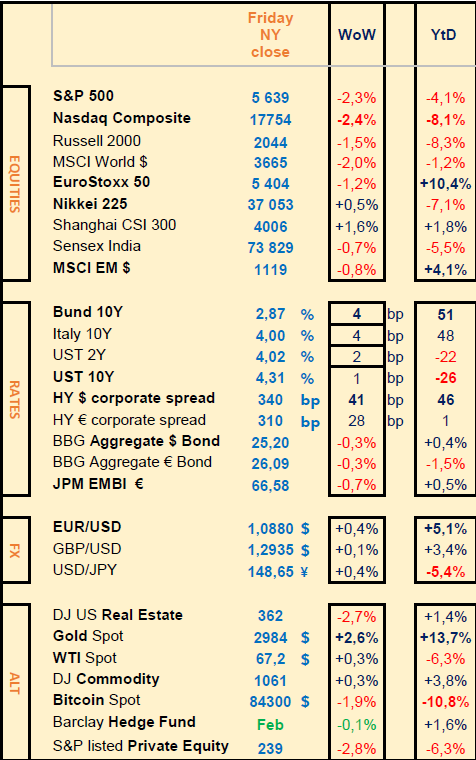

Last week: Fears of US recession and trade war inflation led to further US equities sell-off, Gold broke the $3000 mark

WEEKLY TRENDS

WEEKLY TRENDS

- The ninth week of Q4 earnings releases, was once again disrupted by new trade tariffs being implemented in retaliation

- Technically the US equities indices remain on a downtrend, keeping well below their 200 day moving averages but a resurgent Friday has potentially given some air and most likely avoided another 10% sell-off next week

- Some Q4 earnings releases were good (Rheinmetall, Charles Schwab, Enel) while some were not (Adobe, Swiss Life, BMW and VW)

- The US debt ceiling remains an issue with a near accord between Dems and Reps that should avoid a US government shutdown

- US inflation in February was released lower (PPI at +3.2% vs 3.7% in Jan and CPI at +2.8% vs 3.0% in Jan)

- Late Friday, Fitch maintained its negative watch on France’s LT debt and kept a AA-rating

- This coming week will see 5 central banks decide on their base rates (FED, BOJ, BOE, SNB and BACEN)

MARKETS

Equities

Q4 earnings released (weekly stock performance):

Rheinmetall (+20%), Charles Schwab (+6%), Enel (+3%)

Adobe (-10%), Swiss Life (-3%), BMW (-3%), VW (-2%), Oracle (-1%)

NB: Kering is down –10% after nomination of new creation director at Gucci; Intel is up +16% on nomination of new General Director

Analysts:

Thales (DB ‘buy’ target €265); Sandoz (Bernstein ’o/w’ target CHF52); Spie (BNP & JPM ’o/w’ target €46); Galderma (Jefferies ’buy’ target CHF115); Air France (JPM ’o/w’ target €15)

GSK (Oddo ’neutral’ target £17); Novartis (Oddo ’neutral’ target CHF110); Holcim (Citi ’neutral’ target CHF109); Hensoldt (Kepler ’hold’ target €52); Alstom (Citi ’neutral’ target €26)

Rates

US curve (2-10 years) steepening unchanged at 30bps. Long Bond yields slightly higher especially in the EU

HY corporate spreads higher across the board

Commodities

Oil price unchanged (Macquarie foresees Gold at $3500 in Q3 2025)

Gold price higher (+2.5% on tariffs chaos and possible renewed inflation)

US

Feb CPI released at +2.8% YoY vs 3.0% in Jan; Feb PPI released at +3.2% YoY vs 3.7% in Jan

Cryptos

$900m ETF outflows last week ($90bn outstanding vs $120bn in Jan); NB: SEC accepted Bitwise $DOGE ETF’s application (decision 4 Apr)

Under the watch

US stocks indices 200 day MA (5740 SP500; 18420 Nasdaq Composite)

