Last week: Wild swings in Oil (Iran), Precious Metals (T/P after ATH), individual stocks (earnings); new FED chairman

WEEKLY TRENDS

WEEKLY TRENDS

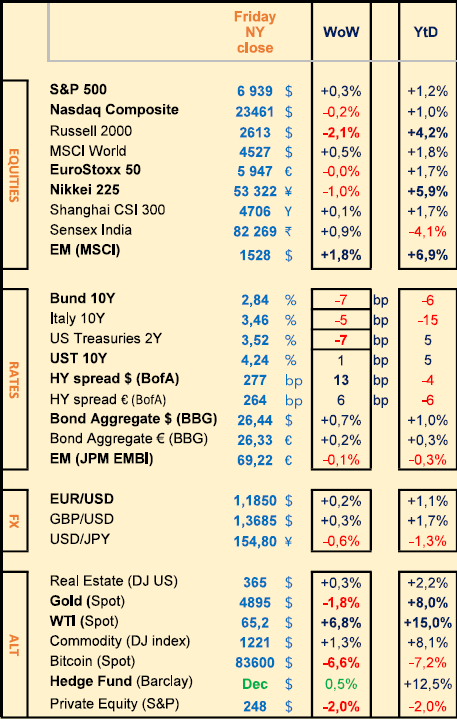

- Wild markets last week, starting with Oil ending the week at +7% (Hormuz strait fear of blockade, pushing the OPEC+ members to meet up on Sunday 1st)

- Precious Metals hitting new All Time Highs (ATH) but then hit by a series of Take Profits (T/P) on Friday with the new FED chairman nomination (Kevin Warsh perceived by markets as less aggressive than Scott Bessent)

- Q4 earnings releases (Microsoft -7% on significant Artificial Intelligence costs despite strong results)

- The FOMC/FED deciding to leave its rates unchanged, as did the Bank of Canada

- Cryptos continuing their landslide with another negative week for the BTC at -7%

- Note that the US credit risk is higher with US Corporate margins (+15bps) and a steepening of the US yield curve (+10bps) and that another wild week is to be expected next week with another series of important Q4 earnings releases (Eli Lilly, Alphabet, Palantir, Amazon) together with the ECB and the MPC/BOE rate decisions, and the most awaited January US Non Farm Payrolls (job report) to finish well a demanding week on Friday

MARKETS

Equities

Q4 earnings weekly performances:

Microsoft (-7%), Tesla (-3%), LVMH (-7%)

Meta (+7%), Apple (+3%), ABB (+11%), Exxon (+5%), ASML Hold. (+5%)

NB: UnitedHealth (-19%, on Medicare), Eramet (-15%, on bank analyst review)

M&A: OHB (+72%, Rheinmetall discussions), Puma (+17%, Anta decision)

Bank analysts: Dassault Sys (MS ‘o/w’ target €30), Eiffage (Barx ‘o/w’ target €146), Engie (Barx ‘o/w’ target €27), Airbus (JPM ‘o/w’ target €240), Alstom (JPM ‘o/w’ target €34), Burberry Group (Barx ‘o/w’ target £14.50)

Rates

US curve steepening (2-10 years) higher at 72bps (+10bps)

HY corp. spreads higher: US at +277bps (+15bps); EU at +264bps (+5)

Commodities

Oil price higher (+7%) 4 month high on Iran concerns (OPEC+ meeting Sunday 1st Feb expected to keep its oil production pause for March)

Gold price lower (-2%) after hitting new ATH - Copper hit $14500 new ATH - Silver hit $121 new ATH (PM much lower after new FED chairman announcement and T/P), Uranium highest since May 2024

US

FOMC/FED (unchanged rates, Powell: FED can afford to wait for new data before making its next move)

Crypto

BTC (-7%), ETH (-2.5%), SOL (-2%), XRP (-5%), Tether owns 3 times more Gold than BTC ($24bn vs $8bn)

Under the watch

FX: FED is said to have ‘checked rates’ (USD/JPY) last week

Nota Bene

S&P revised Italy’s outlook to positive from stable (BBB+) on Jan 30

25% of S&P returns since 2011 have been driven by share Buybacks

CALENDAR

Earnings releases:

US Palantir (2 Feb), AMD (3) Eli Lilly, Alphabet (4), Amazon (5), EU Novartis (4 Feb), Shell, Unilever (5)

Central Bank rate decisions:

MPC/BOE, ECB (4 Feb)

Macro data releases:

US Jan NFP job report (5 Feb)

WHAT ANALYSTS SAY

Lazard AM, 30 January 2026

Author: Daniel Herdt, Global Fixed Income Portfolio Manager

Scandinavia, home to some of the world's most advanced and sustainable economies, has seen its bond markets undergo significant structural changes over the past decade, attracting the interest of international investors.

