Last week: Fitch upgraded Italy to BBB+; US stocks hit new records on FED’s well expected -25bps rate cut decision

WEEKLY TRENDS

WEEKLY TRENDS

- Late Friday Fitch rating agency upgraded Italy long term debt rating to single BBB+ vs BBB prior, citing improved fiscal resilience and spending restraint

- The FOMC/FED did cut rates as expected by -25bps (4-4.25%), with most likely 2 more cuts this year (J. Powell pivoting towards a job market focus). The MPC/BOE kept its base rate unchanged at 4% (UK CPI for August came out as expected at 2.9% p.a.). The BOJ kept also its rate unchanged at 0.5% after PM Ishiba’s resignation and among the new political uncertainty

- Trump’s visit to the UK brought $200bn worth of US investment planned to the UK

- And last but not least for last week, Intel jumped by 22% after Nvidia decided to inject $5bn worth of capital equity into the US chip manufacturer (planning new chips x86 together)

- This coming week, on Monday 22nd, there shall be an S&P index rebalancing with new entrants being AppLovin, Robinhood, Emcor Group and leaving the index, Enphase Energy, Caesars entertainment, MarketAxess while UBER will join the S&P100 instead of Charter Communications. Investors will focus on the US August PCE inflation data to be released on Friday

MARKETS

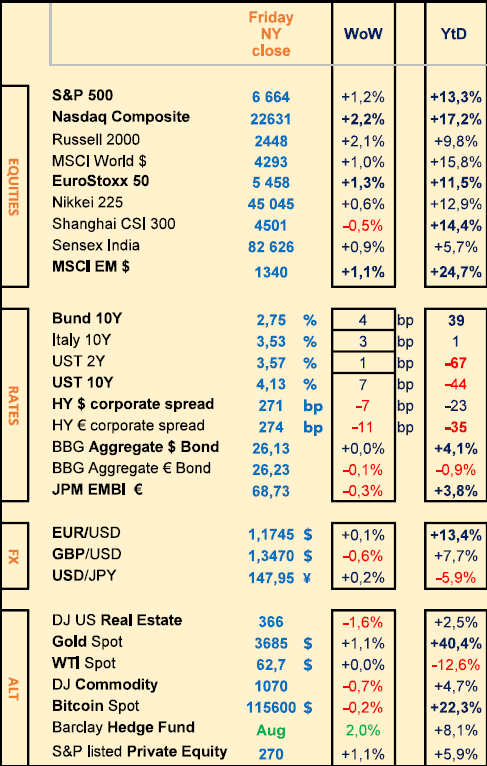

Equities

Specific stock weekly performances:

Intel (+22% on Nvidia $5bn capital injection for 4% equity), US Oklo (+63% on strong demand for nuclear fuel), Kering (+11%), Novo Nordisk (+11%)

Orsted (-47% on poor outlook, is to raise $9.5bn equity capital), SIG (-31% on poor outlook), Bolloré (-4%) Vinci (-1%)

M&A:

Roche is to buy US 89Bio (+84%) for $3.5bn; Puma (+13%) Authentic Brands and CVC are said to be interested in 29% equity from Pinault

Analysts: Airbus (RBC ‘o/w’ target €220), Dassault Aviation (JPM ‘neutral’ target €325), Solvay (MS ‘u/w’ target €25)

Rates

US curve (2-10 years) steepening slightly up at 55bps (+5)

HY corporate spreads lower -10bps (US at 270bps; EU at 275bps)

Commodities

Oil price unchanged

Gold price higher (+1%) new ATH at $3705 an ounce (on FED cut)

Silver YTD performance is at +48%, while Platinum is at +53%

UK

Aug CPI at +3.8% unchanged (Core at 3.6%) CPIH at 4.1% (Core at 4%)

Crypto

BTC unchanged

Under the watch

France debt rating reviews (Moody’s 24 Oct; S&P 28 Nov)

US budget and fiscal situation (Oct 14 US court decision over tariffs)

Nota Bene

Elon Musk bought for $1bn worth of Tesla shares last Monday

The South Korean stock index (Kospi) shows a YTD performance at +45%; Spain’s IBEX at +30% and Poland’s WIG at +25%