Nota Bene

GS Chief economist revised down his forecast for 2025 US GDP growth at 1.7% vs 2.4% prior and raised his PCE forecast to 3% vs 2.4% prior

CALENDAR

Q4 Corporate earnings:

US: Accenture, Nike, Micron Tech, Fedex (20 March)

EU: Bolloré, ADP (17 March), Vinci, Audi (18), Prudential (19)

Central Bank committees: FED, BOJ, BACEN (19 March), BOE, SNB (20)

WHAT ANALYSTS SAY

Amundi Investment Institute, 11 March 2025

Authors: Monica Defend, Head of Amundi Investment Institute & Chief Strategist; Vincent Mortier, Group Chief Investment Officer

· After recent moves, our expectations for markets

As we have seen, gains from the "Trump trade" have been entirely reversed, highlighted by a significant underperformance of US stocks and the powerful rotation taking place. Despite this, some parts of the US equity market remain overvalued, and the correction is likely to continue in these areas.

European equity markets have come a long way in a very short time, and we could now see some stabilisation around current levels. A pull-back at this point could present opportunities from a long-term perspective. The case for a relative preference for Europe vs the US remains intact, as valuations are more appealing and the fiscal push could support earnings dynamics.

In Asia, Chinese stocks have risen on the back of technology announcements, with internet, autos and telecoms leading the gains. The upside in China may be coming at the expense of US companies and, indeed, if the advance in Chinese tech continues, multiples in the US could come under pressure. Therefore, we could witness a continuation of the current rotation out of the US and into European equities.

On the fixed income side, recent market movements confirm the need to maintain an active duration approach. In our view, the very sharp rise in German yields may present a short-term opportunity, but the supply outlook has clearly changed. Bunds are likely to continue to underperform peripheral markets. Although we think the ECB will cut rates down to 1.75% this year, given the weakness of current growth, yield curves could steepen further due to supply and an improving medium-term growth outlook.

In contrast, US yields have fallen sharply, particularly at the front end of the curve. 2y US yields could fall further towards 3.75%, which is where we expect Fed Funds rates to bottom this year. But 10y yields are more likely to rise than fall from current 4.20% levels, given their high supply and despite the slowing economic growth outlook. As a result, yield curves could continue to steepen between the 2y and 10y.

Finally, in corporate credit, we remain constructive on European investment grade credit, with financials in particular likely to see further spread tightening.

Moving to the dollar, it is selling off despite high US inflation, risks to global trade from tariffs, and underperforming US equities. While uncertainty remains, we believe the current trend is backed by two key factors that inform our bearish outlook for the USD in 2025.

1. Loss of safe haven status: historical analysis of correlation dynamics (since 2020) shows that the USD loses its safe haven status when stock market corrections are driven by "lower growth" rather than "higher inflation". We believe this will be the environment moving forward in 2025 as economic risks are tilted towards the downside.

2. Improving sentiment outside the US: Sentiment outside the US is improving amid increased EU spending, a potential ceasefire in Ukraine and lower energy prices. This further challenges the strength of the USD. However, the lack of execution details on the German fiscal package and uncertainty regarding its growth impact are factors to watch, as they could increase volatility ahead.

While some good news may already be priced in (with the euro already approaching our original target of 1.10 by the end of 2025), high USD positioning and valuation, along with the potential for a bull steepening of the US yield curve, indicate that the USD has room for a correction.

Overall, we think it is important to maintain a flexible and vigilant stance on duration as yields could move fast in a short period of time. Select government bonds, along with commodities such as gold, also offer diversification during economic and geopolitical uncertainty. At the same time, for risk assets, investors should consider rotation opportunities outside of expensive segments towards attractively priced areas that still offer robust earnings prospects. Thus, a well-balanced stance is crucial at this stage.

Trump’s activism on the US economy is creating fears of recession. To navigate short-term turbulence, we have tactically scaled back our exposure to macro-sensitive assets, such as US equities, including US midcaps, along with high-yield and emerging-market debt, while increasing our allocation to gold.