High-yield bonds issued by Nordic countries are particularly notable for their consistent returns combined with moderate risks.

A strategy incorporating a performance bonus

High-yield bonds from Nordic countries are unique in that they offer significantly higher coupons and yields than traditional bonds from other developed countries, even though their default rates are comparable. This is because many Nordic issuers are relatively unknown and do not have external credit ratings.

Diversification opportunities

Nordic high yield bonds have low correlation with other market segments, making them a valuable diversification tool. In addition to broad sector and geographical diversification, exposure to this market offers a distinctive risk profile that further enhances diversification effects.

An attractive risk/return profile

Due to their low sensitivity to interest rate fluctuations and higher coupons, Nordic high-yield bonds offer significant return potential with significantly lower volatility than traditional high-yield markets.

Priority to credit quality

As bottom-up investors, our investment process aims to invest selectively in attractive securities while avoiding risks that are not sufficiently remunerated. This strategy has contributed to the fund's historical performance.

Carmignac, 30 January 2026

Authors: Kevin Thozet, Investment Committee member

The appointment of Kevin Warsh as chair of the Federal Reserve (FED) could signal a change of regime for US monetary policy, with major implications for the yield curve, liquidity and risky assets.

Beyond the anecdotal, Warsh has solid credentials. As a Fed governor during the global financial crisis, he played a key role – praised by Ben Bernanke – in maintaining constructive relations between the Fed and Congress at a time when confidence in institutions was crucial. That said, he also distinguished himself by his stubbornly unaccommodating stance on inflation. During his term as governor (2006-2011), he remained resolutely hawkish until the end of 2009, even though core inflation (PCE) had fallen to 0.6% and the unemployment rate had reached 9.9%.

Warsh is also known for his highly critical stance on the Fed's balance sheet management. He has long believed that quantitative easing policies and the accumulation of an oversized balance sheet favour Wall Street at the expense of Main Street: they support asset prices but have a limited impact on the financing conditions that really matter to low-income households and small businesses. In his analysis, QE compresses long-term rates without really easing short-term financing conditions.

It is with this logic in mind that he is now calling for two to three rate cuts in 2026. Here again, it's all about Main Street. For the wealthiest and oldest households (the upward leg of the K-shaped economy), a key rate of around 3.75% can be considered accommodative; for the most modest households (the downward leg of the K-shaped economy), even at 3%, key rates remain restrictive. In other words, monetary easing must focus on Fed Fund rates, not on the balance sheet.

But theory is one thing, practice another. Such a reorientation could not be implemented overnight. And if it were to materialise, it would be part of a gradual transition, coordinated with the US Treasury (Scott Bessent), which for its part would aim to limit long-term issuance and deregulate the banking sector.

The natural consequence would be a steepening of the US yield curve. Short-term rates would be pulled down by cuts in key rates, while long-term rates would be left to market forces – in an environment characterised by a resilient US economy, probably accelerating again, persistent inflationary pressures, high public deficits and a sustained supply of Treasuries.

For risky assets, however, this policy mix could be interpreted as moderately negative. Balance sheet reduction in a context of high budget deficits implies an increase in the net supply of bonds that markets will have to absorb, in an already fragile liquidity environment.

Recurring tensions in the repo markets and episodes of stress on short-term financing suggest that liquidity conditions are far from benign. In this context, a less favourable balance sheet policy could weigh on equities and other risky assets, even if short-term rate cuts will provide support to the real economy.

Aberdeen Investments, 30 January 2026

Authors: Karsten-Dirk Steffens, Country Head

Emerging market equities and bonds have been among the big winners in recent months. After a ‘lost decade’ in which they significantly underperformed the spectacular rise of US markets, they are now experiencing a remarkable renaissance. This is not euphoric, but rationally based.

The American myth is crumbling

Lower interest rates in the United States, high public debt and political volatility have undermined the appeal of the dollar. For emerging markets, this is a real relief: debt servicing is becoming less expensive, inflationary pressures are easing and central banks are regaining room for manoeuvre. A long-absent mechanism is re-emerging: rate cuts are supporting growth, bonds are rising, equities are benefiting – all amplified by currency gains.

This is much more than just a market cycle. We are witnessing a structural shift: belief in American exceptionalism is eroding. Not because of economic weakness, but because of political unpredictability – a trait once attributed mainly to emerging markets.

Mexico and China in the spotlight

Despite US tariffs, Mexico is among the big winners. Focusing solely on trade barriers misses the point: a stable currency, falling interest rates and solid earnings. China, too, is showing resilience despite high tariffs and ongoing geopolitical tensions. The renminbi remains stable, inflation is contained and monetary policy is accommodative. The determining factor remains access to structural growth, particularly in key sectors such as artificial intelligence.