CALENDAR

Earnings releases :

US Micron (23 Sep), EU H&M (25 Sep)

Macro releases :

US August PCE inflation (26 Sep)

WHAT ANALYSTS SAY

Lazard Asset, 19 September 2025

Author: Bertrand Cliquet, Portfolio Manager

As part of our strategy, infrastructure investments provide significant diversification for investors. There are listed companies active in infrastructure that have very different cash flow dynamics, distinct specialisations and low correlation with economic conditions. We focus on what are known as ‘preferred infrastructure’ companies. These are companies that are characterised by a high degree of predictability in terms of future cash flow trends. These companies enjoy a form of monopoly, are able to pass on price increases, operate within proven regulatory frameworks and offer legal recourse. It is indeed very important to have a reliable regulatory environment.

Unlike certain other sectors of activity in which companies can choose their production locations, it is not generally possible to relocate infrastructure-related activities. For example, it is not possible to move the operation of electricity grids or motorway tolls.

Firstly, there is the energy sector, which includes utilities, network equipment used for electricity transmission, and companies that manage water networks, particularly in the United Kingdom and Italy. The second sector is transport. This includes companies that operate airports and motorways. The third sector consists of companies active in telecommunications.

The decisive criterion is the essential nature of the services. Companies that operate electricity, water and gas networks are very little exposed to volume fluctuations. It would take a very severe recession for people to reduce their water consumption, for example. By comparison, the revenues of companies that operate motorway tolls are not completely unrelated to the economic climate, but the variations are much smaller than for other companies active in the transport sector. The risks are therefore limited, even in the event of a recession.

In addition, some concession agreements provide for mechanisms to adjust tariffs based on volumes. This makes margin and cash flow trends more predictable.

As an investor, it is important to pay close attention to the prices paid for assets. This is because assets do not change, or change very little, over time. It is not like in the technology sector, for example, where companies and their results evolve very quickly. The entry point is an essential aspect when investing in infrastructure. That is why it is also important to be wary of trends that are considered most attractive at certain times. A few years ago, it was essential to have investments in renewable energy. This resulted in stratospheric valuations around 2023. In 2024, the trend reversed. Over the past two years, we have seen prices for certain assets fall by up to 60%. This means that price declines are possible even when nothing has happened technically or operationally.

Lower interest rates have not always had the same impact on infrastructure investments on both sides of the Atlantic. In the United States, utility companies have generally benefited from lower interest rates. In Europe, however, returns on invested capital have increased in line with the rise in interest rates in recent years. It can therefore be observed that interest rates have less of an impact on returns in Europe than in the United States. At the same time, regulatory authorities also take interest rate levels into account – if rates fall sharply, they may also want consumers to benefit from lower financing costs.

Infrastructure companies in a monopoly position are subject to a regulatory framework that allows them to pass on the costs of purchasing materials in their tariffs. Thus, if companies were to import electrical transmission cables or transformers, for example, customs duties would be passed on to the consumer. Furthermore, there are so many investment opportunities, ranging from the renewal of ageing assets to the connection of data centres, that we see little risk to these companies' organic growth prospects.

It is important to consider the total return obtained, not just the nominal amount of dividends received. In infrastructure, dividend yields are generally higher than the market average.

Digital Asset Solutions, 19 September 2025

Author: Leon Curti, Head of Research

XRP, Ripple's flagship product, On-Demand Liquidity (ODL), enables real-time payments. Banks exchange their currency for XRP, transfer it to the destination country and convert it back locally, without the need for costly foreign currency accounts. This reduces capital tie-up and costs. ODL is considered the most important application of XRP, but is only available in a few corridors. In the second quarter of 2025, the transaction volume amounted to USD 1.3 billion. By comparison, stablecoins such as USDT and USDC process nearly USD 3 trillion per month.

Since 2020, Ripple had been involved in costly litigation with the SEC, the US financial markets regulator, which considered XRP to be an unregistered security. This also hampered institutional partnerships. It was not until 2025 that the tide turned: the SEC closed the case, confirming that XRP is not considered a security in public trading. During the same quarter, trading volume increased significantly, despite a decline in the number of new retail addresses. Thus, in the first quarter of 2025, the XRP ledger processed approximately two million transactions per day and was among the most active blockchains. Three-quarters of all transactions were confirmed in less than five seconds, which is ideal for high-frequency, low-margin payments. The number of active accounts continued to increase, reaching approximately 130,000 per day.

