Last week: US Supreme Court ruled against Trump’s tariffs; higher EU stocks; higher Oil (Iran); lower US GDP in Q4

WEEKLY TRENDS

WEEKLY TRENDS

- The US Supreme Court has finally ruled against Trump’s tariffs (6 votes against 3), the EU stocks benefitted the most so far (+2.5% WoW). Trump almost immediately announced a new global tariff at 10% for 5 months. This ruling invalidates half of all tariffs imposed under Trump ($175bn at risk of refunds, though the Supreme court did not address those yet). Sectorial tariffs on steel and aluminium remain

- US Core PCE for Dec was released higher than expected at +3% vs 2.8% in Nov, while US Q4 GDP was down sharply at +1.4% vs Q3 at +4.4% pushing the 10yr UST yield to briefly break the 4% mark last week (finished up at 4.08% on Friday)

- The last FOMC/FED meeting minutes revealed that the members were in favour of a status quo for a longer period

- US Dec trade deficit shrank with China and Canada but widened with Mexico and Taiwan

- In the PE world, Blue Owl halted redemptions on its retail private credit fund as quarterly withdrawals went up to 6% vs a 5% limit (PE stocks down)

- Next week’s star of the earnings season, Nvidia, shall publish its Q4 results and outlook, also note that China’s markets will only reopen on Tuesday

MARKETS

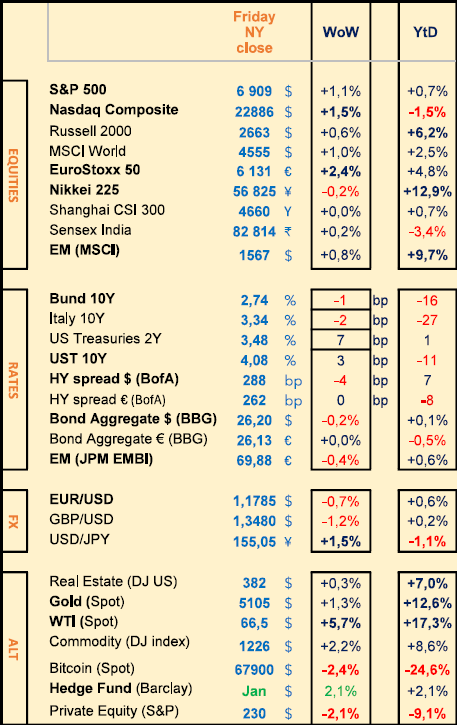

Equities

Q4 earnings weekly performances:

Analog Dev. (+8%), Warner Bros (+2%), BAE Sys (+10%), Danone (+2%)

Walmart (-8%), Nexans (-8%), Airbus (-2%), Rio Tinto (-3%)

NB: Eramet (-18%), Moncler (+12%), Bayer (-5%)

Bank analysts: Siemens Energy (GS ‘buy’ target €185), Anheuser Inbev (MS ‘o/w’ target €74), Arcelormittal (MS ‘o/w’ target 54€)

Rates

US curve steepening (2-10 years) lower at +60bps (-4bps)

HY corp. spreads lower: US at +288bps (-5bps); EU stable at +262bps

Commodities

Oil price higher (+5.5%) due to US military presence around Hormuz strait

Gold price higher (+1.5%) despite a stronger USD

US

Dec Core PCE at +3% vs +2.8% prior; Q4 GDP at +1.4% vs +4.4% in Q3

Crypto

BTC (-2.5%) the 5th consecutive negative week; SOL (-4%) ; XRP (-6%)

Under the watch

FED injected $18bn into the US banking system last week (via o/n repo)

$10trn of US gov. debts are to be refinanced over the next 12 months

Lagarde said to leave much before Oct 2027 (end of her mandate)

Nota Bene

End of Buyback blackout window (for 80% of the SP500 corporates)

SWE bench (repair evaluations) new DeepSeek V4 expected at 83.7% vs Claude at 80.9% GPT 80% Gemini 76% and DeepSeek V3 at 73%

ECB to provide euro liquidity to broad set of CBs vs high quality euro denominated collateral (Q3 2026)

CALENDAR

Earnings releases :

US Home Depot (24 Feb), Nvidia (25), Salesforce (26)

EU HSBC (25 Feb), Schneider Elec, Allianz (26), BASF, Swiss Re, Holcim (27)

Macro data releases:

US Jan PPI (27)

WHAT ANALYSTS SAY

Edmond de Rothschild AM, 20 February 2026

Author: Benjamin Melman, Global Chief Investment Officer

Improvements in software efficiency and lower AI-related costs should lead to an increase – not a contraction – in demand for software.

