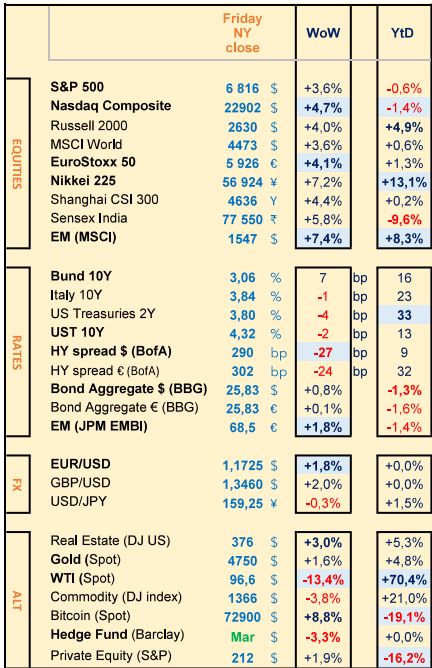

Last week : Risk On (Stocks +4%, Corp spreads lower -25bps, USD lower -2%, Oil much lower -13%, BTC +9%)

WEEKLY TRENDS

WEEKLY TRENDS

- Full Risk On mode last week after a fragile 2 week ceasefire was announced on Tuesday evening followed by negotiations taking place in Islamabad, starting this weekend.

- EM stocks is leading the equity indices pack with +7.5% while HY Corporate spreads went lower by 25bps, the USD lost 2%, the US Real Estate index managed to climb up by 3%, Oil is much lower at -13%, BTC ended the week at +9%. The Russell 2000, the DJ transport sector and the MSCI Emerging Markets (EM) all rebounded on their key support levels (which were previous resistance levels).

- Gold continued its rally for a 3rd week (off its 200 day Moving Average, briefly hit on March 23rd at $4175)

- The Nasdaq 100 has now risen for 7 straight sessions, and is back above its pre-Iran-war level. This coming week, we shall have the Q1 earnings season start, with Goldman Sachs opening the ball on Monday, followed by JP Morgan, Wells Fargo, Citi, BlackRock on Tuesday, Bank of America and Morgan Stanley on Wednesday. Macro wise, we will have the US PPI for March delivered on Tuesday. NB Moody’s left unchanged their rating for France late Friday.

MARKETS

Equities

Q4 earnings weekly performances : Shell (-3%)

NB weekly : ST Micro (+16%) Arcelor Mittal (+14%) SocGen (+11%) Thales (-3%) Dassault Systems (-4%) Avis (+57%)

Bank analysts : Spie (MS ‘o/w’ target €51) Anheuser Inbev (MS ‘o/w’ target €70) Accor (UBS ‘buy’ target €63)

M&A : Universal Music (+13%) on surprising offer from Pershing Square (Bill Ackman’s offer has a 78% premium on current price)

Rates

US curve steepening (2-10 years) stable at +52bps (+2bps)

HY corp. spreads lower : US at +290bps (-25) ; EU at +300bps (-25bps)

Commodities

Oil price WTI much lower (-13%) Gold price higher (+1.5%) helped by a weaker USD ; Dutch TTF Gas (-12%)Copper (+4%) the highest it has been in London for the last 3 months

Crypto

BTC (+4%) ETH (+5%) SOL (+2%) XRP (+1%)

US

March CPI +3.3% vs +3.4% exp. (Core at 2.6% vs 2.7% exp.)

Feb PCE +2.8% vs +2.8% exp. (Core at +3% vs 3.1% prior and 3% exp.)

Under the watch

MSCI World lost 6% in March (its worst performance in 3 years) but gained 5% early April

Nota Bene

Panda Bonds (in RMB) are the new hot thing in Q1 (despite lower yields than USTs, China 10yr at 1.8% vs UST10 at 4.3%)

Moody’s kept its rating for France unchanged

CALENDAR

Earnings releases : US GS (13) JPM, Wells F., Citi (14) BofA, MS (15) Netflix, Pepsico, Abbott (16), EU ASML (15 April)

Macro releases : US March PPI (14 April)

WHAT ANALYSTS SAY

Edmond de Rothschild AM, 10 April 2026

Author : Michael Nizard, Multi Asset & Overlay Director

A 15-day ceasefire was agreed at the last minute on Tuesday evening between the US and Iran, following tensions marked by explicit threats from Donald Trump, who had raised the possibility of “wiping out the entire Iranian civilisation”.