UBP House View, 13 March 2025

Author: Michael Lok, Group CIO & Co-CEO Asset Management

Trump’s activism on the US economy is creating fears of recession. To navigate short-term turbulence, we have tactically scaled back our exposure to macro-sensitive assets, such as US equities, including US midcaps, along with high-yield and emerging-market debt, while increasing our allocation to gold.

Key Takeaways :

· Tactical implementation of a risk management strategy in portfolios

· Reduced exposure to macro-sensitive risk assets such as US equities, incl. midcaps, along with high-yield and emerging-market debt

· Ongoing preference for gold and hedge funds to navigate the current turmoil

· Attractive opportunities likely to arise in the US tech sector.

Managing risk against a turbulent geopolitical backdrop

Donald Trump’s second non-consecutive term in office has begun with a bang, as the 47th US president has set out to reshape not only the architecture of global trade via an aggressive tariff policy, continuing the work he began in his first term, but also to reframe America’s security relationship with its European allies.

The combination of the two has triggered wide swings in volatility since Trump’s November 2024 election, as anticipated in our 2025 Investment Outlook. In preparation for this, we built a strong foundation of assets that can weather such volatility and, in some cases, shield investors from it.

Gold, as we highlighted as far back as 2023, remains a key anchor for preserving clients’ inflation-adjusted wealth as this new era unfolds. Indeed, despite volatility seen for both equity markets and bond yields since Donald Trump’s re-election, gold has delivered a 6% return, outpacing both global bonds and equities amid the tumult.

Even though gold has already seen a strong rally, we continue to expect the yellow metal to head for USD 3,300 as inflation rebounds in the months ahead, driven by not only American tariff policy but also Germany’s historic fiscal expansion. As a result, investors have further opportunities to increase existing positions on gold.

The return of relatively flat yield curves – with short- and long-dated bonds offering similar yields – means that investors are continuing to benefit from low levels of long-term interest-rate risk, while favouring cash and short-dated maturities due to high bond volatility. While credit risk was beneficial for investors at a time of strong economic growth, tariff uncertainty is starting to challenge the historically tight spreads currently seen in credit markets.

As a result, it could be beneficial for investors to look at alternative fixed-income strategies, as noted in our 2025 Investment Outlook. These strategies in the hedge fund space offer investors an avenue to side- step interest-rate volatility and manage and capitalise on credit-spread volatility more proactively, while still replicating the returns achieved by more traditional investment-grade bond portfolios.

Indeed, amid the Trump-driven volatility seen since the end of October 2024, alternative fixed-income strategies, such as relative value fixed-income arbitrage, have delivered returns in excess of their investment-grade counterparts.

Investors can use these anchors as the foundation of their portfolios, protecting them against periodic volatility surges across both bond and equity markets, which we expect to occur frequently given the current US president’s attempts to reshape the global landscape. Investors can then overlay more tactical strategies in response to events as they unfold, in order to calibrate exposures to match the rapidly changing landscape.

Equities

Q4 earnings released (weekly stock performance):

Rheinmetall (+20%), Charles Schwab (+6%), Enel (+3%)

Adobe (-10%), Swiss Life (-3%), BMW (-3%), VW (-2%), Oracle (-1%)

NB: Kering is down –10% after nomination of new creation director at Gucci; Intel is up +16% on nomination of new General Director

Analysts:

Thales (DB ‘buy’ target €265); Sandoz (Bernstein ’o/w’ target CHF52); Spie (BNP & JPM ’o/w’ target €46); Galderma (Jefferies ’buy’ target CHF115); Air France (JPM ’o/w’ target €15)

GSK (Oddo ’neutral’ target £17); Novartis (Oddo ’neutral’ target CHF110); Holcim (Citi ’neutral’ target CHF109); Hensoldt (Kepler ’hold’ target €52); Alstom (Citi ’neutral’ target €26)