· The US market is rebalancing, particularly in favour of small caps, now penalising the heavy investments made by tech giants in AI

· The sharp fall in the software segment is considered disproportionate. The market is underestimating the diversity of companies in the sector and ignoring Jevons' paradox, according to which lower AI costs will stimulate demand for software.

· In this context, we are increasing our exposure to emerging market and Japanese equities.

It is true that the AI stock market cycle has recently matured and is no longer unambiguous. Announcements of investment plans for 2026 that far exceeded expectations from Alphabet and Amazon were punished by the stock market – a first – and did not have the expected knock-on effect on the stocks that were supposed to benefit. The free cash flows of many hyperscalers are expected to be negative this year, forcing them to resort to debt or share issues to finance their investments – again, a first. These companies, previously perceived as ‘asset light’ and therefore favoured by the stock market, are becoming less and less so, and the market is now beginning to question the profitability of these increasingly massive investments.

However, if there is one theme that has remained constant for months, it is the search for ‘AI victims’. Software companies have recently fallen sharply on the stock market, losing nearly 20% in a few weeks, without any real discrimination, based on the idea that customers will in future be able to turn directly to AI to develop the software they need. However, this movement obscures the diversity of models within the sector, between horizontally and vertically integrated software, whose sensitivity to AI differs greatly.

We therefore continue to favour the broadening theme, considering that AI is overplayed on the producer side but still undervalued on the user side.

We are also increasing our exposure to emerging market equities. After years of underperformance, they seem well placed to benefit from the reweighting towards regions other than the United States as the AI cycle matures, the search for new AI-related stocks (particularly in China), the prospect of Fed rate cuts and rising metal prices (in Latin America).

In Japan, the LDP's landslide victory in the snap general election gives Prime Minister Sanae Takaichi full powers to pursue a reflationary policy, leading us to maintain our overweight position in Japanese equities.

In the bond markets, we favour financial bonds and corporate hybrids (which are mainly investment grade issuers), as well as emerging market bonds. Spreads remain low, but we believe private sector bonds are less exposed to rising public deficits. We also favour short and intermediate maturities, which are more sensitive to monetary policy than fiscal policy.

Indosuez Wealth Management, 19 February 2026

Authors: Cyril Suter, Equity specialist

Critical minerals and base metals are emerging as essential pillars of industrial growth. Their strategic role in the sectors of electrification and energy transition, advanced technologies and defence offers major opportunities, but also raises challenges related to global supply.

Base metals, particularly copper, play a key role in the global energy transition. Often referred to as ‘the metal of electricity’, copper is indispensable thanks to its exceptional conductivity. Today, approximately 45% of copper demand comes from electrification, incl. power grids, electric vehicles (EVs), renewable energy and data centres. This proportion could reach 60% by 2030-35. Total demand for copper could therefore increase significantly, with projections indicating a 70% increase by 2050. Despite this, discoveries of new deposits have declined sharply, and bottlenecks in exploration and extraction threaten to create a structural shortage by 2030. On average, it takes around 18 years for a copper mine to become operational and productive, from exploration and discovery.

Critical minerals, such as rare earths, lithium and cobalt, are essential for strategic sectors such as technology, defence and energy transition. Smartphones, for example, contain up to 130 grams of critical minerals, such as indium for touch screens, lithium for batteries, and rare earths for speaker and microphone magnets.

In the defence sector, rare earths play a major strategic role. Magnets made from neodymium and samarium are essential for military technologies that require reliability and heat resistance. For example, an F-35 fighter jet contains 418 kilograms of rare earths for its electric motors, missiles, and precision guidance systems. With growing demand in the military sector, critical minerals are becoming a key geostrategic issue.

Renewable energies, such as wind and solar power, consume critical minerals on a massive scale, particularly neodymium for turbine magnets. Electric vehicles require six times more minerals than a traditional combustion engine vehicle, with demand for lithium expected to quadruple by 2040.