The 10-point Iranian plan demands a non-aggression pledge from the US, the withdrawal of its combat forces from the region, an end to the war on all fronts – including against the ‘Islamic resistance’ in Lebanon – the maintenance of Iranian control over the Strait of Hormuz, recognition of a “right to enrich” uranium, the lifting of all sanctions and the payment of reparations to Tehran.

This document, which Donald Trump nevertheless presents as a “viable basis” for negotiation, differs markedly from the 15-point US plan, which focuses on ending Iran’s nuclear programme, the handover of enriched uranium stocks, the limitation of ballistic capabilities and the international securing of the Strait of Hormuz.

Netanyahu has officially backed the truce, but Israel has made it clear that this does not apply to its operations against Hezbollah in Lebanon, which, together with the reopening of the strait to shipping, constitutes a major point of vulnerability for the upcoming negotiations.

This geopolitical de-escalation had an immediate impact on energy prices. Meanwhile, Iran and Oman have discussed introducing a transit fee of around $1 per barrel for oil flows passing through the Strait of Hormuz, which Tehran has not yet reopened to shipping. The Executive Director of the International Energy Agency (IEA) indicated that oil supply constraints are expected to tighten significantly in April, due to a shortfall of 12 million barrels per day, once the tankers already at sea when hostilities broke out have delivered their cargoes.

The de-escalation in the Middle East has led to a easing of government bond yields and a rebound in risk assets, whilst market expectations regarding monetary policy are being revised downwards across the board. In the UK, for example, investors now anticipate just under two key interest rate hikes in 2026, compared with four at the height of the conflict.

Business surveys for March show a more pronounced impact of the conflict in the eurozone than in the US. The US ISM services index remains in expansionary territory, at 54 compared with 56.1 in February, with the prices sub-index at 70.7 compared with 63.0, confirming that cost pressures remain high in the services sector. In the eurozone, PMIs appear more fragile in countries heavily exposed to exports to the Gulf, such as Italy, where these surveys have now moved into contraction territory.

The desire to end the conflict, and the appointment of J.D. Vance to lead the negotiations, lead us to continue rebalancing the risk in our diversified portfolios, across both equities and credit. We are also adding duration to the short end of the yield curves to benefit from downward revisions to central bank rate hikes.

DNCA, 9 April 2026

Author : Pierre Pincemaille, Asset Management General Secretary

Regional Outlook: Stagflationary trends influence central bank policy

Following a surprisingly strong start to the year, we expect growth in the US to slow by mid-2026. Rising energy costs are likely to keep inflation around 3%, once again above the Fed’s 2% target. This should prompt the central bank to cut its key interest rates later than expected, bringing them down to around 3.5% by the end of 2026.

For Europe, we forecast moderate growth of 1–1.5% in 2026, with positive momentum coming from Germany. At the same time, rising energy prices are expected to push inflation in the eurozone above the European Central Bank’s (ECB) 2% target. Against this backdrop, we believe it is likely that the ECB will not cut rates this year and that the threshold for hikes is low.

Finally, in Asia, the economic outlook remains mixed. Whilst fiscal stimulus measures are running out of steam in China, Japan is benefiting from additional public spending. This should prompt the Bank of Japan to raise its interest rates by a further 50 basis points this year.

Equities: strategic autonomy, energy and AI as key drivers

With regard to equity investments, we highlight certain thematic trends: Europe’s drive to strengthen its strategic autonomy – particularly in defence, but also in energy supply, digitalisation and healthcare – is gaining considerable momentum and becoming a globally significant investment theme. At the same time, the recent escalation in the Middle East highlights the persistent vulnerability of energy supply chains. The sectors concerned are likely to benefit. We see strong structural drivers in the technology sector. AI is and remains a key theme across global equity markets. China is accelerating the adoption of AI, and global demand for semiconductors as well as energy infrastructure such as networks and data centres is rising significantly. In terms of valuations, Japan and the UK remain the most attractive markets.

Bonds: quality, a selective approach and active duration management

We warn of widening disparities in the bond markets. In an increasingly volatile environment, the markets reward selectivity. Inflation fuelled by oil prices and rising risk aversion are sending mixed signals for bonds. In this context, market participants should prioritise quality yields, balance sheet strength and active duration management. Japan and UK government bonds, followed by US Treasuries, appear relatively attractive to us in this context.

