japan an ideal playground for selecting small, differentiated stocks. This region represents 25% of our investment universe, on a par with the United States and Europe, and offers genuine diversification within a global equity allocation.

Carmignac, 14 July 2025

Author: Xavier Hovasse, EM equity fund manager

China's evolution and its great leap forward in AI

Ten years ago, the quality of Chinese products was criticised for being far inferior to that of American or German products. This is no longer the case today. The country is home to some of the best scientists and engineers of the new generation, trained by its excellent education system, and has significantly strengthened its industrial capabilities and skills. China is now a world leader in renewable energy, electric vehicles (EVs) and artificial intelligence (AI). It is now the world's leading exporter of cars, with BYD selling more vehicles in Europe than Tesla.

In the field of AI, two years ago it was assumed that the United States would naturally dominate. However, DeepSeek has overturned this assumption and is now positioning itself as a serious contender in the AI race. As the world's second largest economy, China has an exceptional education system focused on science and mathematics, supported by massive government investment. US measures to restrict exports of electronic chips to China have failed. Jensen Huang, CEO of Nvidia, recently warned that Chinese companies specialising in AI are now ‘formidable’. The world is now realising that China is no longer just a low-cost manufacturing hub; it can dominate global manufacturing in almost every field. Furthermore, it is the leading trading partner for almost all emerging markets.

Beyond China, Asia remains attractive

Although attention is focused on China, Asia as a whole continues to prosper. Today, 100% of Nvidia's graphics processing units (GPUs) are manufactured by Taiwanese company TSMC, and most of its memory products come from South Korean company Hynix. The artificial intelligence revolution depends on Asia.

As for India, the country is reminiscent of China 20 years ago, with an economic model resembling ‘state capitalism’. This type of economic governance is based on a long-term vision, political stability and the mantra ‘Made in India’. In our view, this will bear fruit largely thanks to tensions between the United States and China, but also thanks to a huge and predominantly English-speaking population, a high-quality education system and an industry protected by the government, the cornerstone of Prime Minister Narendra Modi's leadership during his three terms in office. The Indian economy is expected to grow by 6% to 7% per year over the next 10 to 15 years, with very well-managed companies and, unlike China, no overcapacity. Indeed, returns on investment remain high, unlike the supply-driven Chinese economy.

Latin America, the winner of Donald Trump's new policies

Some emerging countries, such as Mexico, are benefiting from trade wars thanks to their attractiveness for the ‘relocation of production chains’ from the United States. Mexican President Claudia Sheinbaum recently strengthened relations with the United States, notably by cooperating to improve security along the border. In the south, we remain optimistic about Brazil. Brazilian equities, particularly those in the utilities sector, are significantly undervalued. Among the world's largest countries, Brazil has the highest real interest rates, above 7%, making the Brazilian real particularly attractive. Finally, in Argentina, the fiscal situation has improved significantly, moving from a large deficit to a surplus under Javier Milei's leadership, and sovereign bonds have seen an impressive recovery.

China is not the only safe bet in emerging markets; it is, of course, an integral part of them, but emerging markets as a whole are full of dynamic, global companies that are leaders in all sectors. And today, with the tailwind of Donald Trump's second term, the time seems more propitious than ever to invest in this asset class.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+374 43 00-43-82

Broker

broker@unibankinvest.am

research@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.