However, China has overwhelming dominance over the rare earths market, and this dependence creates a major vulnerability for Western countries, which are seeking to diversify their supply chains through strategic alliances, investments in local extraction and recycling technologies.

For investors seeking exposure to critical minerals and rare earths, there are ETFs that offer direct exposure to companies involved in the extraction, refining and production of these strategic minerals, such as lithium and cobalt.

Base metals and critical minerals are at the heart of global economic transformations and major geopolitical issues. Investing in these resources is not only a financial and diversification opportunity for portfolios, but also a strategic commitment to the technological future and energy innovation of tomorrow.

Vontobel, 19 February 2026

Authors: Gregor Kapferer, Head of Swiss Bonds

While the CHF retains some upside potential, any further gains are likely to be limited by the threat of monetary policy action.

The Swiss franc is at a critical turning point in early 2026, shaped by its historical appeal as a safe haven, Switzerland's economic fundamentals and the Swiss National Bank's (SNB) policy developments. The Swiss franc's strong performance in recent quarters is the result of a combination of Switzerland's current account surplus, structurally low inflation and stable economic growth. However, with the currency already close to its multi-year highs, any further appreciation is likely to be gradual and more related to external shocks than domestic factors. The SNB's long-standing commitment to limiting excessive strength in the Swiss franc remains a major risk for investors. Policymakers are particularly sensitive to the pace of appreciation; a rapid and sharp rise in the franc could trigger further intervention through foreign exchange operations or adjustments to key interest rates. These measures are aimed at protecting Swiss export competitiveness and inflation targets. The main risk for the markets is that intervention by the SNB – especially if unexpected – could cause sharp reversals in the franc, increase volatility and undermine confidence in trend-following strategies. Thus, even if the franc retains some potential for appreciation, the threat of intervention acts as a natural brake on speculative positioning.

Gold price movements have a limited direct influence on the Swiss franc

Despite Switzerland's important role in global gold trading, fluctuations in the price of gold have only a limited impact on the Swiss franc. The Swiss gold export industry mainly consists of refining and re-exporting imported gold, which is generally denominated in USD. As a result, fluctuations in the price of gold mainly affect trade flows and revenues, but have little impact on demand for the CHF. The value of the franc depends primarily on macroeconomic fundamentals and investor sentiment, rather than on commodity cycles, including gold.

Safe-haven status and stability of central bank reserves

The CHF's enduring status as a safe-haven currency is based on Switzerland's political stability, sound fiscal management and strong external surpluses. In times of global tension, investors regularly seek the security offered by the franc, which contributes to its resilience. However, even though central banks recognise the CHF's safe-haven qualities, their reserve allocations to the currency remain stable and relatively modest. This is due to practical constraints: the limited depth and liquidity of the Swiss financial market make it difficult to accumulate reserves on a large scale, unlike the USD or the EUR. As a result, the franc's share of official reserves remains stable, serving as a diversification tool rather than a core reserve asset.

In summary, the outlook for the Swiss franc in 2026 is shaped by a delicate interplay between solid fundamentals, the risk of SNB intervention and its established reputation as a safe haven.

Equities

Q4 earnings weekly performances:

Analog Dev. (+8%), Warner Bros (+2%), BAE Sys (+10%), Danone (+2%)

Walmart (-8%), Nexans (-8%), Airbus (-2%), Rio Tinto (-3%)

NB: Eramet (-18%), Moncler (+12%), Bayer (-5%)

Bank analysts: Siemens Energy (GS ‘buy’ target €185), Anheuser Inbev (MS ‘o/w’ target €74), Arcelormittal (MS ‘o/w’ target 54€)

Rates

US curve steepening (2-10 years) lower at +60bps (-4bps)

HY corp. spreads lower: US at +288bps (-5bps); EU stable at +262bps

Commodities

Oil price higher (+5.5%) due to US military presence around Hormuz strait

Gold price higher (+1.5%) despite a stronger USD

US

Dec Core PCE at +3% vs +2.8% prior; Q4 GDP at +1.4% vs +4.4% in Q3

Crypto

BTC (-2.5%) the 5th consecutive negative week; SOL (-4%) ; XRP (-6%)