In addition, Ripple has applied for a national banking licence from the US Office of the Comptroller of the Currency (OCC) and is seeking to obtain a master account with the Federal Reserve in order to have direct access to the US payment system. In Europe, expansion is being driven by Ripple Payments Europe SA in Luxembourg, where an EMI licence has been applied for in order to introduce the RLUSD stablecoin in a regulated manner throughout the EEA.

At the same time, XRP is gaining ground in the US financial markets. Asset managers such as Grayscale and WisdomTree have filed applications with the SEC for spot ETF authorisation. If approved, XRP would be the next major cryptocurrency to offer a US spot ETF, after Bitcoin and Ethereum. The outlook is currently considered good. Such a product could significantly facilitate institutional capital inflows into XRP.

From an investor perspective, the picture is mixed.

On the one hand, regulatory clarity, the growing importance of stablecoins, possible ETF approvals and numerous institutional partnerships point to upside potential. On the other hand, on-chain usage by banks and payment service providers remains limited.

Established stablecoins such as USDT and USDC, as well as potential central bank digital currencies (CBDCs), limit the scope of application, while high volatility remains a barrier to payment transactions. Demand for XRP is also limited, as the token is not essential to the core business.

The high market capitalisation is therefore heavily dependent on marketing, networking and acquisitions, while the concentration of tokens in Ripple and its founders – nearly 40% of the total tokens – creates pressure for future sales.

In addition, the possibility of an initial public offering (IPO) of Ripple, which has been mentioned repeatedly, creates uncertainty. For investors, this means that XRP remains a speculative asset, offering opportunities but also risks. Consequently, it may be wise to adjust one's positioning according to one's risk appetite or to determine it by market weighting.

Indosuez/DPAM, 19 September 2025

Author: Ewout de Brauwer, Portfolio Manager

Until now, the stablecoin landscape has resembled a patchwork of regulations, major issuers such as Circle and Paxos operated within the New York regulatory framework, while others benefited from less stringent state licences. The market was operating in a legal grey area, which has now been cleared up thanks to the creation of the category of federally authorised stablecoin issuers (PPSIs) defined by the GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins Act, July 2025). This category includes bank subsidiaries, federally chartered non-banks supervised by the Office of the Comptroller of the Currency (OCC), and state-approved issuers whose stablecoin assets are less than $10bn (above this threshold, they must cease operations or come under federal supervision).

The Act also requires each stablecoin to be backed by a high-quality liquid asset (cash, bank deposits, repos or short-term Treasury bills). This reserve of liquid assets must be accounted for off the issuer's balance sheet, and stablecoin holders have absolute priority in the event of the issuer's bankruptcy. In other words, stablecoins are now legally protected claims that can be exchanged for a fixed amount of fiat currency. They are therefore set to become a common payment instrument used in e-commerce, international money transfers and decentralised finance (DeFi).

The GENIUS Act is explicitly designed to strengthen the dollar's dominant position globally. By requiring US stablecoins to be pegged to dollar-denominated assets, it directly links the expansion of digital currencies to the dollar. Stablecoins make it possible to use the dollar without necessarily having a US bank account, particularly in emerging markets where demand for dollars is high but access to banking services is limited.

The dollar thus becomes the default currency of the digital age. While central bank digital currency (CBDC) faces political opposition in the United States, the GENIUS Act achieves the strategic goal of the latter via the private sector, namely the global expansion of a regulated dollar-denominated token. This reinforces the network effects of the greenback at a time when the United States' geopolitical rivals are encouraging the use of alternative currencies. By making the dollar easier to access and cheaper to use via blockchain, the new law could slow down de-dollarisation.

