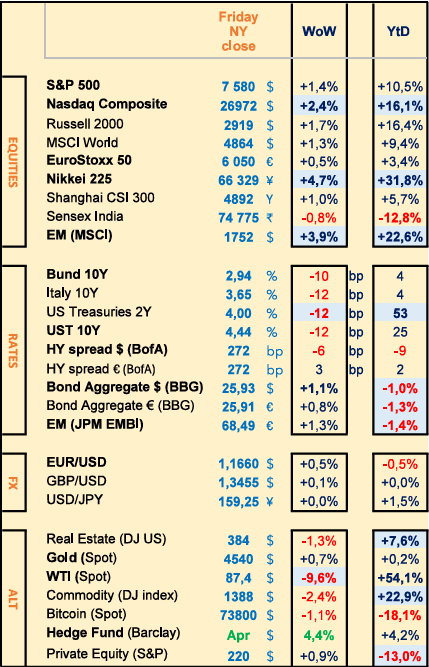

Last week : 9th straight week ATH for SP500 (Dell +57%) ; Nikkei +5% ; EM +4% (all due to earnings and lower Oil price)

WEEKLY TRENDS

WEEKLY TRENDS

- In a 4 day week, the US stocks posted their 9th straight weekly gain due to Oil price much lower (-10%) with hope of a US-Iran peace agreement and also due to an AI linked stocks optimism (Dell was up 57% after strong earnings released last week, Micron +18% on the week).

- US Q1 GDP was revised down (2nd estimate) at +1.6% and the US April PCE was released higher than in March but lower than expected, leading to US treasury yields lower across the board (markets still expect a FED rate increase but not until early 2027 now). Nikkei was up 4.5% WoW mostly due to lower Oil price (Japan imports nearly all its energy).

- Next week, all eyes will be on the US NFP job report for May (to be released on Friday) and a few corporate earnings releases with HP, Palo Alto, Broadcom, CrowdStrike and Inditex. (Note Adobe and Micron Tech will release theirs on the 11th and 24th respectively, Nike on the 30th). Next Central Banks rate decision meetings shall be on 11 June (ECB), 16 June (BOJ, RBA) 17 June (FED) and 18 June (BOE).

MARKETS

Equities

Q4 earnings weekly performances :

Marvell (+5%) Salesforce (+7%) Dell (+57%)

M&A : Akzo Nobel (+26% WoW) after it rejected a €12bn offer from Nippon Paint and Sherwin-Williams

Buybacks : Salvatore Ferragamo (+23%) €53m buyback programme

Bank analysts : Essilorluxottica (MS ‘o/w’ target €225) Eiffage (Citi ‘buy’ target €155) Richemont (Barclays ‘o/w’ target ₣195, UBS ’buy’ target is at ₣186) Iberdrola (Barclays ‘o/w’ target €22.50)

Rates

US curve steepening (2-10 years) stable at +44bps

HY corp. spreads mixed : US at +272bps (-6) EU at +272bps (+3bps)

Commodities

Oil price WTI much lower (-10%) after -8% the previous week (Note US SPR stocks at 2 year low)

Gold price slightly higher (+0.5%) due to lower US yields. Silver (-1.5%)

Crypto

BTC (-1%) ; ETH (-5%) SOL (-4%) XRP (-3%)

US

April PCE (+3.8% vs +3.5% prior) Core at +3.3% vs +3.2% prior

Q1 GDP (2nd estimate) +1.6% vs +2.0% prior read

Under the watch

Anthropic Q1 valuation ($380bn) Q2 should be around $900bn

Nota Bene

GS TMT AI basket +42% YTD (SP500 +10%, SP 500 ex AI is at +3.5%)

CALENDAR

Earnings releases : US HP (1st June) Palo Alto Networks (2) Broadcom, Costco Wholesale, CrowdStrike (3) , EU Inditex (3) Remy Cointreau (4)

Macro Data releases : US May NFP (5th June)

WHAT ANALYSTS SAY

Amundi, May 2026

Authors : Vincent Mortier, Group CIO

Efforts at ending the war and a fragile ceasefire have supported risk assets, but gains have been repeatedly tempered by a lack of resolution to the conflict and by the prospect of rates staying higher for longer. Market moves may be summarised by how the narrative has shifted between ceasefire or no ceasefire, risk-on or risk-off, and inflation and growth concerns. Looking ahead, we think:

· The main risk is the pass- through of headline inflation into core. Economies already experiencing high inflation may see convergence to target interrupted, while economies already at target face a non-negligible risk of expectations becoming de-anchored.