Under the watch

FED injected $18bn into the US banking system last week (via o/n repo)

$10trn of US gov. debts are to be refinanced over the next 12 months

Lagarde said to leave much before Oct 2027 (end of her mandate)

Nota Bene

End of Buyback blackout window (for 80% of the SP500 corporates)

SWE bench (repair evaluations) new DeepSeek V4 expected at 83.7% vs Claude at 80.9% GPT 80% Gemini 76% and DeepSeek V3 at 73%

ECB to provide euro liquidity to broad set of CBs vs high quality euro denominated collateral (Q3 2026)

CALENDAR

Earnings releases :

US Home Depot (24 Feb), Nvidia (25), Salesforce (26)

EU HSBC (25 Feb), Schneider Elec, Allianz (26), BASF, Swiss Re, Holcim (27)

Macro data releases:

US Jan PPI (27)

WHAT ANALYSTS SAY

- Edmond de Rothschild: Market rotation offer attractive opportunities

- Indosuez: Investing in the resourses of the future

- Vontobel: CHF between safe haven appeal, SNB risks and reserve role

Edmond de Rothschild AM, 20 February 2026

Author: Benjamin Melman, Global Chief Investment Officer

Improvements in software efficiency and lower AI-related costs should lead to an increase – not a contraction – in demand for software.

· The US market is rebalancing, particularly in favour of small caps, now penalising the heavy investments made by tech giants in AI

· The sharp fall in the software segment is considered disproportionate. The market is underestimating the diversity of companies in the sector and ignoring Jevons' paradox, according to which lower AI costs will stimulate demand for software.

· In this context, we are increasing our exposure to emerging market and Japanese equities.

It is true that the AI stock market cycle has recently matured and is no longer unambiguous. Announcements of investment plans for 2026 that far exceeded expectations from Alphabet and Amazon were punished by the stock market – a first – and did not have the expected knock-on effect on the stocks that were supposed to benefit. The free cash flows of many hyperscalers are expected to be negative this year, forcing them to resort to debt or share issues to finance their investments – again, a first. These companies, previously perceived as ‘asset light’ and therefore favoured by the stock market, are becoming less and less so, and the market is now beginning to question the profitability of these increasingly massive investments.

However, if there is one theme that has remained constant for months, it is the search for ‘AI victims’. Software companies have recently fallen sharply on the stock market, losing nearly 20% in a few weeks, without any real discrimination, based on the idea that customers will in future be able to turn directly to AI to develop the software they need. However, this movement obscures the diversity of models within the sector, between horizontally and vertically integrated software, whose sensitivity to AI differs greatly.

We therefore continue to favour the broadening theme, considering that AI is overplayed on the producer side but still undervalued on the user side.

We are also increasing our exposure to emerging market equities. After years of underperformance, they seem well placed to benefit from the reweighting towards regions other than the United States as the AI cycle matures, the search for new AI-related stocks (particularly in China), the prospect of Fed rate cuts and rising metal prices (in Latin America).

In Japan, the LDP's landslide victory in the snap general election gives Prime Minister Sanae Takaichi full powers to pursue a reflationary policy, leading us to maintain our overweight position in Japanese equities.

In the bond markets, we favour financial bonds and corporate hybrids (which are mainly investment grade issuers), as well as emerging market bonds. Spreads remain low, but we believe private sector bonds are less exposed to rising public deficits. We also favour short and intermediate maturities, which are more sensitive to monetary policy than fiscal policy.

Indosuez Wealth Management, 19 February 2026

Authors: Cyril Suter, Equity specialist

Critical minerals and base metals are emerging as essential pillars of industrial growth. Their strategic role in the sectors of electrification and energy transition, advanced technologies and defence offers major opportunities, but also raises challenges related to global supply.

Base metals, particularly copper, play a key role in the global energy transition. Often referred to as ‘the metal of electricity’, copper is indispensable thanks to its exceptional conductivity. Today, approximately 45% of copper demand comes from electrification, incl. power grids, electric vehicles (EVs), renewable energy and data centres. This proportion could reach 60% by 2030-35. Total demand for copper could therefore increase significantly, with projections indicating a 70% increase by 2050. Despite this, discoveries of new deposits have declined sharply, and bottlenecks in exploration and extraction threaten to create a structural shortage by 2030. On average, it takes around 18 years for a copper mine to become operational and productive, from exploration and discovery.