80% of the $200 bn in stablecoin reserves are Treasury bills and repos. With the GENIUS Act paving the way for institutional adoption of stablecoins, it is not impossible that their outstanding amount could reach $1 to $2 trn within a few years. This additional demand for short-term Treasury bills could amount to several hundred billion. It would be welcome, as these securities are struggling to find buyers while the budget deficit is increasing. It remains to be seen whether this will be net demand or simply a reallocation. If the growth in demand for stablecoins comes at the expense of money market funds or bank deposits, the Treasury could lose on one hand what it gains on the other.

Beyond regulatory clarification, the GENIUS Act reflects a deeper trend, namely the tokenisation of real assets. Stablecoins are the first large-scale example of a tokenised fiat currency. By formally offering them a place in the financial system, the Act implicitly validates tokenisation as a means of modernising finance. Thus, the GENIUS Act aims not only to regulate stablecoins, but also to lay the groundwork for a tokenised economy, where dollars, treasury bills, and eventually stocks or real estate could all be digitised and instantly traded on the blockchain.

For banks and investors, reshaping the flow of money and financial assets will open up new opportunities over the next decade. Once considered a speculative instrument, stablecoins are poised to become one of the main pillars of the financial system. As bridges between fiat currency and cryptocurrency, they are one of the building blocks of a tokenised economy.

Equities

Specific stock weekly performances:

Intel (+22% on Nvidia $5bn capital injection for 4% equity), US Oklo (+63% on strong demand for nuclear fuel), Kering (+11%), Novo Nordisk (+11%)

Orsted (-47% on poor outlook, is to raise $9.5bn equity capital), SIG (-31% on poor outlook), Bolloré (-4%) Vinci (-1%)

M&A:

Roche is to buy US 89Bio (+84%) for $3.5bn; Puma (+13%) Authentic Brands and CVC are said to be interested in 29% equity from Pinault

Analysts: Airbus (RBC ‘o/w’ target €220), Dassault Aviation (JPM ‘neutral’ target €325), Solvay (MS ‘u/w’ target €25)

Rates

US curve (2-10 years) steepening slightly up at 55bps (+5)

HY corporate spreads lower -10bps (US at 270bps; EU at 275bps)

Commodities

Oil price unchanged

Gold price higher (+1%) new ATH at $3705 an ounce (on FED cut)

Silver YTD performance is at +48%, while Platinum is at +53%

UK

Aug CPI at +3.8% unchanged (Core at 3.6%) CPIH at 4.1% (Core at 4%)

Crypto

BTC unchanged

Under the watch

France debt rating reviews (Moody’s 24 Oct; S&P 28 Nov)

US budget and fiscal situation (Oct 14 US court decision over tariffs)

Nota Bene

Elon Musk bought for $1bn worth of Tesla shares last Monday

The South Korean stock index (Kospi) shows a YTD performance at +45%; Spain’s IBEX at +30% and Poland’s WIG at +25%

CALENDAR

Earnings releases :

US Micron (23 Sep), EU H&M (25 Sep)

Macro releases :

US August PCE inflation (26 Sep)

WHAT ANALYSTS SAY

- Lazard: The entry point is crucial when investing in infrastructure

- Digital Asset Solutions: XRP, overrated or well desrved number 3?

- Indosuez/DPAM: Genius Act, a turning point for the digital dollar?

Lazard Asset, 19 September 2025

Author: Bertrand Cliquet, Portfolio Manager

As part of our strategy, infrastructure investments provide significant diversification for investors. There are listed companies active in infrastructure that have very different cash flow dynamics, distinct specialisations and low correlation with economic conditions. We focus on what are known as ‘preferred infrastructure’ companies. These are companies that are characterised by a high degree of predictability in terms of future cash flow trends. These companies enjoy a form of monopoly, are able to pass on price increases, operate within proven regulatory frameworks and offer legal recourse. It is indeed very important to have a reliable regulatory environment.

Unlike certain other sectors of activity in which companies can choose their production locations, it is not generally possible to relocate infrastructure-related activities. For example, it is not possible to move the operation of electricity grids or motorway tolls.

Firstly, there is the energy sector, which includes utilities, network equipment used for electricity transmission, and companies that manage water networks, particularly in the United Kingdom and Italy. The second sector is transport. This includes companies that operate airports and motorways. The third sector consists of companies active in telecommunications.