· The growth outlook is weaker (notrecessionary), depending on the persistence and propagation of this shock to the economy, and the length of time energy prices remain high. The positive momentum expected in early 2026 has given way to more subdued growth, due to the squeeze on real incomes and falling business confidence.

· The developed market fiscal outlook was already strained before this crisis, and as a result we do not expect fiscal support to be broad- based in most parts of the world, including the US, Eurozone(EZ) and UK . It would be targeted, with selective relief for households and strategic sectors. Even in emerging markets (EM), responses will be country-specific.

Factors we are closely monitoring to change our views.

A longer period of disruption in the supply of oil, gas and other commodities from the Gulf would lead to second-round effects in the economy. This means a pass-through of the crisis to energy, transport and other parts of the economy will affect prices in general. But if a pass-through to consumer prices is not possible, then corporate margins will be affected, implying a change in our views. Europe, in particular, is vulnerable to this shock. Any hawkish shift in central banks’response will be extremely important. If the Fed or ECB shows renewed hawkish tendencies, our call on duration, particularly for the front end, would change. Revisions in earnings per share (EPS), as a consequence of a more persistent crisis. Liquidity and credit transmission are supportive for risk assets at present. Equity volatility is low, and we do not see outflows in fixed income credit; technicals are also reasonable. Any change here would affect our views.

This is a time to lean on long- term convictions and, if risk assets offer an opportunity, explore areas where earnings and fundamentals are robust, while maintaining safeguards.

· In fixed income, we are not calling for a directional bet on duration but rather for a focus on different yield curves and relative value. The front end of the curve remains sensitive to hawkish repricing, while weaker economic growth should, overtime, limit the long end. This calls for a more nuanced investment approach. On duration, we upgraded the UK and are now neutral on the US. We are also selectively exploring corporate credit, and EM debt on which were main positive, although we’ve tactically downgraded Indian bonds.

· In equities, the recovery seen in April is indicative of markets’ view on a quick solution to the Middle East crisis. While the US is structurally the strongest region in equities, it’s also the most concentrated, and in some cases, is showing high valuations. Hence, we look for value in regions such as Europe, Japan and emerging markets like Latin America. Even though Europe may be less compelling as a pure beta play, it is more interesting through sector dispersion and selective themes such as industrial policy, infrastructure and defence.

· In multi asset, the crisis is leading us to maintain a more nuanced stance across asset classes and regions. We aim to balance short-term opportunities with long-term convictions, staying slightly positive on risk and keeping a diversified stance. We also think that gold is not just a diversifier against geopolitical risks, but also a hedge against policy ambiguity from central banks.

Lombard Odier, 28 May 2026

Author : Luca Bindelli, Head of Investment Strategy

Rising government bond yields tend to put pressure on equity valuations. Following the recent bond market correction, yields have reached multi-year highs in many major economies. However, the impact of rising rates on equities depends on the reason behind the rise: stronger growth, which generally leads to higher real interest rates, or rising inflation expectations. It also depends on the volatility of yields across different bond maturities. The main driver of the recent rise in yields is growing inflation expectations, as markets have already priced in some tightening of central bank monetary policy. In the US, equity prices imply one rate hike by the Federal Reserve, compared with around three in Europe. The current situation differs from that of 2022, when central banks had to raise their key rates hastily against a backdrop of high inflation and real rates in deeply negative territory, causing high volatility and weighing on equity markets. It seems unlikely that central banks will exceed market expectations in terms of monetary tightening. On the contrary, they should be able to cut their rates. Furthermore, although inflation risks may rise if disruptions in the Strait of Hormuz persist, this is not our base case scenario. While rising yields are certainly likely to exert temporary pressure, we do not anticipate a sustained decline in equity valuations.