As for corporate bonds, this segment has proved particularly stable despite increased volatility in the equity markets. Within the bond markets, Euro Investment Grade bonds continue to stand out as offering the best value, although US Investment Grade bonds have narrowed the gap compared with the previous three months. Furthermore, emerging market bonds can offer resilient yields and diversification benefits. Asian bonds are particularly notable for their low volatility.

UBS, 8 April 2026

Authors : Mark Haefele, Global Wealth Management Chief Investment Officer

On the positive side:

• The ceasefire signals that both sides wish to avert a worst-case scenario of a prolonged closure of the Strait of Hormuz and further damage to civilian and energy infrastructure. Negotiating should also help improve the probability of eventual agreement and reduce the probability of severe escalation. Like we saw after "Liberation Day," temporary truces can also be extended.

• The prospect of greater flow through the Strait of Hormuz should support sentiment in markets most subject to shortages, including those in Asia-Pacific and sectors exposed to diesel and jet fuel. The latest data had started to show larger inventory draws in Japan and India.

• The price of energy tends to have a non-linear impact on economic growth, with oil price levels above USD 150/bbl starting to have an exponentially negative impact.

• Moderately, but not dramatically, higher energy prices than pre-conflict levels should mean that central banks do not feel the need to increase interest rates, provided energy flows sustainably resume.

• The approaching US midterm elections, declining popularity ratings for President Trump and for the conflict, domestic concerns about higher gas prices, and criticism from some Republicans over recent rhetoric may increase President Trump’s willingness to strike a deal.

Several risks remain:

• It is not yet clear how quickly, to what extent, traffic through the Strait of Hormuz will normalize. It will take time for tankers not currently in the region to reroute. Tankers may be less willing to return as the end of the two-week ceasefire window approaches.

• Damaged energy infrastructure needs to be repaired, it could take weeks or months to resume shut-in production, and operators may be hesitant to resume while continued passage through the Strait remains in question. With this in mind, it is unlikely that energy prices will fall back to preconflict levels in the near term, and this will weigh on growth.

• We note that Iran’s Revolutionary Guard has stated that passage through the Strait of Hormuz can only be conducted "in coordination with Iran’s armed forces." It is not clear if Iran will retain de-facto control over the Strait and/or if it wishes to charge vessels for passage.

• We also note that President Trump’s demands for limits on Iran’s nuclear programs have not been agreed, nor have Iran’s demands to lift sanctions, guarantee long-term security, withdraw US troops from the region, and for Israel to cease hostilities against regional proxies. Israel has already stated that the ceasefire “does not include Lebanon.” Negotiations in Pakistan, starting on Friday, may start to unveil some of these differences. Any resolution that does not cover Iranian nuclear enrichment and ballistic missile programs may present longer-term risks if the US or Israel in the future perceive that nuclear threats are growing again.

Equities

Q4 earnings weekly performances : Shell (-3%)

NB weekly : ST Micro (+16%) Arcelor Mittal (+14%) SocGen (+11%) Thales (-3%) Dassault Systems (-4%) Avis (+57%)

Bank analysts : Spie (MS ‘o/w’ target €51) Anheuser Inbev (MS ‘o/w’ target €70) Accor (UBS ‘buy’ target €63)

M&A : Universal Music (+13%) on surprising offer from Pershing Square (Bill Ackman’s offer has a 78% premium on current price)

Rates

US curve steepening (2-10 years) stable at +52bps (+2bps)

HY corp. spreads lower : US at +290bps (-25) ; EU at +300bps (-25bps)

Commodities

Oil price WTI much lower (-13%) Gold price higher (+1.5%) helped by a weaker USD ; Dutch TTF Gas (-12%)Copper (+4%) the highest it has been in London for the last 3 months

Crypto

BTC (+4%) ETH (+5%) SOL (+2%) XRP (+1%)

US

March CPI +3.3% vs +3.4% exp. (Core at 2.6% vs 2.7% exp.)

Feb PCE +2.8% vs +2.8% exp. (Core at +3% vs 3.1% prior and 3% exp.)