The decisive criterion is the essential nature of the services. Companies that operate electricity, water and gas networks are very little exposed to volume fluctuations. It would take a very severe recession for people to reduce their water consumption, for example. By comparison, the revenues of companies that operate motorway tolls are not completely unrelated to the economic climate, but the variations are much smaller than for other companies active in the transport sector. The risks are therefore limited, even in the event of a recession.

In addition, some concession agreements provide for mechanisms to adjust tariffs based on volumes. This makes margin and cash flow trends more predictable.

As an investor, it is important to pay close attention to the prices paid for assets. This is because assets do not change, or change very little, over time. It is not like in the technology sector, for example, where companies and their results evolve very quickly. The entry point is an essential aspect when investing in infrastructure. That is why it is also important to be wary of trends that are considered most attractive at certain times. A few years ago, it was essential to have investments in renewable energy. This resulted in stratospheric valuations around 2023. In 2024, the trend reversed. Over the past two years, we have seen prices for certain assets fall by up to 60%. This means that price declines are possible even when nothing has happened technically or operationally.

Lower interest rates have not always had the same impact on infrastructure investments on both sides of the Atlantic. In the United States, utility companies have generally benefited from lower interest rates. In Europe, however, returns on invested capital have increased in line with the rise in interest rates in recent years. It can therefore be observed that interest rates have less of an impact on returns in Europe than in the United States. At the same time, regulatory authorities also take interest rate levels into account – if rates fall sharply, they may also want consumers to benefit from lower financing costs.

Infrastructure companies in a monopoly position are subject to a regulatory framework that allows them to pass on the costs of purchasing materials in their tariffs. Thus, if companies were to import electrical transmission cables or transformers, for example, customs duties would be passed on to the consumer. Furthermore, there are so many investment opportunities, ranging from the renewal of ageing assets to the connection of data centres, that we see little risk to these companies' organic growth prospects.

It is important to consider the total return obtained, not just the nominal amount of dividends received. In infrastructure, dividend yields are generally higher than the market average.

Digital Asset Solutions, 19 September 2025

Author: Leon Curti, Head of Research

XRP, Ripple's flagship product, On-Demand Liquidity (ODL), enables real-time payments. Banks exchange their currency for XRP, transfer it to the destination country and convert it back locally, without the need for costly foreign currency accounts. This reduces capital tie-up and costs. ODL is considered the most important application of XRP, but is only available in a few corridors. In the second quarter of 2025, the transaction volume amounted to USD 1.3 billion. By comparison, stablecoins such as USDT and USDC process nearly USD 3 trillion per month.

Since 2020, Ripple had been involved in costly litigation with the SEC, the US financial markets regulator, which considered XRP to be an unregistered security. This also hampered institutional partnerships. It was not until 2025 that the tide turned: the SEC closed the case, confirming that XRP is not considered a security in public trading. During the same quarter, trading volume increased significantly, despite a decline in the number of new retail addresses. Thus, in the first quarter of 2025, the XRP ledger processed approximately two million transactions per day and was among the most active blockchains. Three-quarters of all transactions were confirmed in less than five seconds, which is ideal for high-frequency, low-margin payments. The number of active accounts continued to increase, reaching approximately 130,000 per day.

In addition, Ripple has applied for a national banking licence from the US Office of the Comptroller of the Currency (OCC) and is seeking to obtain a master account with the Federal Reserve in order to have direct access to the US payment system. In Europe, expansion is being driven by Ripple Payments Europe SA in Luxembourg, where an EMI licence has been applied for in order to introduce the RLUSD stablecoin in a regulated manner throughout the EEA.

At the same time, XRP is gaining ground in the US financial markets. Asset managers such as Grayscale and WisdomTree have filed applications with the SEC for spot ETF authorisation. If approved, XRP would be the next major cryptocurrency to offer a US spot ETF, after Bitcoin and Ethereum. The outlook is currently considered good. Such a product could significantly facilitate institutional capital inflows into XRP.

From an investor perspective, the picture is mixed.

On the one hand, regulatory clarity, the growing importance of stablecoins, possible ETF approvals and numerous institutional partnerships point to upside potential. On the other hand, on-chain usage by banks and payment service providers remains limited.