Rates

US curve (2-10 years) steepening unchanged at 30bps. Long Bond yields slightly higher especially in the EU

HY corporate spreads higher across the board

Commodities

Oil price unchanged (Macquarie foresees Gold at $3500 in Q3 2025)

Gold price higher (+2.5% on tariffs chaos and possible renewed inflation)

US

Feb CPI released at +2.8% YoY vs 3.0% in Jan; Feb PPI released at +3.2% YoY vs 3.7% in Jan

Cryptos

$900m ETF outflows last week ($90bn outstanding vs $120bn in Jan); NB: SEC accepted Bitwise $DOGE ETF’s application (decision 4 Apr)

Under the watch

US stocks indices 200 day MA (5740 SP500; 18420 Nasdaq Composite)

Nota Bene

GS Chief economist revised down his forecast for 2025 US GDP growth at 1.7% vs 2.4% prior and raised his PCE forecast to 3% vs 2.4% prior

CALENDAR

Q4 Corporate earnings:

US: Accenture, Nike, Micron Tech, Fedex (20 March)

EU: Bolloré, ADP (17 March), Vinci, Audi (18), Prudential (19)

Central Bank committees: FED, BOJ, BACEN (19 March), BOE, SNB (20)

WHAT ANALYSTS SAY

- Amundi Investment Institute - Tariffs and European news fuel volatility

- UBP House View - March 2025

Amundi Investment Institute, 11 March 2025

Authors: Monica Defend, Head of Amundi Investment Institute & Chief Strategist; Vincent Mortier, Group Chief Investment Officer

· After recent moves, our expectations for markets

As we have seen, gains from the "Trump trade" have been entirely reversed, highlighted by a significant underperformance of US stocks and the powerful rotation taking place. Despite this, some parts of the US equity market remain overvalued, and the correction is likely to continue in these areas.

European equity markets have come a long way in a very short time, and we could now see some stabilisation around current levels. A pull-back at this point could present opportunities from a long-term perspective. The case for a relative preference for Europe vs the US remains intact, as valuations are more appealing and the fiscal push could support earnings dynamics.

In Asia, Chinese stocks have risen on the back of technology announcements, with internet, autos and telecoms leading the gains. The upside in China may be coming at the expense of US companies and, indeed, if the advance in Chinese tech continues, multiples in the US could come under pressure. Therefore, we could witness a continuation of the current rotation out of the US and into European equities.

On the fixed income side, recent market movements confirm the need to maintain an active duration approach. In our view, the very sharp rise in German yields may present a short-term opportunity, but the supply outlook has clearly changed. Bunds are likely to continue to underperform peripheral markets. Although we think the ECB will cut rates down to 1.75% this year, given the weakness of current growth, yield curves could steepen further due to supply and an improving medium-term growth outlook.

In contrast, US yields have fallen sharply, particularly at the front end of the curve. 2y US yields could fall further towards 3.75%, which is where we expect Fed Funds rates to bottom this year. But 10y yields are more likely to rise than fall from current 4.20% levels, given their high supply and despite the slowing economic growth outlook. As a result, yield curves could continue to steepen between the 2y and 10y.

Finally, in corporate credit, we remain constructive on European investment grade credit, with financials in particular likely to see further spread tightening.

Moving to the dollar, it is selling off despite high US inflation, risks to global trade from tariffs, and underperforming US equities. While uncertainty remains, we believe the current trend is backed by two key factors that inform our bearish outlook for the USD in 2025.

1. Loss of safe haven status: historical analysis of correlation dynamics (since 2020) shows that the USD loses its safe haven status when stock market corrections are driven by "lower growth" rather than "higher inflation". We believe this will be the environment moving forward in 2025 as economic risks are tilted towards the downside.

2. Improving sentiment outside the US: Sentiment outside the US is improving amid increased EU spending, a potential ceasefire in Ukraine and lower energy prices. This further challenges the strength of the USD. However, the lack of execution details on the German fiscal package and uncertainty regarding its growth impact are factors to watch, as they could increase volatility ahead.