Under the watch

MSCI World lost 6% in March (its worst performance in 3 years) but gained 5% early April

Nota Bene

Panda Bonds (in RMB) are the new hot thing in Q1 (despite lower yields than USTs, China 10yr at 1.8% vs UST10 at 4.3%)

Moody’s kept its rating for France unchanged

CALENDAR

Earnings releases : US GS (13) JPM, Wells F., Citi (14) BofA, MS (15) Netflix, Pepsico, Abbott (16), EU ASML (15 April)

Macro releases : US March PPI (14 April)

WHAT ANALYSTS SAY

- Edmond de Rothschild: A truce as fragile as crystal

- DNCA: Private debt, a problem that is becoming a public concern

- UBS: Ceasefire, global markets investment perspectives

Edmond de Rothschild AM, 10 April 2026

Author : Michael Nizard, Multi Asset & Overlay Director

A 15-day ceasefire was agreed at the last minute on Tuesday evening between the US and Iran, following tensions marked by explicit threats from Donald Trump, who had raised the possibility of “wiping out the entire Iranian civilisation”.

The 10-point Iranian plan demands a non-aggression pledge from the US, the withdrawal of its combat forces from the region, an end to the war on all fronts – including against the ‘Islamic resistance’ in Lebanon – the maintenance of Iranian control over the Strait of Hormuz, recognition of a “right to enrich” uranium, the lifting of all sanctions and the payment of reparations to Tehran.

This document, which Donald Trump nevertheless presents as a “viable basis” for negotiation, differs markedly from the 15-point US plan, which focuses on ending Iran’s nuclear programme, the handover of enriched uranium stocks, the limitation of ballistic capabilities and the international securing of the Strait of Hormuz.

Netanyahu has officially backed the truce, but Israel has made it clear that this does not apply to its operations against Hezbollah in Lebanon, which, together with the reopening of the strait to shipping, constitutes a major point of vulnerability for the upcoming negotiations.

This geopolitical de-escalation had an immediate impact on energy prices. Meanwhile, Iran and Oman have discussed introducing a transit fee of around $1 per barrel for oil flows passing through the Strait of Hormuz, which Tehran has not yet reopened to shipping. The Executive Director of the International Energy Agency (IEA) indicated that oil supply constraints are expected to tighten significantly in April, due to a shortfall of 12 million barrels per day, once the tankers already at sea when hostilities broke out have delivered their cargoes.

The de-escalation in the Middle East has led to a easing of government bond yields and a rebound in risk assets, whilst market expectations regarding monetary policy are being revised downwards across the board. In the UK, for example, investors now anticipate just under two key interest rate hikes in 2026, compared with four at the height of the conflict.

Business surveys for March show a more pronounced impact of the conflict in the eurozone than in the US. The US ISM services index remains in expansionary territory, at 54 compared with 56.1 in February, with the prices sub-index at 70.7 compared with 63.0, confirming that cost pressures remain high in the services sector. In the eurozone, PMIs appear more fragile in countries heavily exposed to exports to the Gulf, such as Italy, where these surveys have now moved into contraction territory.

The desire to end the conflict, and the appointment of J.D. Vance to lead the negotiations, lead us to continue rebalancing the risk in our diversified portfolios, across both equities and credit. We are also adding duration to the short end of the yield curves to benefit from downward revisions to central bank rate hikes.

DNCA, 9 April 2026

Author : Pierre Pincemaille, Asset Management General Secretary

Regional Outlook: Stagflationary trends influence central bank policy

Following a surprisingly strong start to the year, we expect growth in the US to slow by mid-2026. Rising energy costs are likely to keep inflation around 3%, once again above the Fed’s 2% target. This should prompt the central bank to cut its key interest rates later than expected, bringing them down to around 3.5% by the end of 2026.

For Europe, we forecast moderate growth of 1–1.5% in 2026, with positive momentum coming from Germany. At the same time, rising energy prices are expected to push inflation in the eurozone above the European Central Bank’s (ECB) 2% target. Against this backdrop, we believe it is likely that the ECB will not cut rates this year and that the threshold for hikes is low.

Finally, in Asia, the economic outlook remains mixed. Whilst fiscal stimulus measures are running out of steam in China, Japan is benefiting from additional public spending. This should prompt the Bank of Japan to raise its interest rates by a further 50 basis points this year.

Equities: strategic autonomy, energy and AI as key drivers

With regard to equity investments, we highlight certain thematic trends: Europe’s drive to strengthen its strategic autonomy – particularly in defence, but also in energy supply, digitalisation and healthcare – is gaining considerable momentum and becoming a globally significant investment theme. At the same time, the recent escalation in the Middle East highlights the persistent vulnerability of energy supply chains. The sectors concerned are likely to benefit. We see strong structural drivers in the technology sector. AI is and remains a key theme across global equity markets. China is accelerating the adoption of AI, and global demand for semiconductors as well as energy infrastructure such as networks and data centres is rising significantly. In terms of valuations, Japan and the UK remain the most attractive markets.