Capital follows economic arguments, not political sensitivities. In this respect, the markets are often more lucid than the public debate.

Europe is underestimated

For Europe, one conclusion is clear: the continent is not as helpless as it sometimes tends to believe. Europe's problem is not so much a lack of substance as a lack of self-confidence. In a world dominated by power struggles and uncertainty, Europe too often turns inwards.

Yet certain asset classes and investment strategies are precisely benefiting from the current global changes. European institutional investors are strongly interconnected on a global scale, benefit from a stable regulatory framework and have robust financial foundations. They must capitalise on these strengths.

For decades, structural bull market risk has been concentrated almost exclusively on equities. High US debt is now also putting pressure on bonds. China has massively reduced its holdings of US Treasury bonds, while Europe still holds a significant portion. This is not a cause for alarm, but a strategic call for vigilance.

Equities

Q4 earnings weekly performances:

Microsoft (-7%), Tesla (-3%), LVMH (-7%)

Meta (+7%), Apple (+3%), ABB (+11%), Exxon (+5%), ASML Hold. (+5%)

NB: UnitedHealth (-19%, on Medicare), Eramet (-15%, on bank analyst review)

M&A: OHB (+72%, Rheinmetall discussions), Puma (+17%, Anta decision)

Bank analysts: Dassault Sys (MS ‘o/w’ target €30), Eiffage (Barx ‘o/w’ target €146), Engie (Barx ‘o/w’ target €27), Airbus (JPM ‘o/w’ target €240), Alstom (JPM ‘o/w’ target €34), Burberry Group (Barx ‘o/w’ target £14.50)

Rates

US curve steepening (2-10 years) higher at 72bps (+10bps)

HY corp. spreads higher: US at +277bps (+15bps); EU at +264bps (+5)

Commodities

Oil price higher (+7%) 4 month high on Iran concerns (OPEC+ meeting Sunday 1st Feb expected to keep its oil production pause for March)

Gold price lower (-2%) after hitting new ATH - Copper hit $14500 new ATH - Silver hit $121 new ATH (PM much lower after new FED chairman announcement and T/P), Uranium highest since May 2024

US

FOMC/FED (unchanged rates, Powell: FED can afford to wait for new data before making its next move)

Crypto

BTC (-7%), ETH (-2.5%), SOL (-2%), XRP (-5%), Tether owns 3 times more Gold than BTC ($24bn vs $8bn)

Under the watch

FX: FED is said to have ‘checked rates’ (USD/JPY) last week

Nota Bene

S&P revised Italy’s outlook to positive from stable (BBB+) on Jan 30

25% of S&P returns since 2011 have been driven by share Buybacks

CALENDAR

Earnings releases:

US Palantir (2 Feb), AMD (3) Eli Lilly, Alphabet (4), Amazon (5), EU Novartis (4 Feb), Shell, Unilever (5)

Central Bank rate decisions:

MPC/BOE, ECB (4 Feb)

Macro data releases:

US Jan NFP job report (5 Feb)

WHAT ANALYSTS SAY

- Lazard: Nordic countries HY bonds

- Carmignac: Change of regime under the new FED Chairman Kevin Warsh

- Aberdeen: 'Trumpified' World order, Emerging Markets are the winners

Lazard AM, 30 January 2026

Author: Daniel Herdt, Global Fixed Income Portfolio Manager

Scandinavia, home to some of the world's most advanced and sustainable economies, has seen its bond markets undergo significant structural changes over the past decade, attracting the interest of international investors.

High-yield bonds issued by Nordic countries are particularly notable for their consistent returns combined with moderate risks.

A strategy incorporating a performance bonus

High-yield bonds from Nordic countries are unique in that they offer significantly higher coupons and yields than traditional bonds from other developed countries, even though their default rates are comparable. This is because many Nordic issuers are relatively unknown and do not have external credit ratings.

Diversification opportunities

Nordic high yield bonds have low correlation with other market segments, making them a valuable diversification tool. In addition to broad sector and geographical diversification, exposure to this market offers a distinctive risk profile that further enhances diversification effects.

An attractive risk/return profile

Due to their low sensitivity to interest rate fluctuations and higher coupons, Nordic high-yield bonds offer significant return potential with significantly lower volatility than traditional high-yield markets.

Priority to credit quality

As bottom-up investors, our investment process aims to invest selectively in attractive securities while avoiding risks that are not sufficiently remunerated. This strategy has contributed to the fund's historical performance.