Can earnings continue to drive share prices higher?

Despite a strong Q1, earnings forecasts for 2026 have been revised upwards once again, driven by EM, Japan and the US . This remains a key support for equities, particularly as valuations in some developed markets are becoming harder to justify – once again exceeding long-term averages. We remain optimistic about the technology sector, where valuations suggest upside potential. Massive investment in AI, in data centres and record demand in the semiconductor and cloud/software sectors continue to underpin earnings.

EM offer more attractive prospects: stronger earnings growth momentum than in developed markets, more attractive valuations and a favourable investor sentiment, particularly if the US dollar remains weak. Our overweight position in equities is therefore reflected in EM stocks, whose performance appears set to extend beyond AI-driven markets. South Korea stands out due to accelerating spending on AI infrastructure and strengthened corporate governance. China and South Africa also offer attractive valuations and earnings. Chinese earnings growth is expected to recover in 2026 and 2027, supported by exports, investment in AI, moderating competition and energy resilience, whilst South African mining companies (40% of the country’s index), are expected to benefit from structurally high demand for Gold. Earnings continue to underpin global equity markets, but we maintain a selective approach, as quality and geographical region are key determinants.

Are bonds still a reliable source of diversification?

The paradigm has shifted in recent years. The previous economic cycle was characterised by low inflation, demand shocks and concerns about growth. Sovereign bonds served as effective diversification tools, as growth shocks tended to lead to a fall in real interest rates and support bond prices. In 2022, the energy supply shock led to a rise in inflation and forced central banks to tighten monetary policy sharply. The resulting fall in sovereign bond prices amplified portfolio losses rather than cushioning them. No asset is defensive in absolute terms, but only relative to the type of shock to which it is exposed. Sovereign bonds generally perform well when the dominant risk is a growth shock – as was the case during the global financial crisis. They perform less well in the face of an inflationary or supply shock.

VanEck, 26 May 2026

Authors : Imaru Casanova, Portfolio Manager

Global demand for gold rose by 2% YoY in Q1 2026, driven by central bank purchases and demand for bars and coins. Newmont and Agnico Eagle reported record results despite low valuations.

Key points :

· Strong demand for gold continues, underpinned by central bank purchases and resilient demand for physical investment

· Inflation expectations and real interest rates remain the key drivers of the outlook for the price of Gold

· Shares in Gold mining companies are posting strong results and cash flows, whilst their valuations remain relatively low

Central banks remained net buyers, adding 244 tonnes during Q1, representing a 3% year-on-year increase. This trend continued despite a reported rise in selling activity, notably including transactions by Turkey, Azerbaijan’s SOFAZ and the Central Bank of Russia. Net demand remained positive, thanks to purchases by countries such as Poland, Uzbekistan and China, as well as new entrants such as Guatemala, Cambodia, Malaysia, Serbia and the United Arab Emirates. This pattern could indicate that central bank demand for gold remains resilient.

Ongoing geopolitical developments, notably tensions in the Middle East, have been accompanied by sustained interest in gold as a reserve asset. Some sales appear to be driven by short-term liquidity needs rather than a shift in long-term reserve strategy. Demand for gold-backed ETFs totalled 62 tonnes in Q1, down from the 230 tonnes of inflows recorded over the same period last year, with US funds seeing outflows in March. Overall investment demand was, however, supported by strong demand for bars and coins, up 42% year-on-year to 474 tonnes. This is one of the highest quarterly levels ever recorded, driven largely by Asian investors.

A key factor for gold lies in how inflation expectations are reflected across different measures. The University of Michigan’s April survey showed that consumers’ 1-year and 5-year inflation expectations stood at 4.7% and 3.5% respectively. Conversely, the 5-year TIPS break-even rate, a market measure, stands at around 2.7%, keeping real rates comfortably in positive territory, for now. If bond markets were to close this gap and reflect something closer to what consumers are already anticipating, a ‘Fed on hold’ could quickly result in real rates close to zero, or even negative — a scenario that is historically among the most favourable for gold.