Bonds: quality, a selective approach and active duration management

We warn of widening disparities in the bond markets. In an increasingly volatile environment, the markets reward selectivity. Inflation fuelled by oil prices and rising risk aversion are sending mixed signals for bonds. In this context, market participants should prioritise quality yields, balance sheet strength and active duration management. Japan and UK government bonds, followed by US Treasuries, appear relatively attractive to us in this context.

As for corporate bonds, this segment has proved particularly stable despite increased volatility in the equity markets. Within the bond markets, Euro Investment Grade bonds continue to stand out as offering the best value, although US Investment Grade bonds have narrowed the gap compared with the previous three months. Furthermore, emerging market bonds can offer resilient yields and diversification benefits. Asian bonds are particularly notable for their low volatility.

UBS, 8 April 2026

Authors : Mark Haefele, Global Wealth Management Chief Investment Officer

On the positive side:

• The ceasefire signals that both sides wish to avert a worst-case scenario of a prolonged closure of the Strait of Hormuz and further damage to civilian and energy infrastructure. Negotiating should also help improve the probability of eventual agreement and reduce the probability of severe escalation. Like we saw after "Liberation Day," temporary truces can also be extended.

• The prospect of greater flow through the Strait of Hormuz should support sentiment in markets most subject to shortages, including those in Asia-Pacific and sectors exposed to diesel and jet fuel. The latest data had started to show larger inventory draws in Japan and India.

• The price of energy tends to have a non-linear impact on economic growth, with oil price levels above USD 150/bbl starting to have an exponentially negative impact.

• Moderately, but not dramatically, higher energy prices than pre-conflict levels should mean that central banks do not feel the need to increase interest rates, provided energy flows sustainably resume.

• The approaching US midterm elections, declining popularity ratings for President Trump and for the conflict, domestic concerns about higher gas prices, and criticism from some Republicans over recent rhetoric may increase President Trump’s willingness to strike a deal.

Several risks remain:

• It is not yet clear how quickly, to what extent, traffic through the Strait of Hormuz will normalize. It will take time for tankers not currently in the region to reroute. Tankers may be less willing to return as the end of the two-week ceasefire window approaches.

• Damaged energy infrastructure needs to be repaired, it could take weeks or months to resume shut-in production, and operators may be hesitant to resume while continued passage through the Strait remains in question. With this in mind, it is unlikely that energy prices will fall back to preconflict levels in the near term, and this will weigh on growth.

• We note that Iran’s Revolutionary Guard has stated that passage through the Strait of Hormuz can only be conducted "in coordination with Iran’s armed forces." It is not clear if Iran will retain de-facto control over the Strait and/or if it wishes to charge vessels for passage.

• We also note that President Trump’s demands for limits on Iran’s nuclear programs have not been agreed, nor have Iran’s demands to lift sanctions, guarantee long-term security, withdraw US troops from the region, and for Israel to cease hostilities against regional proxies. Israel has already stated that the ceasefire “does not include Lebanon.” Negotiations in Pakistan, starting on Friday, may start to unveil some of these differences. Any resolution that does not cover Iranian nuclear enrichment and ballistic missile programs may present longer-term risks if the US or Israel in the future perceive that nuclear threats are growing again.

Contacts

8 Kievyan Street, Yerevan, Armenia

+374 10 712 259

+374 43 004 182

unibankinvest@unibank.am

info@unibankinvest.am

Disclaimer

The information presented in the document contains a general overview of the products and services offered by Unibank OJSC (registered trademark – Unibank Invest, hereinafter referred to as the Bank).

The information is intended solely for the attention of the persons to whom it is addressed. Further dissemination of this information is allowed only with the prior consent of the Bank.

The information is only indicative, is not exhaustive and is provided solely for discussion purposes. The information should not be regarded as a public offer, request or invitation to purchase or sell any securities, financial instruments or services. The Bank reserves the right to make a final decision on the provision of these products and/or services to a specific customer, including refusing to provide products and/or services if such activities would be contrary to applicable law.

No guarantees in direct or indirect form, including those stipulated by law, are provided in connection with the specified information and materials. The information presented above cannot be considered as a recommendation for investing funds, as well as guarantees or promises of future profitability of investments.