Carmignac, 30 January 2026

Authors: Kevin Thozet, Investment Committee member

The appointment of Kevin Warsh as chair of the Federal Reserve (FED) could signal a change of regime for US monetary policy, with major implications for the yield curve, liquidity and risky assets.

Beyond the anecdotal, Warsh has solid credentials. As a Fed governor during the global financial crisis, he played a key role – praised by Ben Bernanke – in maintaining constructive relations between the Fed and Congress at a time when confidence in institutions was crucial. That said, he also distinguished himself by his stubbornly unaccommodating stance on inflation. During his term as governor (2006-2011), he remained resolutely hawkish until the end of 2009, even though core inflation (PCE) had fallen to 0.6% and the unemployment rate had reached 9.9%.

Warsh is also known for his highly critical stance on the Fed's balance sheet management. He has long believed that quantitative easing policies and the accumulation of an oversized balance sheet favour Wall Street at the expense of Main Street: they support asset prices but have a limited impact on the financing conditions that really matter to low-income households and small businesses. In his analysis, QE compresses long-term rates without really easing short-term financing conditions.

It is with this logic in mind that he is now calling for two to three rate cuts in 2026. Here again, it's all about Main Street. For the wealthiest and oldest households (the upward leg of the K-shaped economy), a key rate of around 3.75% can be considered accommodative; for the most modest households (the downward leg of the K-shaped economy), even at 3%, key rates remain restrictive. In other words, monetary easing must focus on Fed Fund rates, not on the balance sheet.

But theory is one thing, practice another. Such a reorientation could not be implemented overnight. And if it were to materialise, it would be part of a gradual transition, coordinated with the US Treasury (Scott Bessent), which for its part would aim to limit long-term issuance and deregulate the banking sector.

The natural consequence would be a steepening of the US yield curve. Short-term rates would be pulled down by cuts in key rates, while long-term rates would be left to market forces – in an environment characterised by a resilient US economy, probably accelerating again, persistent inflationary pressures, high public deficits and a sustained supply of Treasuries.

For risky assets, however, this policy mix could be interpreted as moderately negative. Balance sheet reduction in a context of high budget deficits implies an increase in the net supply of bonds that markets will have to absorb, in an already fragile liquidity environment.

Recurring tensions in the repo markets and episodes of stress on short-term financing suggest that liquidity conditions are far from benign. In this context, a less favourable balance sheet policy could weigh on equities and other risky assets, even if short-term rate cuts will provide support to the real economy.

Aberdeen Investments, 30 January 2026

Authors: Karsten-Dirk Steffens, Country Head

Emerging market equities and bonds have been among the big winners in recent months. After a ‘lost decade’ in which they significantly underperformed the spectacular rise of US markets, they are now experiencing a remarkable renaissance. This is not euphoric, but rationally based.

The American myth is crumbling

Lower interest rates in the United States, high public debt and political volatility have undermined the appeal of the dollar. For emerging markets, this is a real relief: debt servicing is becoming less expensive, inflationary pressures are easing and central banks are regaining room for manoeuvre. A long-absent mechanism is re-emerging: rate cuts are supporting growth, bonds are rising, equities are benefiting – all amplified by currency gains.

This is much more than just a market cycle. We are witnessing a structural shift: belief in American exceptionalism is eroding. Not because of economic weakness, but because of political unpredictability – a trait once attributed mainly to emerging markets.

Mexico and China in the spotlight

Despite US tariffs, Mexico is among the big winners. Focusing solely on trade barriers misses the point: a stable currency, falling interest rates and solid earnings. China, too, is showing resilience despite high tariffs and ongoing geopolitical tensions. The renminbi remains stable, inflation is contained and monetary policy is accommodative. The determining factor remains access to structural growth, particularly in key sectors such as artificial intelligence.

Capital follows economic arguments, not political sensitivities. In this respect, the markets are often more lucid than the public debate.

Europe is underestimated

For Europe, one conclusion is clear: the continent is not as helpless as it sometimes tends to believe. Europe's problem is not so much a lack of substance as a lack of self-confidence. In a world dominated by power struggles and uncertainty, Europe too often turns inwards.

Yet certain asset classes and investment strategies are precisely benefiting from the current global changes. European institutional investors are strongly interconnected on a global scale, benefit from a stable regulatory framework and have robust financial foundations. They must capitalise on these strengths.

For decades, structural bull market risk has been concentrated almost exclusively on equities. High US debt is now also putting pressure on bonds. China has massively reduced its holdings of US Treasury bonds, while Europe still holds a significant portion. This is not a cause for alarm, but a strategic call for vigilance.

Contacts

8 Kievyan Street, Yerevan, Armenia

+374 10 712 259

+374 43 004 182

unibankinvest@unibank.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.