Shares in gold mining companies have historically outperformed the metal itself in a rising gold price environment. However, investors do not necessarily have to wait for the next bull run to start increasing their exposure. At current gold prices, these companies are already generating record cash flows, as the first-quarter 2026 results amply demonstrate. Newmont and Agnico Eagle, the world’s two largest gold mining companies, have both reported record quarterly results. This record profitability is funding the expansion of exploration programmes and growth pipelines, whilst leaving sufficient scope to reward shareholders through sustainable dividend policies and the continuation of substantial share buyback programmes. Both companies ended the quarter with approximately $3bn in net cash and strong liquidity positions.

In summary, the sector appears to be in good financial and operational health by historical standards. Despite these fundamentals, valuations in the gold mining sector remain relatively low compared to historical levels. Current share prices appear to reflect more cautious assumptions than the current price of gold would suggest.

Equities

Q4 earnings weekly performances :

Marvell (+5%) Salesforce (+7%) Dell (+57%)

M&A : Akzo Nobel (+26% WoW) after it rejected a €12bn offer from Nippon Paint and Sherwin-Williams

Buybacks : Salvatore Ferragamo (+23%) €53m buyback programme

Bank analysts : Essilorluxottica (MS ‘o/w’ target €225) Eiffage (Citi ‘buy’ target €155) Richemont (Barclays ‘o/w’ target ₣195, UBS ’buy’ target is at ₣186) Iberdrola (Barclays ‘o/w’ target €22.50)

Rates

US curve steepening (2-10 years) stable at +44bps

HY corp. spreads mixed : US at +272bps (-6) EU at +272bps (+3bps)

Commodities

Oil price WTI much lower (-10%) after -8% the previous week (Note US SPR stocks at 2 year low)

Gold price slightly higher (+0.5%) due to lower US yields. Silver (-1.5%)

Crypto

BTC (-1%) ; ETH (-5%) SOL (-4%) XRP (-3%)

US

April PCE (+3.8% vs +3.5% prior) Core at +3.3% vs +3.2% prior

Q1 GDP (2nd estimate) +1.6% vs +2.0% prior read

Under the watch

Anthropic Q1 valuation ($380bn) Q2 should be around $900bn

Nota Bene

GS TMT AI basket +42% YTD (SP500 +10%, SP 500 ex AI is at +3.5%)

CALENDAR

Earnings releases : US HP (1st June) Palo Alto Networks (2) Broadcom, Costco Wholesale, CrowdStrike (3) , EU Inditex (3) Remy Cointreau (4)

Macro Data releases : US May NFP (5th June)

WHAT ANALYSTS SAY

Amundi, May 2026

Authors : Vincent Mortier, Group CIO

Efforts at ending the war and a fragile ceasefire have supported risk assets, but gains have been repeatedly tempered by a lack of resolution to the conflict and by the prospect of rates staying higher for longer. Market moves may be summarised by how the narrative has shifted between ceasefire or no ceasefire, risk-on or risk-off, and inflation and growth concerns. Looking ahead, we think:

· The main risk is the pass- through of headline inflation into core. Economies already experiencing high inflation may see convergence to target interrupted, while economies already at target face a non-negligible risk of expectations becoming de-anchored.

· The growth outlook is weaker (notrecessionary), depending on the persistence and propagation of this shock to the economy, and the length of time energy prices remain high. The positive momentum expected in early 2026 has given way to more subdued growth, due to the squeeze on real incomes and falling business confidence.

· The developed market fiscal outlook was already strained before this crisis, and as a result we do not expect fiscal support to be broad- based in most parts of the world, including the US, Eurozone(EZ) and UK . It would be targeted, with selective relief for households and strategic sectors. Even in emerging markets (EM), responses will be country-specific.

Factors we are closely monitoring to change our views.