While some good news may already be priced in (with the euro already approaching our original target of 1.10 by the end of 2025), high USD positioning and valuation, along with the potential for a bull steepening of the US yield curve, indicate that the USD has room for a correction.

Overall, we think it is important to maintain a flexible and vigilant stance on duration as yields could move fast in a short period of time. Select government bonds, along with commodities such as gold, also offer diversification during economic and geopolitical uncertainty. At the same time, for risk assets, investors should consider rotation opportunities outside of expensive segments towards attractively priced areas that still offer robust earnings prospects. Thus, a well-balanced stance is crucial at this stage.

Trump’s activism on the US economy is creating fears of recession. To navigate short-term turbulence, we have tactically scaled back our exposure to macro-sensitive assets, such as US equities, including US midcaps, along with high-yield and emerging-market debt, while increasing our allocation to gold.

UBP House View, 13 March 2025

Author: Michael Lok, Group CIO & Co-CEO Asset Management

Trump’s activism on the US economy is creating fears of recession. To navigate short-term turbulence, we have tactically scaled back our exposure to macro-sensitive assets, such as US equities, including US midcaps, along with high-yield and emerging-market debt, while increasing our allocation to gold.

Key Takeaways :

· Tactical implementation of a risk management strategy in portfolios

· Reduced exposure to macro-sensitive risk assets such as US equities, incl. midcaps, along with high-yield and emerging-market debt

· Ongoing preference for gold and hedge funds to navigate the current turmoil

· Attractive opportunities likely to arise in the US tech sector.

Managing risk against a turbulent geopolitical backdrop

Donald Trump’s second non-consecutive term in office has begun with a bang, as the 47th US president has set out to reshape not only the architecture of global trade via an aggressive tariff policy, continuing the work he began in his first term, but also to reframe America’s security relationship with its European allies.

The combination of the two has triggered wide swings in volatility since Trump’s November 2024 election, as anticipated in our 2025 Investment Outlook. In preparation for this, we built a strong foundation of assets that can weather such volatility and, in some cases, shield investors from it.

Gold, as we highlighted as far back as 2023, remains a key anchor for preserving clients’ inflation-adjusted wealth as this new era unfolds. Indeed, despite volatility seen for both equity markets and bond yields since Donald Trump’s re-election, gold has delivered a 6% return, outpacing both global bonds and equities amid the tumult.

Even though gold has already seen a strong rally, we continue to expect the yellow metal to head for USD 3,300 as inflation rebounds in the months ahead, driven by not only American tariff policy but also Germany’s historic fiscal expansion. As a result, investors have further opportunities to increase existing positions on gold.

The return of relatively flat yield curves – with short- and long-dated bonds offering similar yields – means that investors are continuing to benefit from low levels of long-term interest-rate risk, while favouring cash and short-dated maturities due to high bond volatility. While credit risk was beneficial for investors at a time of strong economic growth, tariff uncertainty is starting to challenge the historically tight spreads currently seen in credit markets.

As a result, it could be beneficial for investors to look at alternative fixed-income strategies, as noted in our 2025 Investment Outlook. These strategies in the hedge fund space offer investors an avenue to side- step interest-rate volatility and manage and capitalise on credit-spread volatility more proactively, while still replicating the returns achieved by more traditional investment-grade bond portfolios.

Indeed, amid the Trump-driven volatility seen since the end of October 2024, alternative fixed-income strategies, such as relative value fixed-income arbitrage, have delivered returns in excess of their investment-grade counterparts.

Investors can use these anchors as the foundation of their portfolios, protecting them against periodic volatility surges across both bond and equity markets, which we expect to occur frequently given the current US president’s attempts to reshape the global landscape. Investors can then overlay more tactical strategies in response to events as they unfold, in order to calibrate exposures to match the rapidly changing landscape.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+374 43 00-43-82

Broker

broker@unibankinvest.am

research@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.