Established stablecoins such as USDT and USDC, as well as potential central bank digital currencies (CBDCs), limit the scope of application, while high volatility remains a barrier to payment transactions. Demand for XRP is also limited, as the token is not essential to the core business.

The high market capitalisation is therefore heavily dependent on marketing, networking and acquisitions, while the concentration of tokens in Ripple and its founders – nearly 40% of the total tokens – creates pressure for future sales.

In addition, the possibility of an initial public offering (IPO) of Ripple, which has been mentioned repeatedly, creates uncertainty. For investors, this means that XRP remains a speculative asset, offering opportunities but also risks. Consequently, it may be wise to adjust one's positioning according to one's risk appetite or to determine it by market weighting.

Indosuez/DPAM, 19 September 2025

Author: Ewout de Brauwer, Portfolio Manager

Until now, the stablecoin landscape has resembled a patchwork of regulations, major issuers such as Circle and Paxos operated within the New York regulatory framework, while others benefited from less stringent state licences. The market was operating in a legal grey area, which has now been cleared up thanks to the creation of the category of federally authorised stablecoin issuers (PPSIs) defined by the GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins Act, July 2025). This category includes bank subsidiaries, federally chartered non-banks supervised by the Office of the Comptroller of the Currency (OCC), and state-approved issuers whose stablecoin assets are less than $10bn (above this threshold, they must cease operations or come under federal supervision).

The Act also requires each stablecoin to be backed by a high-quality liquid asset (cash, bank deposits, repos or short-term Treasury bills). This reserve of liquid assets must be accounted for off the issuer's balance sheet, and stablecoin holders have absolute priority in the event of the issuer's bankruptcy. In other words, stablecoins are now legally protected claims that can be exchanged for a fixed amount of fiat currency. They are therefore set to become a common payment instrument used in e-commerce, international money transfers and decentralised finance (DeFi).

The GENIUS Act is explicitly designed to strengthen the dollar's dominant position globally. By requiring US stablecoins to be pegged to dollar-denominated assets, it directly links the expansion of digital currencies to the dollar. Stablecoins make it possible to use the dollar without necessarily having a US bank account, particularly in emerging markets where demand for dollars is high but access to banking services is limited.

The dollar thus becomes the default currency of the digital age. While central bank digital currency (CBDC) faces political opposition in the United States, the GENIUS Act achieves the strategic goal of the latter via the private sector, namely the global expansion of a regulated dollar-denominated token. This reinforces the network effects of the greenback at a time when the United States' geopolitical rivals are encouraging the use of alternative currencies. By making the dollar easier to access and cheaper to use via blockchain, the new law could slow down de-dollarisation.

80% of the $200 bn in stablecoin reserves are Treasury bills and repos. With the GENIUS Act paving the way for institutional adoption of stablecoins, it is not impossible that their outstanding amount could reach $1 to $2 trn within a few years. This additional demand for short-term Treasury bills could amount to several hundred billion. It would be welcome, as these securities are struggling to find buyers while the budget deficit is increasing. It remains to be seen whether this will be net demand or simply a reallocation. If the growth in demand for stablecoins comes at the expense of money market funds or bank deposits, the Treasury could lose on one hand what it gains on the other.

Beyond regulatory clarification, the GENIUS Act reflects a deeper trend, namely the tokenisation of real assets. Stablecoins are the first large-scale example of a tokenised fiat currency. By formally offering them a place in the financial system, the Act implicitly validates tokenisation as a means of modernising finance. Thus, the GENIUS Act aims not only to regulate stablecoins, but also to lay the groundwork for a tokenised economy, where dollars, treasury bills, and eventually stocks or real estate could all be digitised and instantly traded on the blockchain.

For banks and investors, reshaping the flow of money and financial assets will open up new opportunities over the next decade. Once considered a speculative instrument, stablecoins are poised to become one of the main pillars of the financial system. As bridges between fiat currency and cryptocurrency, they are one of the building blocks of a tokenised economy.

Contacts

Main office

1-5, № 53, 12 Charents Str., Yerevan, 0025

+374 43 00-43-82

Broker

broker@unibankinvest.am

research@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.