A longer period of disruption in the supply of oil, gas and other commodities from the Gulf would lead to second-round effects in the economy. This means a pass-through of the crisis to energy, transport and other parts of the economy will affect prices in general. But if a pass-through to consumer prices is not possible, then corporate margins will be affected, implying a change in our views. Europe, in particular, is vulnerable to this shock. Any hawkish shift in central banks’response will be extremely important. If the Fed or ECB shows renewed hawkish tendencies, our call on duration, particularly for the front end, would change. Revisions in earnings per share (EPS), as a consequence of a more persistent crisis. Liquidity and credit transmission are supportive for risk assets at present. Equity volatility is low, and we do not see outflows in fixed income credit; technicals are also reasonable. Any change here would affect our views.

This is a time to lean on long- term convictions and, if risk assets offer an opportunity, explore areas where earnings and fundamentals are robust, while maintaining safeguards.

· In fixed income, we are not calling for a directional bet on duration but rather for a focus on different yield curves and relative value. The front end of the curve remains sensitive to hawkish repricing, while weaker economic growth should, overtime, limit the long end. This calls for a more nuanced investment approach. On duration, we upgraded the UK and are now neutral on the US. We are also selectively exploring corporate credit, and EM debt on which were main positive, although we’ve tactically downgraded Indian bonds.

· In equities, the recovery seen in April is indicative of markets’ view on a quick solution to the Middle East crisis. While the US is structurally the strongest region in equities, it’s also the most concentrated, and in some cases, is showing high valuations. Hence, we look for value in regions such as Europe, Japan and emerging markets like Latin America. Even though Europe may be less compelling as a pure beta play, it is more interesting through sector dispersion and selective themes such as industrial policy, infrastructure and defence.

· In multi asset, the crisis is leading us to maintain a more nuanced stance across asset classes and regions. We aim to balance short-term opportunities with long-term convictions, staying slightly positive on risk and keeping a diversified stance. We also think that gold is not just a diversifier against geopolitical risks, but also a hedge against policy ambiguity from central banks.

Lombard Odier, 28 May 2026

Author : Luca Bindelli, Head of Investment Strategy

Rising government bond yields tend to put pressure on equity valuations. Following the recent bond market correction, yields have reached multi-year highs in many major economies. However, the impact of rising rates on equities depends on the reason behind the rise: stronger growth, which generally leads to higher real interest rates, or rising inflation expectations. It also depends on the volatility of yields across different bond maturities. The main driver of the recent rise in yields is growing inflation expectations, as markets have already priced in some tightening of central bank monetary policy. In the US, equity prices imply one rate hike by the Federal Reserve, compared with around three in Europe. The current situation differs from that of 2022, when central banks had to raise their key rates hastily against a backdrop of high inflation and real rates in deeply negative territory, causing high volatility and weighing on equity markets. It seems unlikely that central banks will exceed market expectations in terms of monetary tightening. On the contrary, they should be able to cut their rates. Furthermore, although inflation risks may rise if disruptions in the Strait of Hormuz persist, this is not our base case scenario. While rising yields are certainly likely to exert temporary pressure, we do not anticipate a sustained decline in equity valuations.

Can earnings continue to drive share prices higher?

Despite a strong Q1, earnings forecasts for 2026 have been revised upwards once again, driven by EM, Japan and the US . This remains a key support for equities, particularly as valuations in some developed markets are becoming harder to justify – once again exceeding long-term averages. We remain optimistic about the technology sector, where valuations suggest upside potential. Massive investment in AI, in data centres and record demand in the semiconductor and cloud/software sectors continue to underpin earnings.

EM offer more attractive prospects: stronger earnings growth momentum than in developed markets, more attractive valuations and a favourable investor sentiment, particularly if the US dollar remains weak. Our overweight position in equities is therefore reflected in EM stocks, whose performance appears set to extend beyond AI-driven markets. South Korea stands out due to accelerating spending on AI infrastructure and strengthened corporate governance. China and South Africa also offer attractive valuations and earnings. Chinese earnings growth is expected to recover in 2026 and 2027, supported by exports, investment in AI, moderating competition and energy resilience, whilst South African mining companies (40% of the country’s index), are expected to benefit from structurally high demand for Gold. Earnings continue to underpin global equity markets, but we maintain a selective approach, as quality and geographical region are key determinants.