Critical minerals, such as rare earths, lithium and cobalt, are essential for strategic sectors such as technology, defence and energy transition. Smartphones, for example, contain up to 130 grams of critical minerals, such as indium for touch screens, lithium for batteries, and rare earths for speaker and microphone magnets.

In the defence sector, rare earths play a major strategic role. Magnets made from neodymium and samarium are essential for military technologies that require reliability and heat resistance. For example, an F-35 fighter jet contains 418 kilograms of rare earths for its electric motors, missiles, and precision guidance systems. With growing demand in the military sector, critical minerals are becoming a key geostrategic issue.

Renewable energies, such as wind and solar power, consume critical minerals on a massive scale, particularly neodymium for turbine magnets. Electric vehicles require six times more minerals than a traditional combustion engine vehicle, with demand for lithium expected to quadruple by 2040.

However, China has overwhelming dominance over the rare earths market, and this dependence creates a major vulnerability for Western countries, which are seeking to diversify their supply chains through strategic alliances, investments in local extraction and recycling technologies.

For investors seeking exposure to critical minerals and rare earths, there are ETFs that offer direct exposure to companies involved in the extraction, refining and production of these strategic minerals, such as lithium and cobalt.

Base metals and critical minerals are at the heart of global economic transformations and major geopolitical issues. Investing in these resources is not only a financial and diversification opportunity for portfolios, but also a strategic commitment to the technological future and energy innovation of tomorrow.

Vontobel, 19 February 2026

Authors: Gregor Kapferer, Head of Swiss Bonds

While the CHF retains some upside potential, any further gains are likely to be limited by the threat of monetary policy action.

The Swiss franc is at a critical turning point in early 2026, shaped by its historical appeal as a safe haven, Switzerland's economic fundamentals and the Swiss National Bank's (SNB) policy developments. The Swiss franc's strong performance in recent quarters is the result of a combination of Switzerland's current account surplus, structurally low inflation and stable economic growth. However, with the currency already close to its multi-year highs, any further appreciation is likely to be gradual and more related to external shocks than domestic factors. The SNB's long-standing commitment to limiting excessive strength in the Swiss franc remains a major risk for investors. Policymakers are particularly sensitive to the pace of appreciation; a rapid and sharp rise in the franc could trigger further intervention through foreign exchange operations or adjustments to key interest rates. These measures are aimed at protecting Swiss export competitiveness and inflation targets. The main risk for the markets is that intervention by the SNB – especially if unexpected – could cause sharp reversals in the franc, increase volatility and undermine confidence in trend-following strategies. Thus, even if the franc retains some potential for appreciation, the threat of intervention acts as a natural brake on speculative positioning.

Gold price movements have a limited direct influence on the Swiss franc

Despite Switzerland's important role in global gold trading, fluctuations in the price of gold have only a limited impact on the Swiss franc. The Swiss gold export industry mainly consists of refining and re-exporting imported gold, which is generally denominated in USD. As a result, fluctuations in the price of gold mainly affect trade flows and revenues, but have little impact on demand for the CHF. The value of the franc depends primarily on macroeconomic fundamentals and investor sentiment, rather than on commodity cycles, including gold.

Safe-haven status and stability of central bank reserves

The CHF's enduring status as a safe-haven currency is based on Switzerland's political stability, sound fiscal management and strong external surpluses. In times of global tension, investors regularly seek the security offered by the franc, which contributes to its resilience. However, even though central banks recognise the CHF's safe-haven qualities, their reserve allocations to the currency remain stable and relatively modest. This is due to practical constraints: the limited depth and liquidity of the Swiss financial market make it difficult to accumulate reserves on a large scale, unlike the USD or the EUR. As a result, the franc's share of official reserves remains stable, serving as a diversification tool rather than a core reserve asset.

In summary, the outlook for the Swiss franc in 2026 is shaped by a delicate interplay between solid fundamentals, the risk of SNB intervention and its established reputation as a safe haven.

Contacts

8 Kievyan Street, Yerevan, Armenia

+374 10 712 259

+374 43 004 182

unibankinvest@unibank.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.