Are bonds still a reliable source of diversification?

The paradigm has shifted in recent years. The previous economic cycle was characterised by low inflation, demand shocks and concerns about growth. Sovereign bonds served as effective diversification tools, as growth shocks tended to lead to a fall in real interest rates and support bond prices. In 2022, the energy supply shock led to a rise in inflation and forced central banks to tighten monetary policy sharply. The resulting fall in sovereign bond prices amplified portfolio losses rather than cushioning them. No asset is defensive in absolute terms, but only relative to the type of shock to which it is exposed. Sovereign bonds generally perform well when the dominant risk is a growth shock – as was the case during the global financial crisis. They perform less well in the face of an inflationary or supply shock.

VanEck, 26 May 2026

Authors : Imaru Casanova, Portfolio Manager

Global demand for gold rose by 2% YoY in Q1 2026, driven by central bank purchases and demand for bars and coins. Newmont and Agnico Eagle reported record results despite low valuations.

Key points :

· Strong demand for gold continues, underpinned by central bank purchases and resilient demand for physical investment

· Inflation expectations and real interest rates remain the key drivers of the outlook for the price of Gold

· Shares in Gold mining companies are posting strong results and cash flows, whilst their valuations remain relatively low

Central banks remained net buyers, adding 244 tonnes during Q1, representing a 3% year-on-year increase. This trend continued despite a reported rise in selling activity, notably including transactions by Turkey, Azerbaijan’s SOFAZ and the Central Bank of Russia. Net demand remained positive, thanks to purchases by countries such as Poland, Uzbekistan and China, as well as new entrants such as Guatemala, Cambodia, Malaysia, Serbia and the United Arab Emirates. This pattern could indicate that central bank demand for gold remains resilient.

Ongoing geopolitical developments, notably tensions in the Middle East, have been accompanied by sustained interest in gold as a reserve asset. Some sales appear to be driven by short-term liquidity needs rather than a shift in long-term reserve strategy. Demand for gold-backed ETFs totalled 62 tonnes in Q1, down from the 230 tonnes of inflows recorded over the same period last year, with US funds seeing outflows in March. Overall investment demand was, however, supported by strong demand for bars and coins, up 42% year-on-year to 474 tonnes. This is one of the highest quarterly levels ever recorded, driven largely by Asian investors.

A key factor for gold lies in how inflation expectations are reflected across different measures. The University of Michigan’s April survey showed that consumers’ 1-year and 5-year inflation expectations stood at 4.7% and 3.5% respectively. Conversely, the 5-year TIPS break-even rate, a market measure, stands at around 2.7%, keeping real rates comfortably in positive territory, for now. If bond markets were to close this gap and reflect something closer to what consumers are already anticipating, a ‘Fed on hold’ could quickly result in real rates close to zero, or even negative — a scenario that is historically among the most favourable for gold.

Shares in gold mining companies have historically outperformed the metal itself in a rising gold price environment. However, investors do not necessarily have to wait for the next bull run to start increasing their exposure. At current gold prices, these companies are already generating record cash flows, as the first-quarter 2026 results amply demonstrate. Newmont and Agnico Eagle, the world’s two largest gold mining companies, have both reported record quarterly results. This record profitability is funding the expansion of exploration programmes and growth pipelines, whilst leaving sufficient scope to reward shareholders through sustainable dividend policies and the continuation of substantial share buyback programmes. Both companies ended the quarter with approximately $3bn in net cash and strong liquidity positions.

In summary, the sector appears to be in good financial and operational health by historical standards. Despite these fundamentals, valuations in the gold mining sector remain relatively low compared to historical levels. Current share prices appear to reflect more cautious assumptions than the current price of gold would suggest.

Contacts

8 Kievyan Street, Yerevan, Armenia

+374 10 712 259

+374 43 004 182

unibankinvest@unibank.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.